FICO: The Most Unfair Business In The World

Initiating equity research coverage

FICO is the poster child for wide-moat, high-quality compounding businesses with immense pricing power and robust margins. FICO’s score business in particular is of extremely high margins and boasts over 95% market share, despite competitors handing out their services for free. However, recent news headlines have provided a very rare opportunity to purchase FICO below fair intrinsic value. That is one opportunity that I am not missing out on.

Company profile

17 August, 2025 Initiated coverage

Direction: Buy

Previous fair intrinsic value: N/A, as of N/A

Symbol: FICO, Exchange: NYSE

Sector: Technology, Industry: Software - Application

Theme: High quality

Fair intrinsic value: $1595.16 (19%), as of August 17, 2025

Market capitalization: $33 008 million

Pricing data: P/S 17x, P/E 52x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

Scores is the best business model in the world

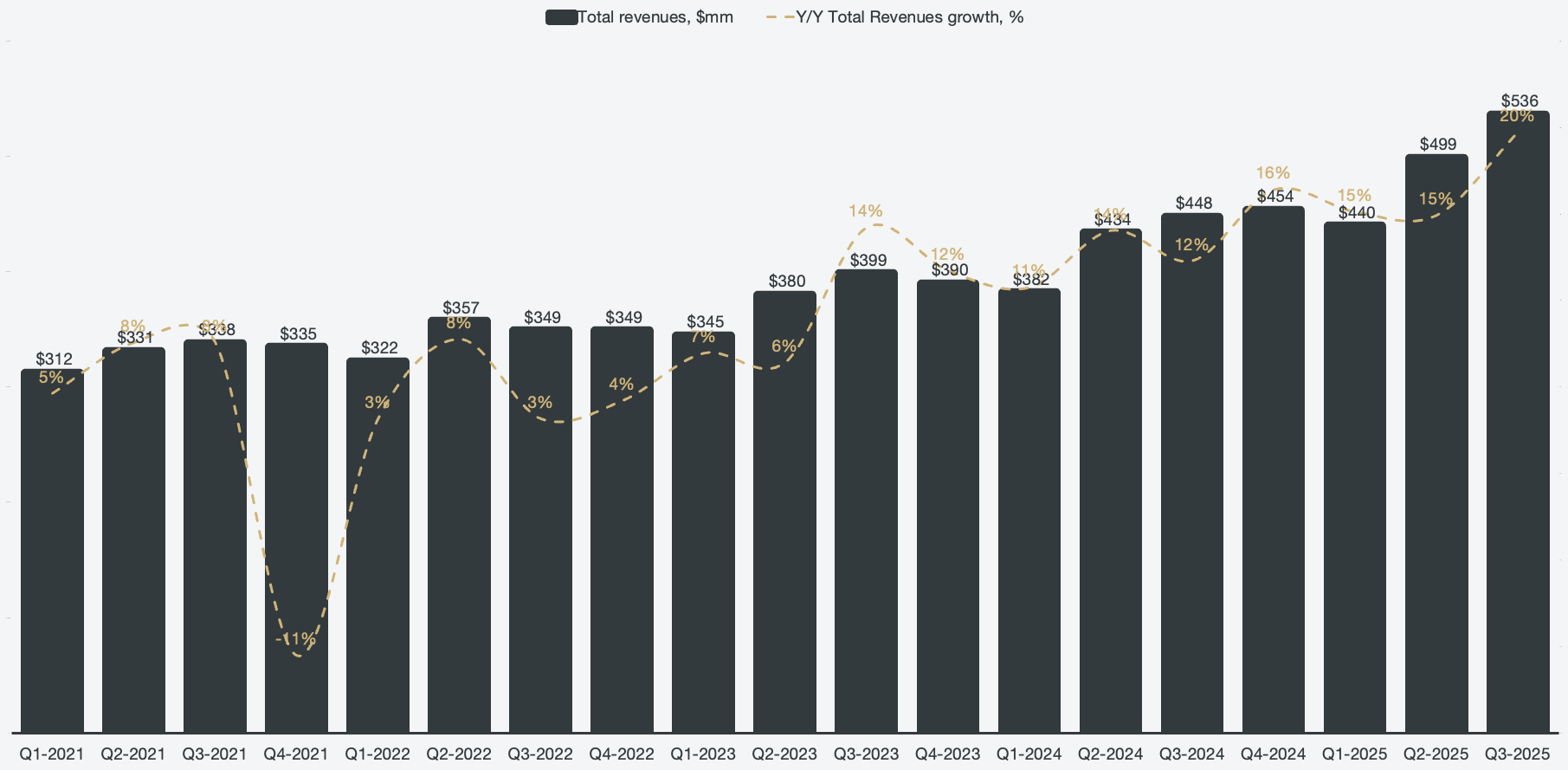

FICO operates two main lines of business: a scores and a software segment. For a century, FICO only had consumer credit ratings (FICO scores) and lacked organic growth. The operating margins were always impressive, but FICO was beholden to the credit markets. If the credit markets were moving slowly, so too were FICO’s earnings results. However, FICO has added a software segment, which drives organic growth. Together with the stability and extremely high margins of its score segment, a beautiful dynamic is created where FICO can derive revenue growth organically without being as exposed to cyclicality.

Figure 1: Total revenues and revenue growth

Scores are comprised of consumer credit scores. FICO scores are used to assess credit risk for consumer loans such as mortgages, credit cards, and auto loans. Scores are split into business-to-business (B2B) and business-to-consumer (B2C) segments, where B2B accounts for a majority of revenues within the segment. B2B score recipients include banks, credit card issuers, insurers, retailers, various lenders, and reporting agencies. The B2C segment is primarily comprised of myFICO.com offerings.

In short, FICO scores are mathematical models designed to assess credit risk. FICO itself does not own or store consumer credit data; instead, it licenses its scoring algorithm to the credit bureaus. The bureaus apply FICOs model to consumer credit files that they maintain, and the resulting FICO score is then sold to lenders.

Figure 2: Segmented scores revenue

While the scores segment historically lacked organic growth, that does not mean that scores did not grow. The consumer credit markets are compounding at mid- to high single-digit for the coming 10 years, which serves as a solid backbone of growth. In addition, FICO has immense pricing power, which the company has been showcasing as of late. By further developing the credit scoring model, they are retaining a monopoly as the de facto golden standard of credit risk assessment on the consumer side.

When asked about FICOs scores market share, FICO management pointed to third-party estimates of it being in the high 90s range, essentially a monopoly.

It's in the high 90% range. So it's hard to come up with exact numbers on this because it's not really reported anywhere. But from third parties that have done the actual work on this, it's a pretty high number.

Steve Weber, Chief Financial Officer

Fair Isaac Corporation, Q3 2025 Earnings Conference Call

Figure 3: Scores growth

FICO did not leverage its pricing power for decades, until 2018, when FICO began raising royalties on mortgage score pulls. Historically, the base FICO score royalty per score was assumed to be ~$0.60 for close to three decades. In 2025, royalties are fixed at $4.95 per score for mortgages; that represents a ~725% increase. In 2024, score costs were fixed at $3.50 per score, representing a 41% year-over-year increase in 2025. On a tri-merge basis, that translates to $14.85 to FICO per loan today, versus only ~$1.80 in 2018 and prior.

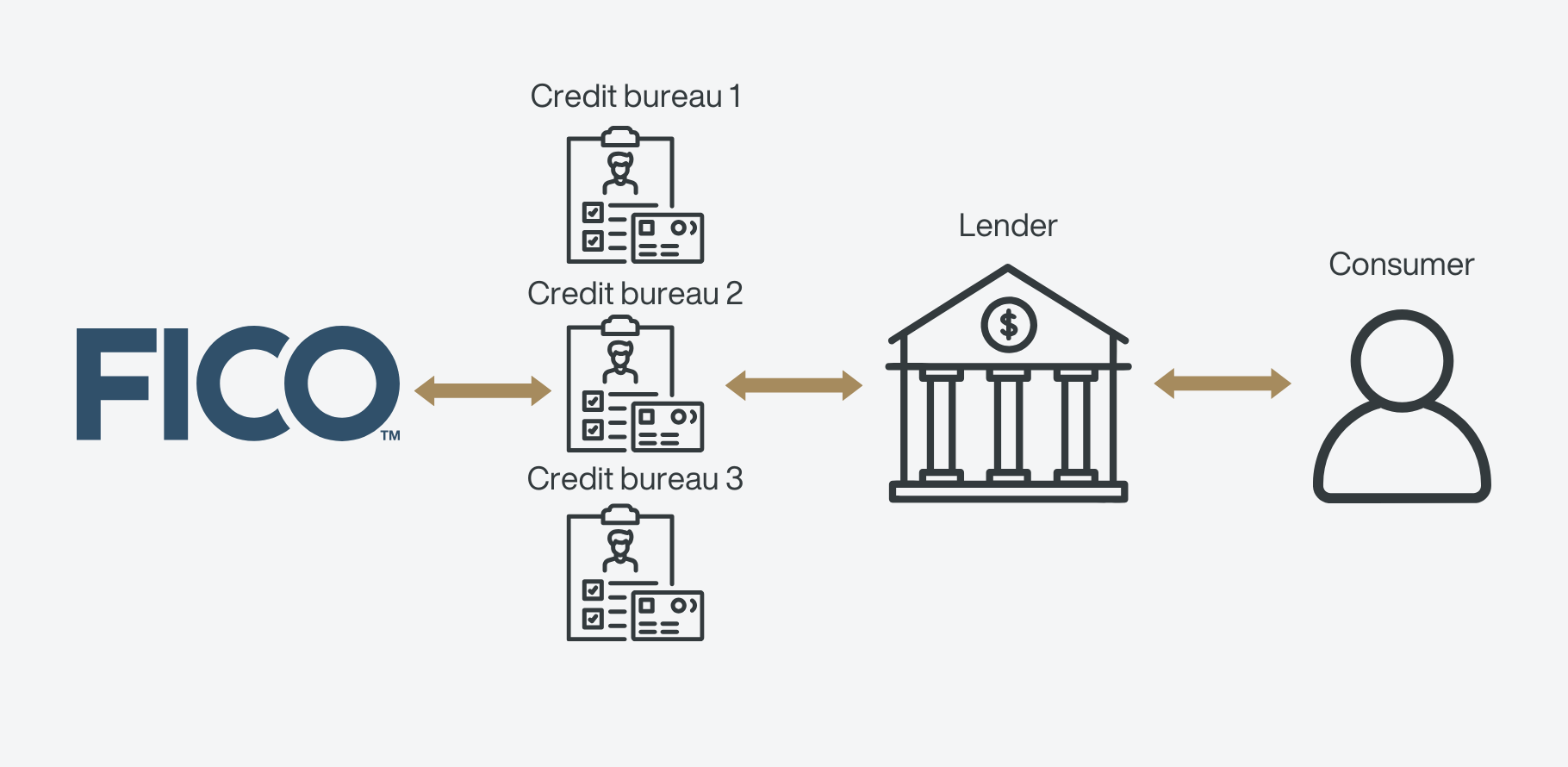

To understand why FICO has such immense pricing power, it’s important to understand the chain of credit scoring.

The consumer applies for a loan from a lender.

The borrower authorizes the lender (bank, credit union, mortgage broker, etc.) to pull their credit.

The lender requests credit reports.

For mortgages, this typically means a tri-merge report from all three major bureaus (Equifax, Experian, and TransUnion).

Credit bureaus license FICO’s scoring algorithm from FICO.

Bureaus take the consumer’s credit file and apply the FICO model to produce a FICO score.

The cost of pulling the consumer’s credit is embedded in the closing fees. When originating a mortgage, a score pull represents a tiny fraction of overall mortgage costs. Whether the royalty is $1.80, $10.50, or $14.85 on a tri-merge basis per mortgage, it is immaterial compared to thousands in closing fees. This is why FICO has been able to increase royalties so aggressively, and why I believe they have a lot of room to further increase them in the future.

Figure 4: Scores chain

There will always be periods of weak consumer credit markets, and finding ways to leverage FICO’s moat will help mitigate market cyclicality. While sheer pricing power is one key aspect to increasing revenues during cold credit markets, another way is to further increase the value proposition. FICO scores are the golden standard for assessing consumer credit risk, and FICO continues to refine scores to be more predictive and expand coverage into additional markets and verticals.

…I mean if you're in the business of measuring risk, and you benefit when you reduce the risk and you suffer when the risk comes home to roost. You want the most predictive score. You want to avoid as much credit default as possible. That's what you achieved with FICO 10 T. And with respect to FICO classic, I would say, it's also very, very good. And it's not very good for a 20-year-old score. It's very, very good in absolute terms […] All the models, everything is optimized around it. And that's truly the moat. It's not some government-conferred monopoly. That's not what makes it successful.

William Lansing, Chief Executive Officer

Fair Isaac Corporation, Q3 2025 Earnings Conference Call

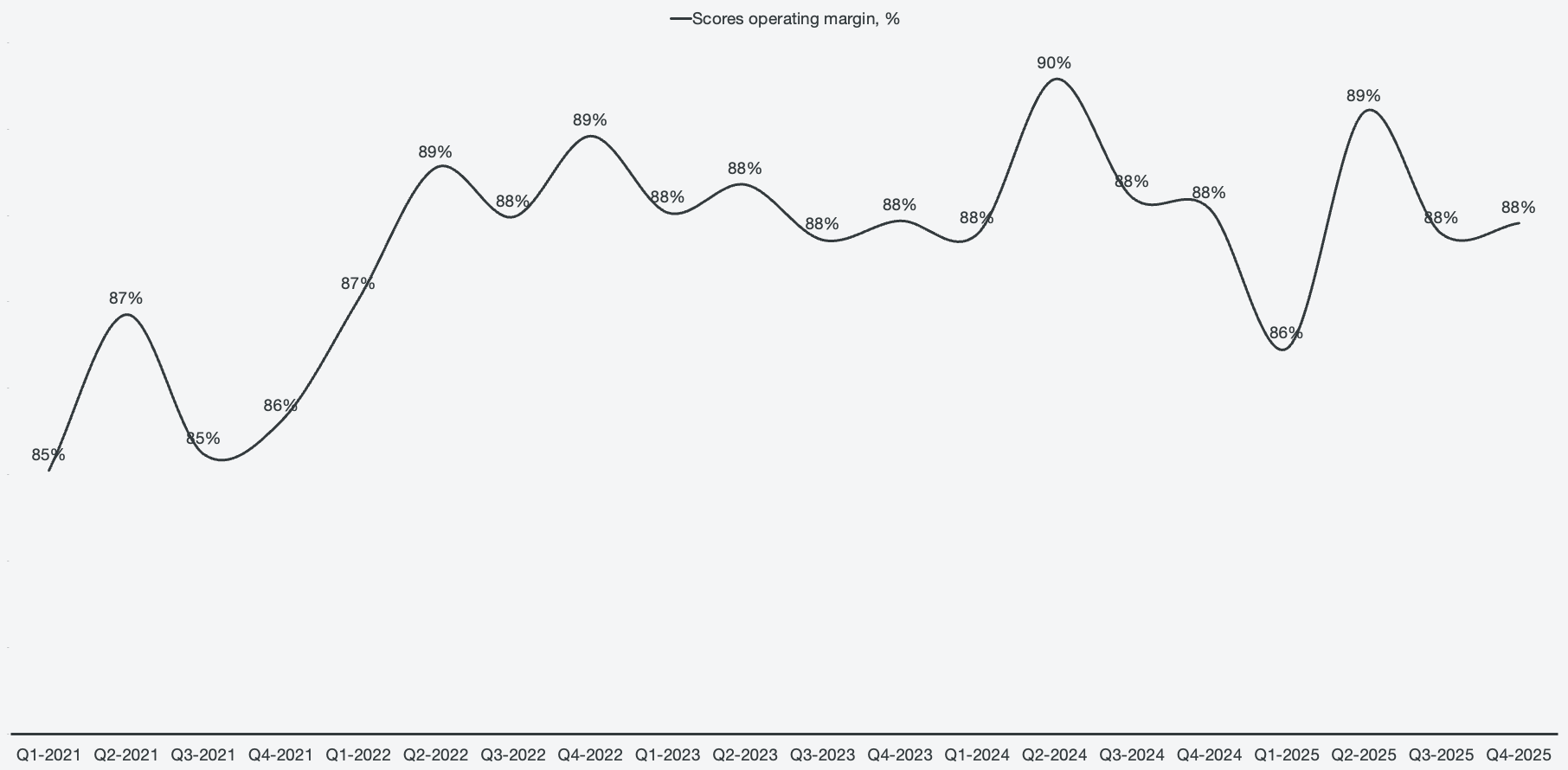

What truly makes the scores segment special are the margins. FICO scores have exceptionally high margins, since there are essentially minimal operating costs associated with providing the mathematical model to credit bureaus when a score is pulled. Unlike S&P Global (NYSE:SPGI) and Moody’s (NYSE:MCO), FICO does not need researchers to compile credit reports, which is why FICO can boast immense margins.

Figure 5: Scores operating margins

Software is the untold growth story

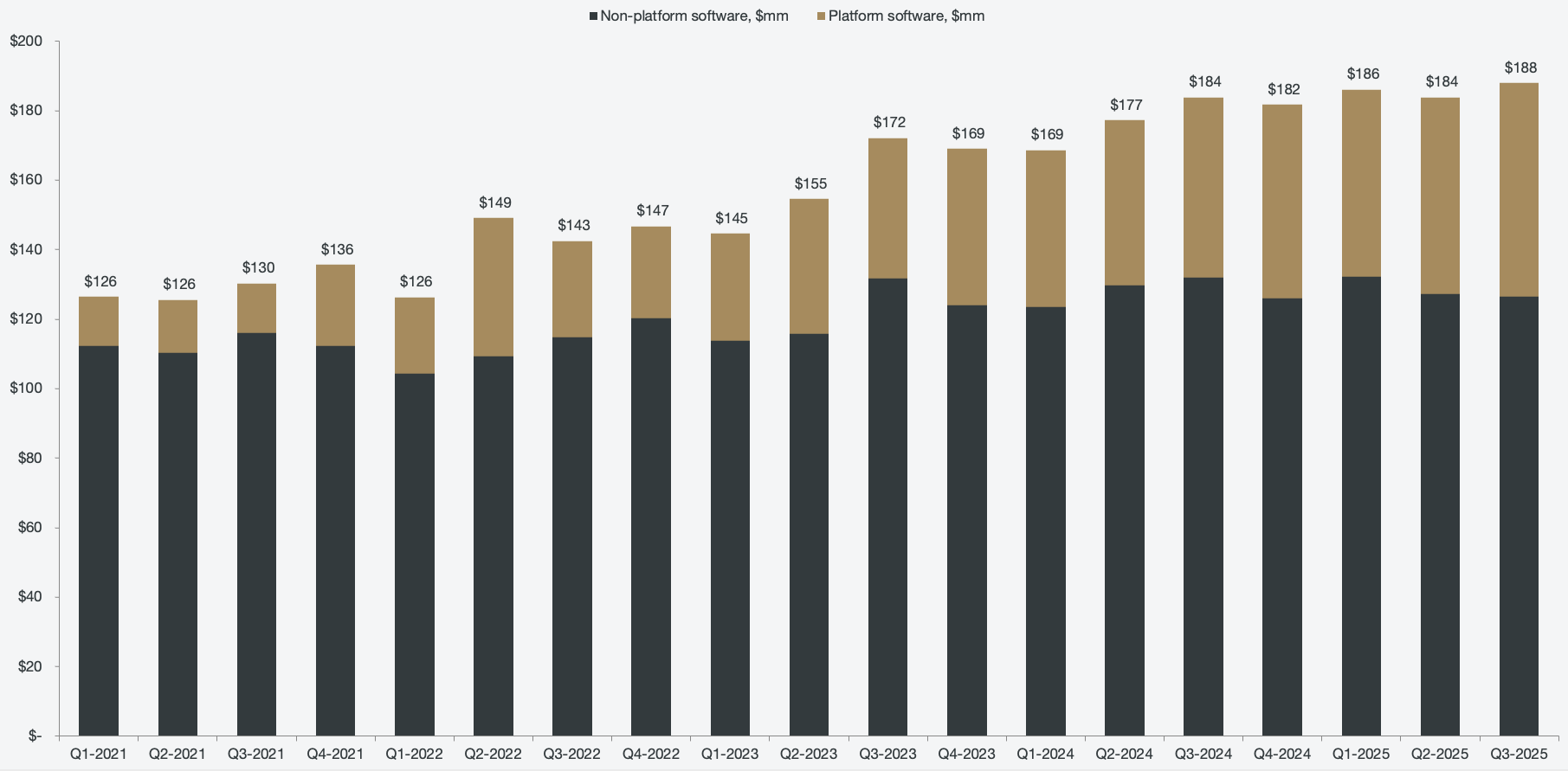

The other business segment besides scores is the software business. Depending on the cycle of credit markets, software accounts for roughly half of FICO’s revenues in recent years. The software segment can be divided into two categories: Platform and Non-platform.

Figure 6: Segmented software revenue

The FICO Platform is a cloud-based decisioning and analytics platform. It’s essentially a unified environment where enterprises can ingest data and apply FICO’s models for credit risk, fraud detection, marketing, and compliance to serve as a basis for decision-making. The FICO Platform can apply advanced analytics and AI, execute real-time rule-based decisions and workflows, and support outcomes like simulations and feedback loops.

The FICO Platform was introduced around 2019 in order to shift customers to a unified, cloud-based ecosystem, with the goal of driving organic growth. The FICO Platform has pricing tied to usage and employs a “land and expand” strategy, not unlike Palantir.