AMD: The Perpetual Second

Equity research report

As noted in my Nvidia coverage, AMD seems to always appear behind the curve, appearing after leaders like Nvidia have taken most. AMD never displaced the leader in gaming; they were not first to the brief boom of crypto mining, and they were not first to the AI expansion. However, AMD has managed to carve out a piece of the market nonetheless, to the point where it almost seems like a strategy.

AMD has become a second-source specialist, entering huge markets with a dominant vendor. The problem huge markets with a dominant monopolist face is that customers have a structural desire for alternatives, which moderates prices, supply, and pushes the pace of innovation of the whole industry.

Company profile

Theme: AI Accelerator, Direction: Buy

Symbol: AMD, Exchange: NASDAQ

Sector: Technology, Industry: Semiconductors

Fair intrinsic value: $503 (-8%), as of July 10, 2026

Market capitalization: $894 532 million

Pricing data: P/S 24x, P/E 179x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

Perpetual second

Even AMD’s original x86 business benefited from IBM’s refusal to let Intel be the sole supplier in 1982, thus forcing a second source to emerge. However, not everything was rosy for AMD; in fact, it was on the brink of bankruptcy before now CEO Lisa Su entered as CEO in 2014. Ruthless capital allocation decisions had to be made to ensure the survival of AMD, and since it lacked the R&D budget to compete against both Nvidia and Intel, Lisa Su hedged AMD’s survival on the CPU side and took the fight to Intel. The GPU division was starved of funding, while Nvidia poured billions into R&D, extending its lead in architecture and efficiency. Therefore, while AMD never seems to be the industry leader, the company has had to carve a path through other means.

AMD, like Nvidia, is a semiconductor designer and outsources its manufacturing. Wafers are manufactured by TSMC TSM 0.00%↑, advanced packaging by OSAT and TSMC, and memory by SK hynix, Samsung, and Micron. Since AMD employs a fabless model, its capital intensity is structurally low. AMD is also able to scale free cash flow quickly with revenue growth, but the financial advantages also come with downsides. Supply has to be negotiated, thus becoming a forward-committed resource. Wafers, packaging slots, and high-bandwidth memory must be reserved quarters, or even years, ahead.

The revenue segments are divided by end market, ranging from gaming GPUs (Radeon), client encompassing desktop and notebook CPUs and APUs (Ryzen), to server CPUs (EPYC) and data center AI solutions (Instinct).

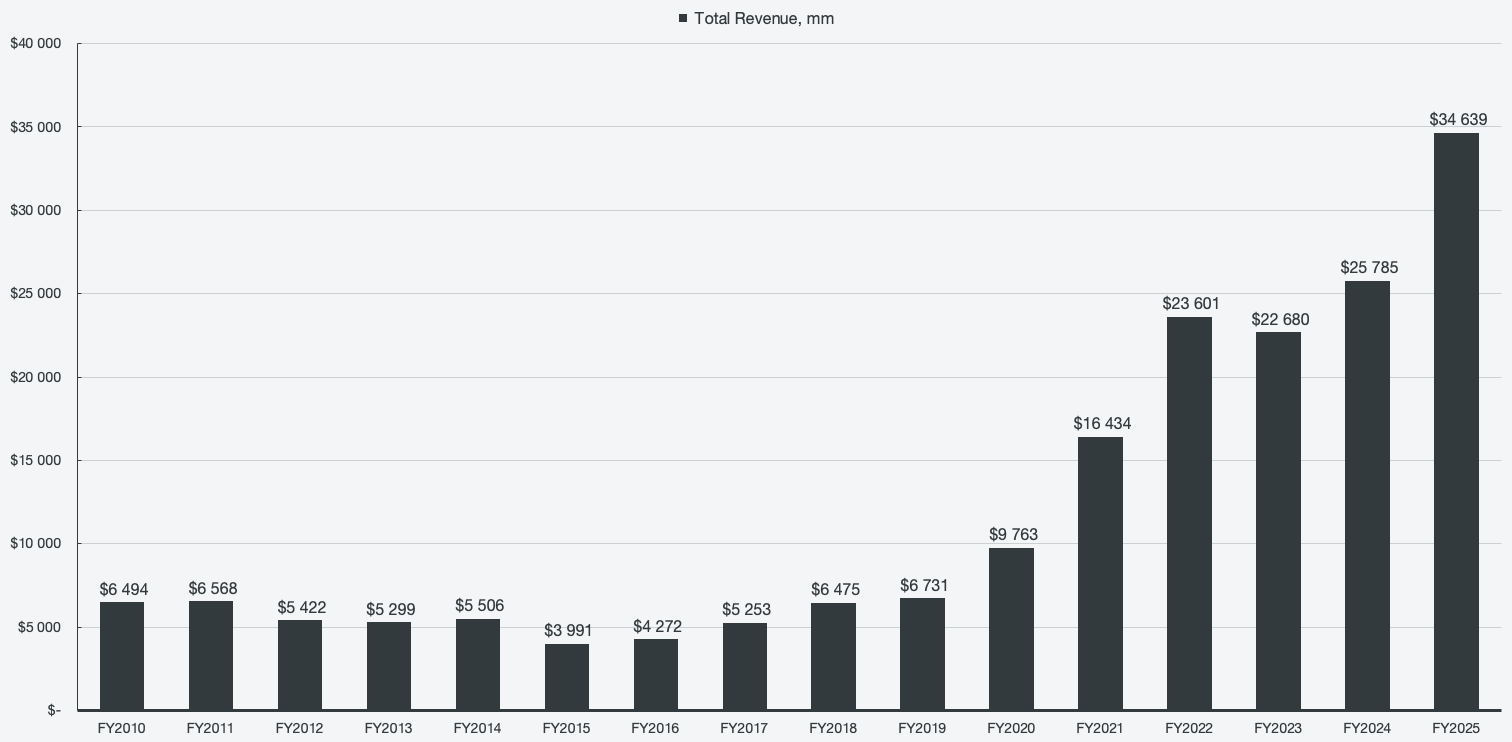

Figure 1: Total revenues

Data center will decide everything

The data center segment in particular is what makes or breaks the thesis for AMD, as everything hinges on whether AMD can stay a major player in the AI revolution. EPYC server CPUs and Instinct AI accelerators are sold to hyperscalers, cloud builders, enterprises, and AI labs. In a sense, the segment can be seen as two businesses at different stages of their lifecycles: a mature franchise in EPYC, and a hypergrowth business in Instinct. AMD reports them together, making it difficult to gauge how AI GPUs are performing against the backbone of server CPUs.

Looking at the market share at face value, it may seem like AMD has continuously lost its place in the market. However, that is due to Nvidia’s first-mover advantage in the AI space. Data centers have historically run on CPUs, solving sequential problems, one at a time. However, LLM training during this phase of the AI revolution requires a different kind of processing, namely solving many simpler tasks simultaneously. GPUs excel at parallel processing, and Nvidia was the first to capitalize on the opportunity, extending its dominance through its CUDA platform and NVLink technology. NVLink allows for multiple GPUs to process as a single, efficient cluster. Meaning, whenever a hyperscaler wanted to place a large order of GPUs, they couldn’t mix and match among vendors, allowing Nvidia to take most of the market. During the initial stages of the AI arms race, there was no time to wait for incumbents, and Nvidia’s inbound volumes exploded.

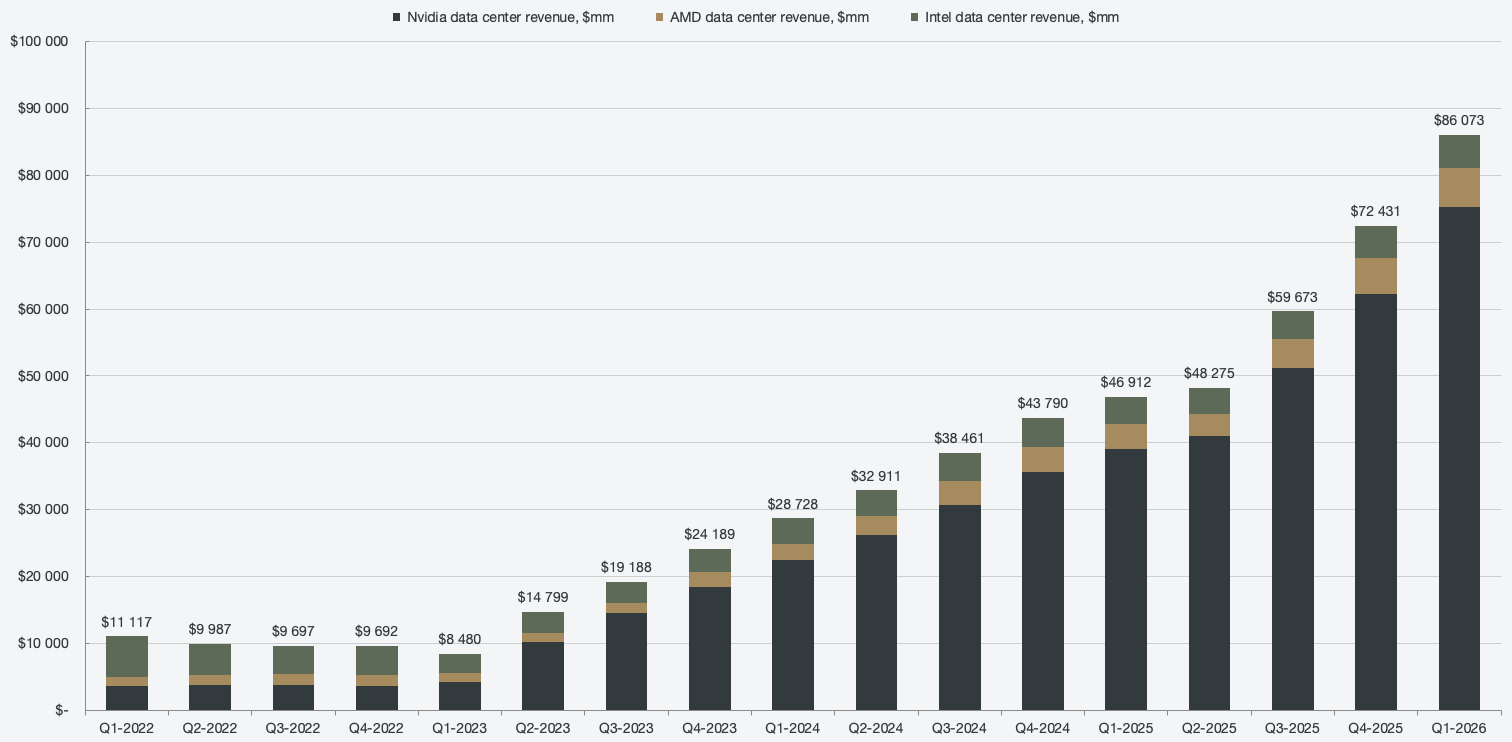

Figure 2: Data center revenues, segmented by vendor

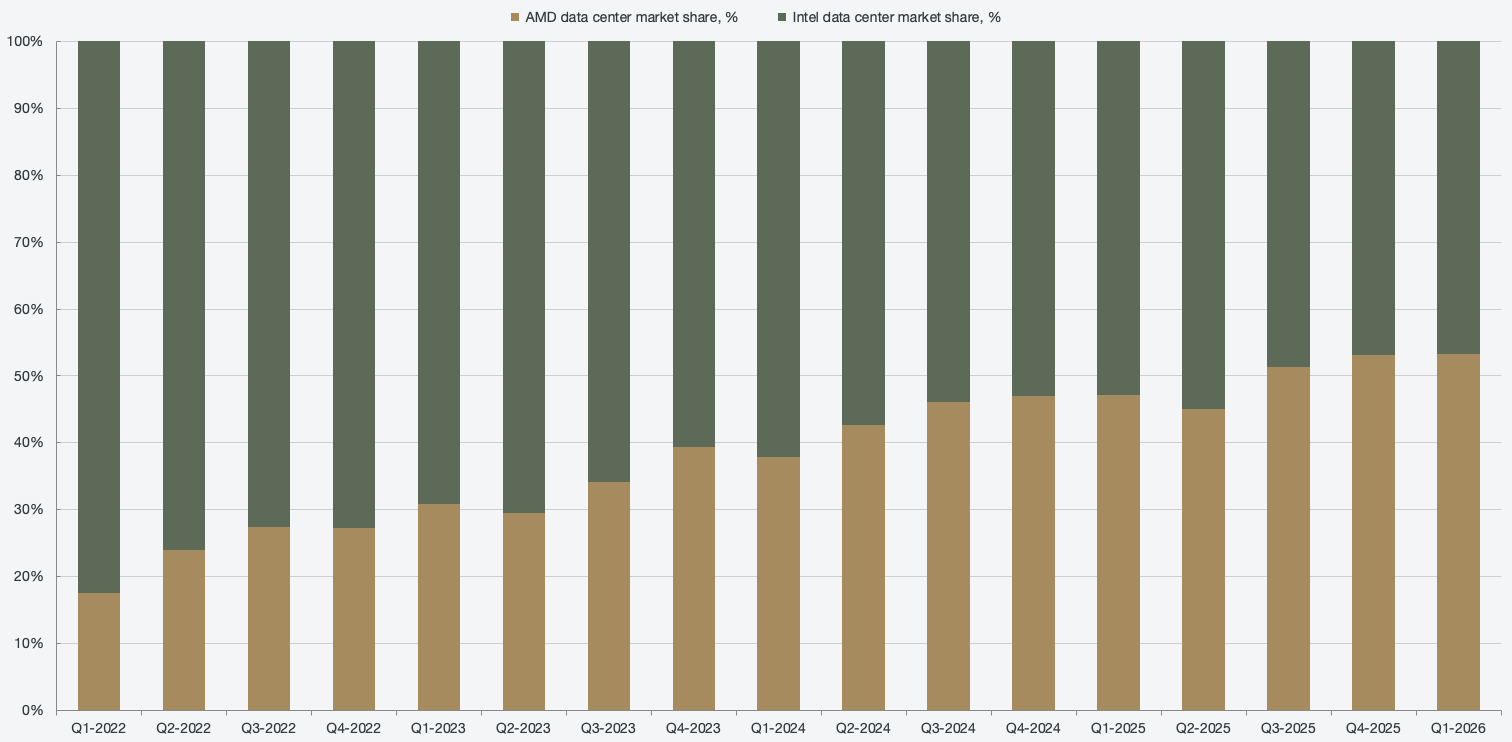

In Q1 2022, AMD held an implied 8% data center market share. In Q1 2026, that market share has diminished to 6.7%. At a glance, it spells disaster for AMD; not only is AMD not gaining market share, but it is actively losing it over time. However, excluding Nvidia from the picture, the market share narrative is turned on its head. AMD has gone from 11% data center market share to overtaking Intel at 54% market share in Q1 2026.

Figure 3: Implied data center market share between Intel and AMD

The CPU business is a qualification business that spans several years. A hyperscaler qualifies a platform, meaning the platform (CPU, firmware, software stack, etc) over half a year to a year, and then it is deployed over several years. That dynamic has protected Intel’s server business for decades, but once share flips, it typically stays flipped for a long time. AMD’s server share, while veiled, has likely not retraced for close to a decade since every EPYC generation has launched on time, while Intel’s advanced nodes have been delayed, and transitions have slipped.

The AI business is starting to shift massively, just as Nvidia saturated most of the market. Nvidia’s had such an immense edge that a second supplier became desperately needed. Unlike CPUs, AI platforms are bought in large-scale commitments, typically sized in gigawatts of data center power rather than units. They are also negotiated at the CEO level, to then be deployed as complete racks, which involve the compute, interconnectivity, networking, and cooling, rather than as mere chips. Nvidia’s rack solutions created vendor lock-ins since there were no alternatives, but AMD is now becoming competitive.

Historically, AMD’s weakness was software, but ROCm, which is the equivalent of Nvidia’s CUDA, is now becoming mature. CUDA and ROCm are software stacks that enable the harnessing of the compute power of GPUs. CUDA, while proprietary, was cleverly made available for free to researchers and universities over a decade ago, resulting in a majority of AI libraries, math frameworks, and learning models being specifically written for CUDA. That in and of itself created a moat, since customers would be reluctant to change vendors, as it would mean having to rewrite code from scratch. ROCm 7 makes it close to seamless to migrate AI/ML frameworks like PyTorch from Nvidia to AMD, and as such, the underlying hardware language now matters less.

Another major hurdle for AMD that is about to be overcome is that NVLink, like CUDA, is Nvidia’s proprietary technology for cluster processing. NVLink became mandatory since there was no alternative for unifying racks, forcing vendor lock-in. However, a coalition including Microsoft, Google, Meta, Intel, AMD, and Broadcom has come together in order to form the Ultra Accelerator Link (UALink) consortium. UALink will enable interchangeability between various semiconductor vendors, tearing down the walled garden that NVLink historically has provided. To further strengthen its rack-scale systems capability, AMD acquired ZT Systems in March of 2025, but divested the manufacturing arm and only kept the rack design and enablement teams.

Like UALink and ROCm, other layers of AMD’s stack are also open standards. AMD uses the OCP (Open Compute Project) open-rack standard introduced by Meta for its data center hardware. Vendors who fear vendor lock-in have strategic reasons to fund the open stacks.

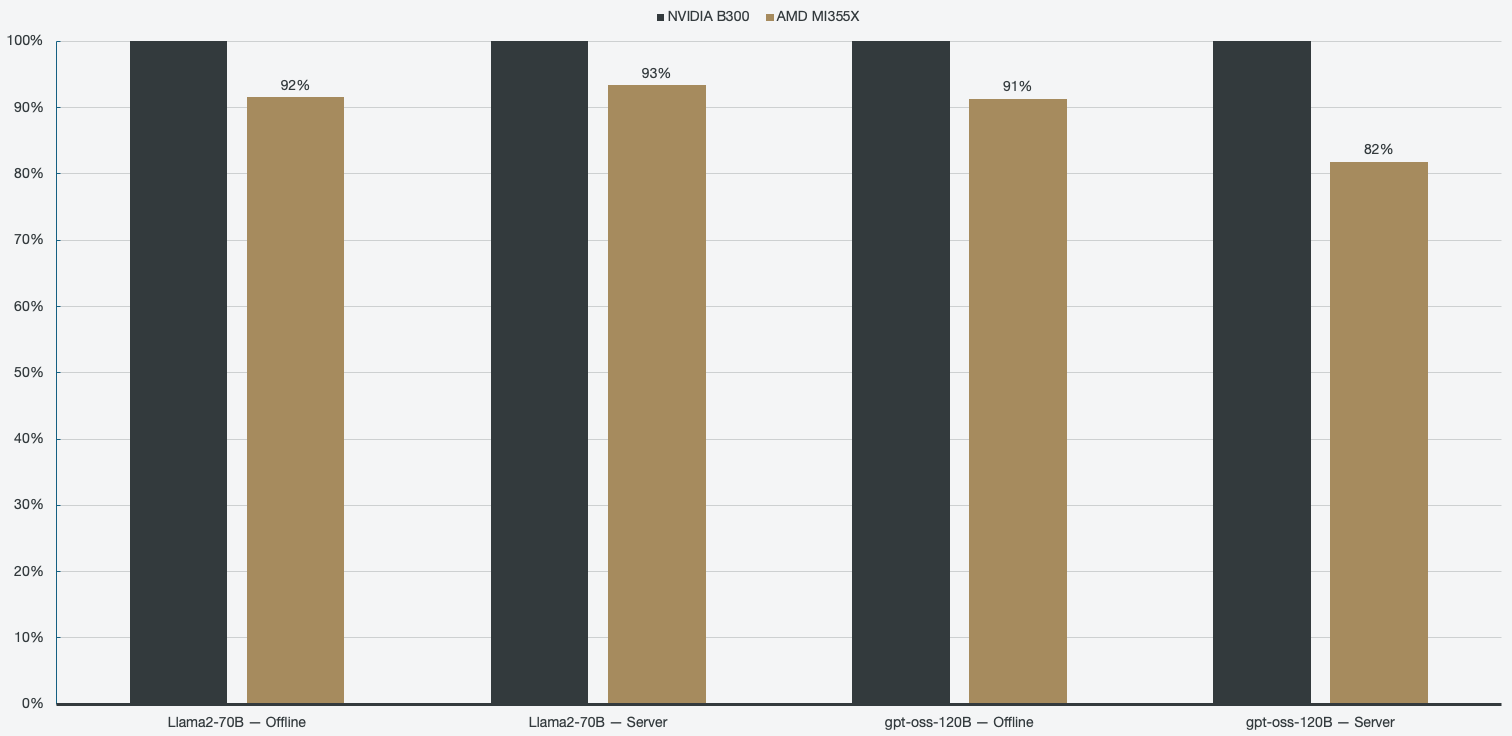

AMD’s key advantage is its price-per-performance, meaning tokens-per-dollar, especially in inference. That is also a key pivotal point in this stage of the AI buildout: large-language models are sophisticated enough to be widely deployed across enterprises, meaning that there is increasingly more demand for inference (using models) rather than just training. Customers, however, are unhappy with the costs of deploying AI, with many companies imposing per-employee token budgets.

Figure 4: LLM inference throughput, full system performance comparison against Nvidia

GPUs are versatile and can be applied to a wide variety of workloads, and while not the most efficient at every task, they are very flexible. As such, even though computational demand gradually shifts from training to inference, GPUs will still stay relevant as a jack-of-all-trades. However, the companies committing the most capital expenditures towards GPUs are the hyperscalers, most of which are now building out their own custom silicon (ASICs). That causes not only an introduction of new competition, but also a loss of revenue from the largest spenders.

The future of the AI data center market carries a lot of uncertainty, and forecasts by third-party experts are continuously revised. However, the consensus throughout the volatility in expectations all points towards a prosperous decade for AI accelerators. It is hard to predict how the near-term shift between GPUs and ASICs will play out, but it is looking like there is enough demand to stay distant from saturation for a long time to come. AMD has already de-risked the MI400 ramp by signing deals with both OpenAI and Meta for 6 gigawatts of AMD GPUs, which will take years to fulfill. AMD themselves target a >60% CAGR in the data center segment over the coming 3-5 years, citing a $1 trillion compute TAM by 2030 (>40% CAGR). That alone shows a lot of confidence in the experienced demand in the near-term.

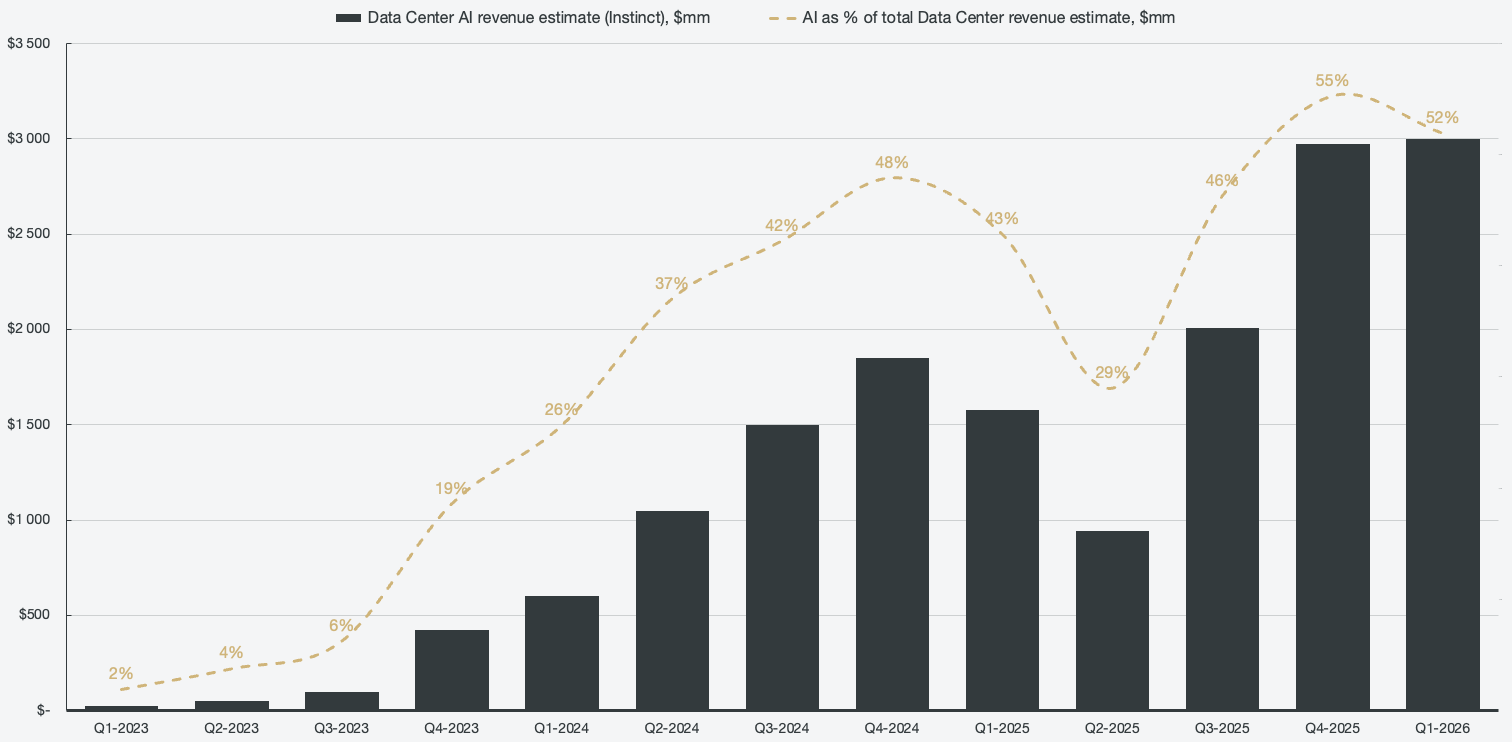

AMD discloses very limited information about its AI business within the data center segment. Using those clues and vague disclosures, I have tried to put forward an estimated AI data center revenue line. The implied acceleration is astonishing, going from ~2% of data center revenues to >50% in 3 years.

Figure 5: Estimated Data Center AI revenue