Constellation Software: Reinvestment Engine Is Not Out Of Gas

Equity research report

Constellation is not the type of business that I would typically look at, and I regarded an acquisition-centered business model to be relatively weak and without a moat. However, I received a commission on Type-F’s website to research the business, and what I found was truly an impressive compounding machine. A pleasant reminder not to judge a book by its cover, and when it comes to investing and equity research, keep an open mind.

Company profile

Theme: Compounding, Direction: Buy

Symbol: CSU, CNSWF, Exchange: TSX, OTCMKTS

Sector: Technology, Industry: Software - Infrastructure

Fair intrinsic value (CNSWF): $4039 (+27.55%), as of September 14, 2025

Market capitalization: $67 119 million

Pricing data: P/S 6.3x, P/E 92x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

Incredible growth, but…

Constellation Software, in short, acquires and operates small- to mid-size vertical market software (VMS) businesses. This is a set of niche software for highly specific and often mission-critical use cases or industries. These products may not have a large TAM but are instead deeply embedded in workflows and regulations, which makes them inherently sticky. The business model at face value is straightforward and simple, but the nuances are quite complex.

Figure 1: Historical segmented revenue

The company employs a disciplined approach in their M&A-heavy strategy, utilizing now decades of experience to identify and acquire VMS companies that meet their hurdle-rate criteria. Constellation has managed to grow their revenues at an impressive 24% CAGR since 2006, which translates to 4676% of total growth over the period. One may assume that most of the growth came in the earlier periods and that growth slows down with scale, but in reality, the past four years have grown at an average rate of 26%.

However, contrary to most other types of businesses, revenue growth is not the metric to watch for Constellation. Since the growth is largely inorganic, as it stems from M&A, the economics surrounding the acquisitions are more noteworthy measures to track for investors.

To understand how Constellation is able to compound its size so efficiently despite growing massively in scale, we have to look at the business structure. Founder Mark Leonard opposes bureaucracy and believes that it limits entrepreneurship. Instead, he devises a decentralized model that pushes decision-making down to the operating companies.

There are currently six operating groups, each having its own CEO, M&A team, culture, and internal systems. The operating groups contain hundreds of business units (BUs) of mostly acquired companies. Similarly to the operating groups, the BUs retain their own internal systems, management teams, and brands. Instead, the BUs are monitored and held to Constellation’s strict financial performance standards and are regularly measured based on return on invested capital (ROIC). This layered structure is what allows Constellation to keep expanding and scaling, despite how big it grows, as the company can always add more operating groups to allow for more M&A deals. However, while the business model is infinitely scalable, the market is not.

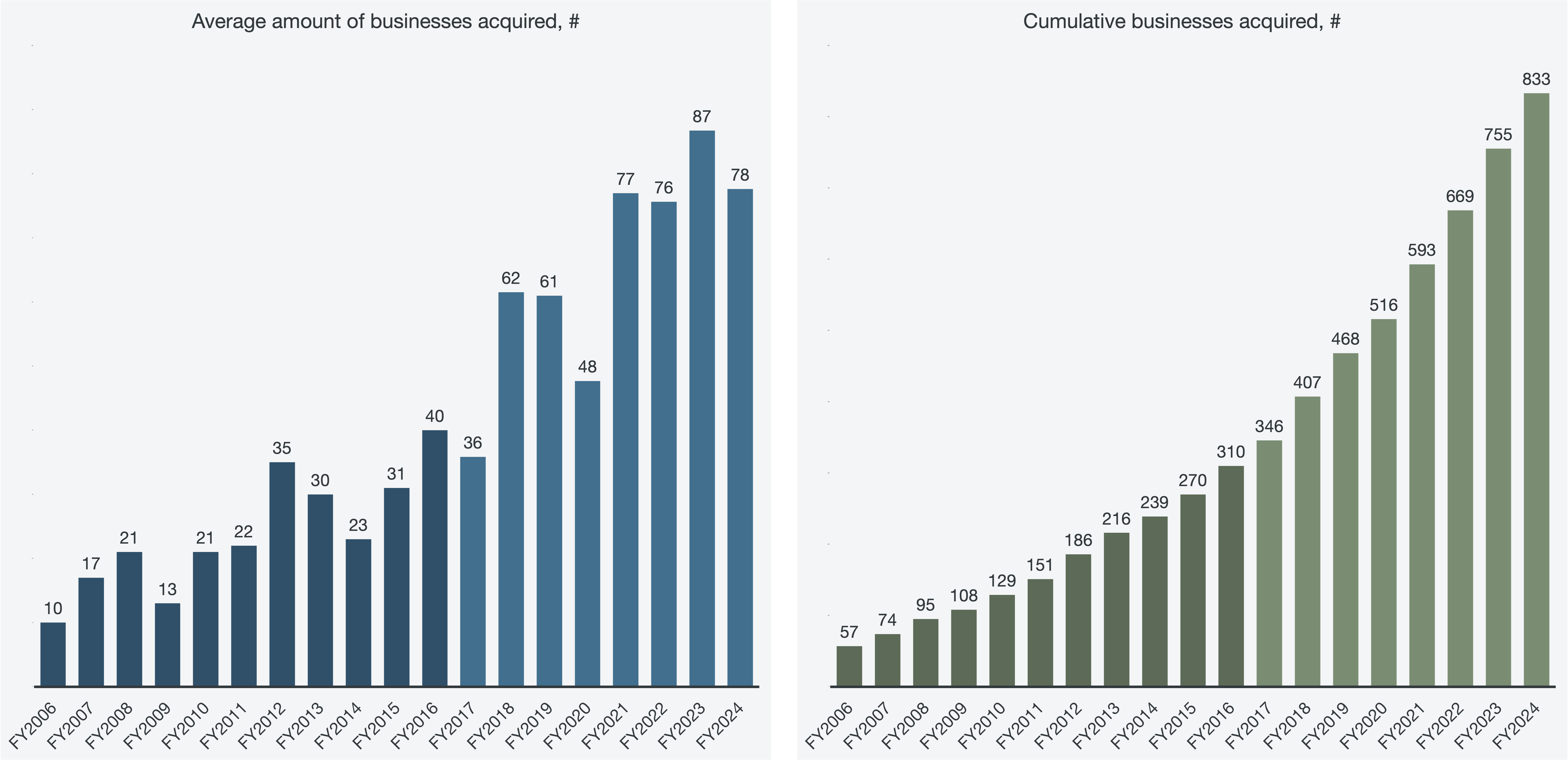

Figure 2, 3: Businesses acquired per period and cumulative overview (calculated post 2017)

Cumulatively, I estimate that Constellation has acquired over 800 businesses as of 2024. I derive that by assuming an average price per acquisition based on historical averages, divided by the aggregate net cash consideration. The average acquisition cost assumed starts at $7.5 million in 2017, rolling up to $12.3 million in 2024.

While the cumulative chart looks impressive, the average amount of businesses acquired per period has stagnated and stayed relatively static the past four years. As mentioned, the business model may scale infinitely simply by expanding the number of operating groups and BUs. However, the VMS market itself does not have enough high-quality businesses to sustain an accelerated pace much beyond ~100 businesses per year. Management has commented on the funnel being of lesser quality in recent times, making it more and more difficult to acquire businesses that meet the hurdle rate.

The future of the business

To combat a deteriorating pipeline and funnel of small- to mid-size VMS, Constellation has started targeting large VMS businesses as well, in addition to experimenting with the acquisition of companies outside of VMS. Both of these strategies pose their own individual challenges, though.

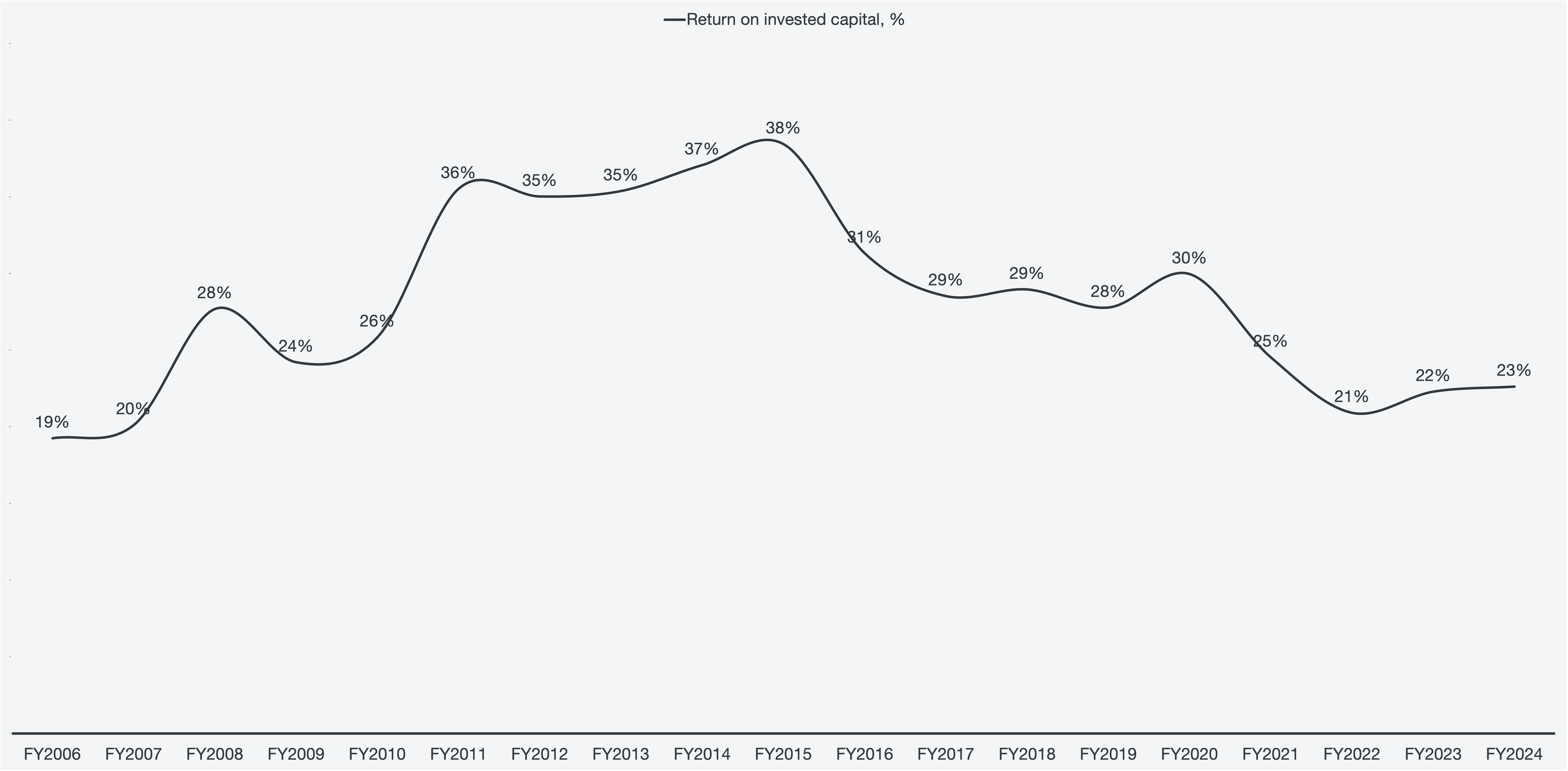

In regard to large VMS, there have been 5 large acquisitions since 2021, which is also when ROIC started to plummet. The primary reason large VMS is less appealing as an acquisition target is because private equity firms bid in auctions for them, inflating the prices. This inherently makes it much more difficult to find and acquire a business while meeting the same hurdle rates as a small- to mid-sized VMS.

Figure 4: Return on invested capital

In a 2021 president’s letter to shareholders, Mark Leonard shared as much:

If we are successful in acquiring one or investors’ capital will decrease, two large VMS businesses per annum, then I anticipate that CSI's return on but we will not have to return any of our free cash flow to shareholders.

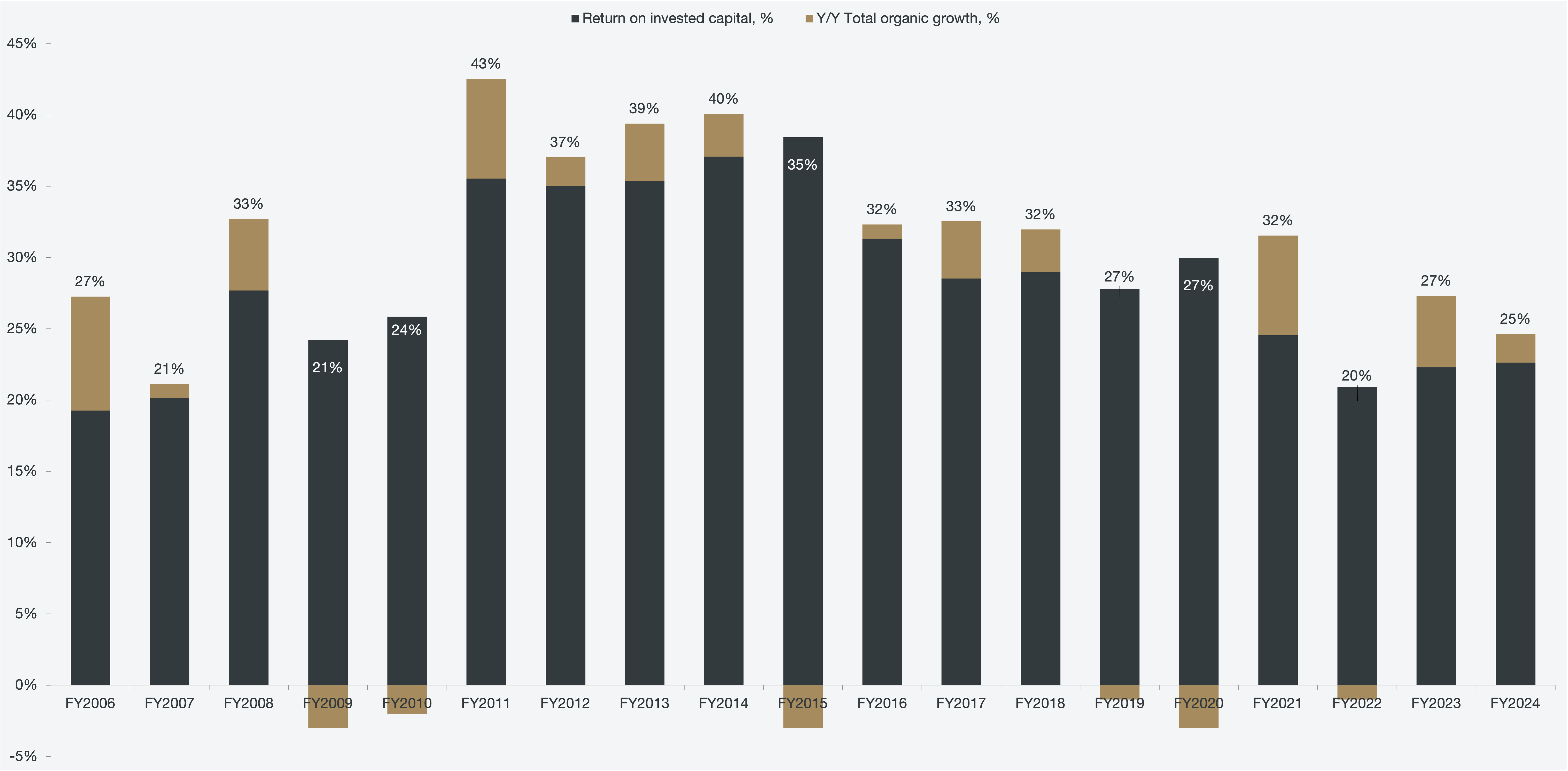

So, what is the hurdle rate? The founder and director, Mark Leonard, outlines a “combined ratio” as the single most useful way to track the health and sustainability of the business. Mark Leonard’s combined ratio should not be confused with the combined ratio used to measure underwriting profitability in insurance companies. Mark Leonard’s combined ratio is defined as follows:

The healthy level that signifies that the current business model is working is a combined ratio of ~25%. If ROIC is kept above 20% while organic growth is in the mid-single digits, then the reinvestment engine is alive and well. ROIC measures the cash returned from acquisitions, which is typically shareholder’s equity plus accumulated amortization, as Constellation utilizes limited amounts of debt. Organic growth is the growth from existing businesses, excluding contributions from acquisitions.

The combined ratio measures Constellation’s performance from both a profitability and growth perspective, without requiring significant additional capital. To minimize short-term noise in the numbers, the combined ratio could be read on a rolling 5-year basis as well.

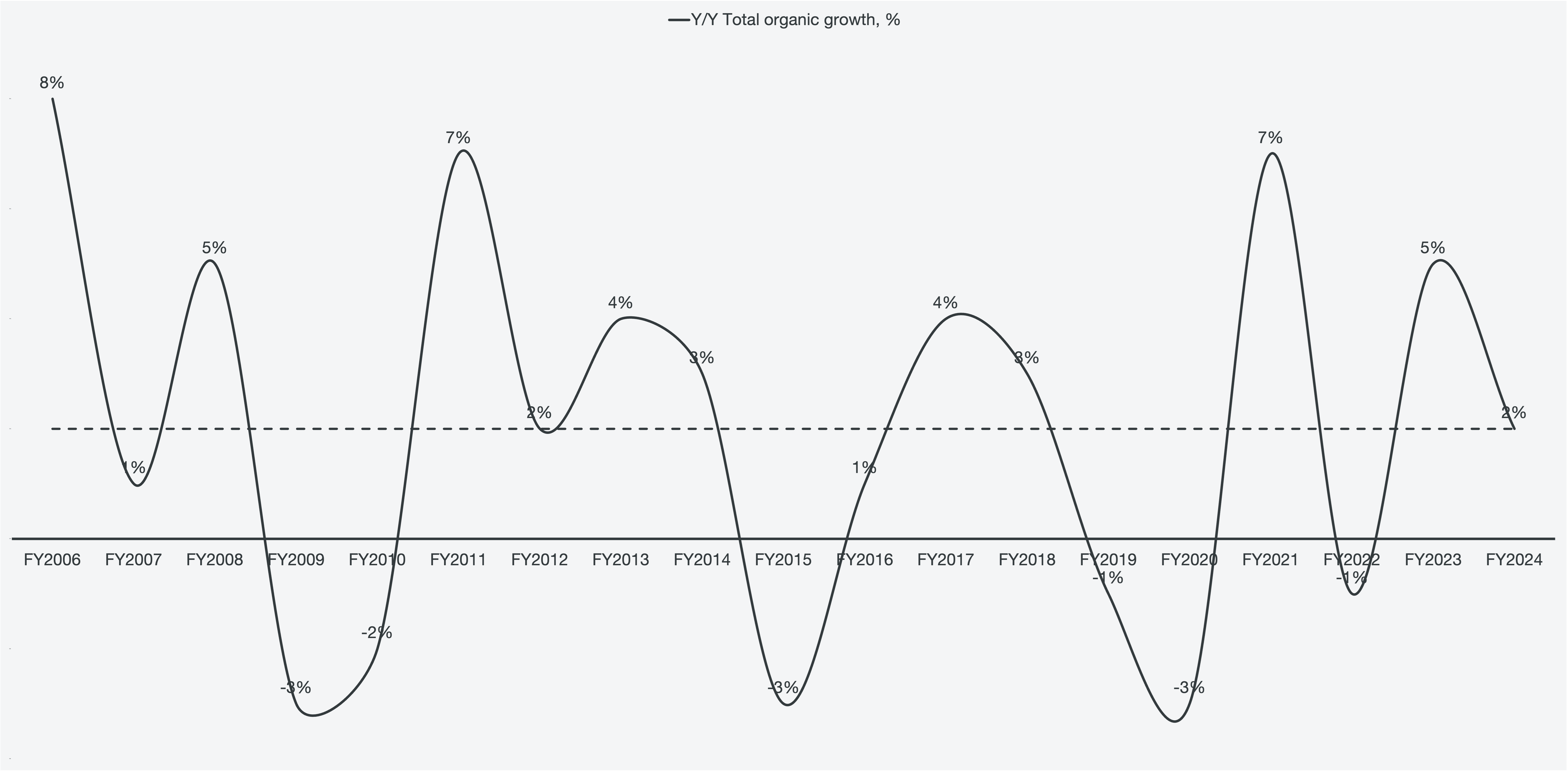

The organic growth rate varies drastically from period to period, and that is the case throughout all stages of growth. The average organic growth rate since 2006 is 2%, which is where the organic growth rate is for FY2024. This implies that the acquisition pipeline still has businesses of historically comparable quality.

Figure 5: Organic growth

Looking at the combined ratio, it is still at a level that implies that the acquisition engine is working. The overall goal is to avoid having to return free cash flow to shareholders, and that is only the case as long as the hurdle rate is met. In periods when Constellation did not find attractive enough acquisition targets, they issued special dividends. However, shareholders and management generally agree that the capital is better spent by Constellation rather than having it be returned.

Figure 6: Combined ratio

In addition to targeting larger acquisitions at the cost of ROIC, it is also known that Constellation is looking to expand beyond just VMS. The following was mentioned by Mark Leonard in the president’s letter in 2021:

We are seeking attractive returns, a sustainable advantage, and the ability to deploy large amounts of capital outside of VMS. That will require highly contrarian thinking and is likely to be uncomfortable in the early going. Hopefully, we have built enough credibility to warrant your patience as we explore new and under-appreciated sectors.

During the 2025 AGM, Constellation positively noted that there have been experiments across a variety of business categories. This is a necessary step to develop the next leg of growth, but it also carries significant risk, as the management’s expertise and experience is in VMS. It is likely that ROIC will suffer in coming periods as a mix of large VMS and other business categories are being acquired before the acquisition formula gets refined.

While expansion of the scope is a risk, there is also a risk brought by AI. Constellation is an operator and partner that sells highly customized software and services to niche, mission-critical environments. AI could serve as an opportunity that accelerates integrations and growth, but it could also be the case that AI automates the tasks handled by VMS. This could deteriorate the value and organic growth of the BUs or, in some cases, even make them obsolete. AI lowers the barrier to developing new solutions, which could thin out the pipeline or create competitive alternatives faster and cheaper. However, AI is more likely to disrupt broader horizontal software rather than niche vertical markets, but it is worth tracking as a key risk.

Cash generation and operational discipline

A common way to identify a high-quality business is by reviewing its capital discipline and predictability. Constellation's margins have stayed consistent for two decades, despite the business growing revenues from $200 million to $10 billion. A majority of the operating costs are staff expenses, which makes sense given the M&A strategy. Since 2010, the staff operating expenses are ~53% as a percentage of revenue on average. In 2024, it was recorded at 53%, which speaks to the operational discipline.

Figure 7: Staff operating expenses and total revenues

The discipline in demanding financial excellence through hurdle rates has also resulted in consistent, high-quality cash generation for the business. Operating margins and free cash flow to the firm margins have remained consistently high throughout the businesses’ history.

Figure 8: Operating margins and free cash flow to the firm margins

Intrinsic valuation

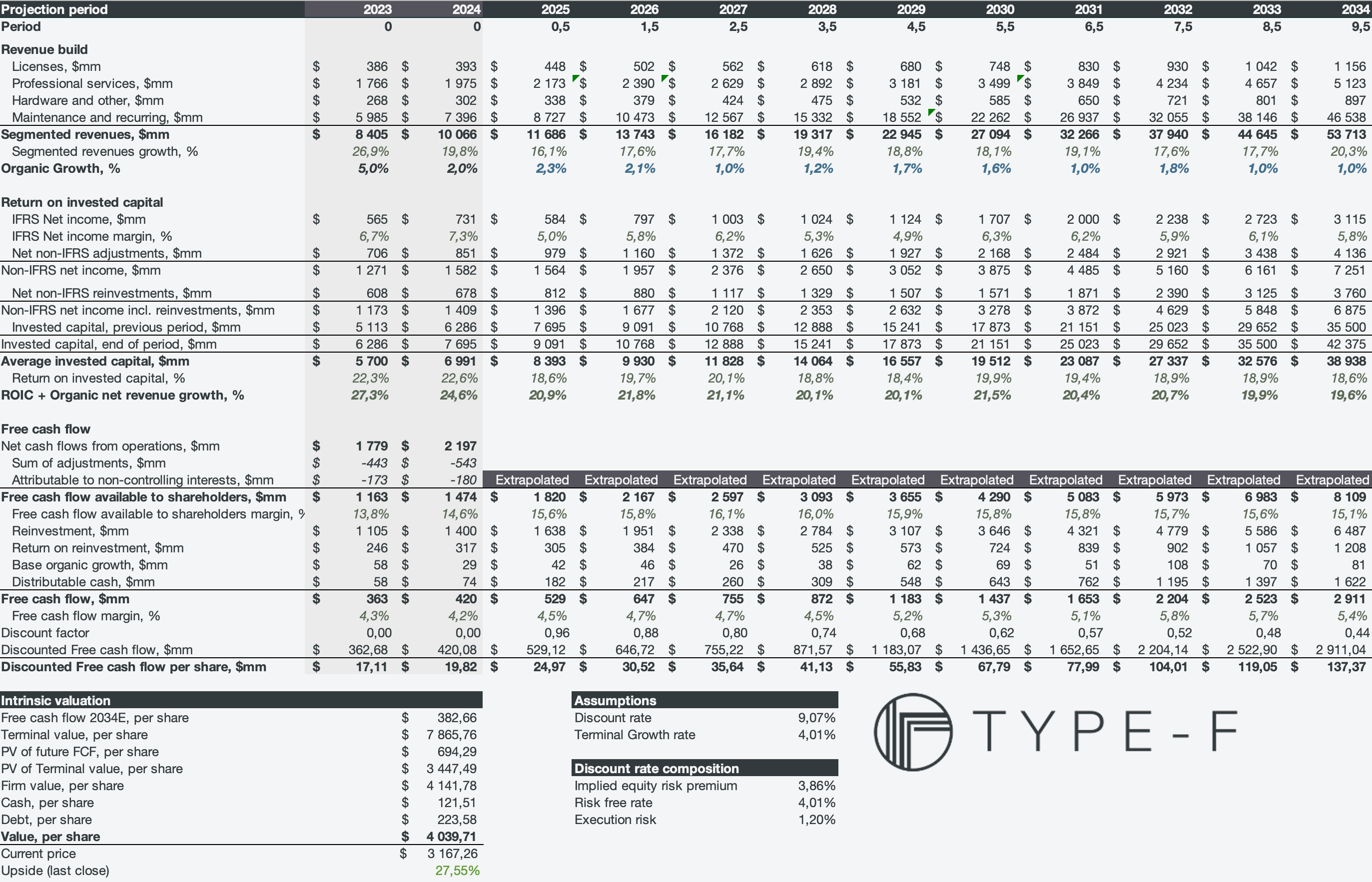

Valuing Constellation Software comes with several challenges. The model has to capture the reinvestments required to drive intrinsic value creation, which also means that acquisitions have to be accounted for. My approach to valuing Constellation is a multi-stage framework that projects future FCF available to shareholders (FCFA2S) based on the prior period’s FCFA2S, while factoring in ROIC and organic growth from the current FCFA2S. The model assumes that Constellation will find it increasingly harder to reinvest all of its FCFA2S over time, which is instead accounted for as distributable cash. After reinvestment, the resulting FCFF is the sum of distributable cash, organic growth, and ROIC on the reinvestment.

Assumptions:

Discount rate: 9.07%

(3.86% ERP, 4.01% Risk-free rate, 1.20% Business specific risk)

Terminal growth rate: 4.01% (10-year US Treasury yield proxy)

Table 1: Discounted cash flow model, $ millions

My narrative translates to a Constellation Software that will drift towards 20% ROIC, which implies that the deteriorating small and mid-size VMS pipeline will be increasingly replaced by larger VMS deals and other software categories. The reinvested portion and distributable cash split begins at 90/10 and becomes 80/20 towards the later forecasting periods. Organic growth represents a decreased quality in the VMS pipeline over time.

The business-specific risk (execution risk) is reflecting the unknown results of Constellation’s expansion into other software categories.