Mercado Libre: Built The Rails, Now Renting Them Back

Equity research report

Famously known as the Amazon of Latin America, MercadoLibre is a well-positioned business to assert the same kind of dominance that Amazon has in the past. MercadoLibre is thoroughly integrated across the region as the operating system for commerce and money, and is not only rapidly expanding its revenues, but also its market position amidst a tough competitive landscape.

It is doing so while deliberately investing through near-term margin to reap the rewards from structural levers in the future. A high-margin advertising segment, improved logistics economics, and a maturing credit portfolio are investments that will blossom from near-term hits to margins. The company is also increasingly spreading to more verticals, spearheaded by sharp management that has been executing and outcompeting the opposition in the region for decades.

Company profile

Theme: Commerce and fintech ecosystem, Direction: Buy

Symbol: MELI, Exchange: NASDAQ

Sector: Consumer Discretionary, Industry: Internet Retail

Fair intrinsic value: $3 394 (103%), as of June 28, 2026

Market capitalization: $84 923 million

Pricing data: P/S 2.67x, P/E 44x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

The monetization ladder

Looking at the revenue segments, it would be easy to assume that the business is split across two core segments: commerce and fintech. In absolute terms, there are indeed two core segments, but a better way to view MercadoLibre is through the lens of a monetization ladder applied to the users.

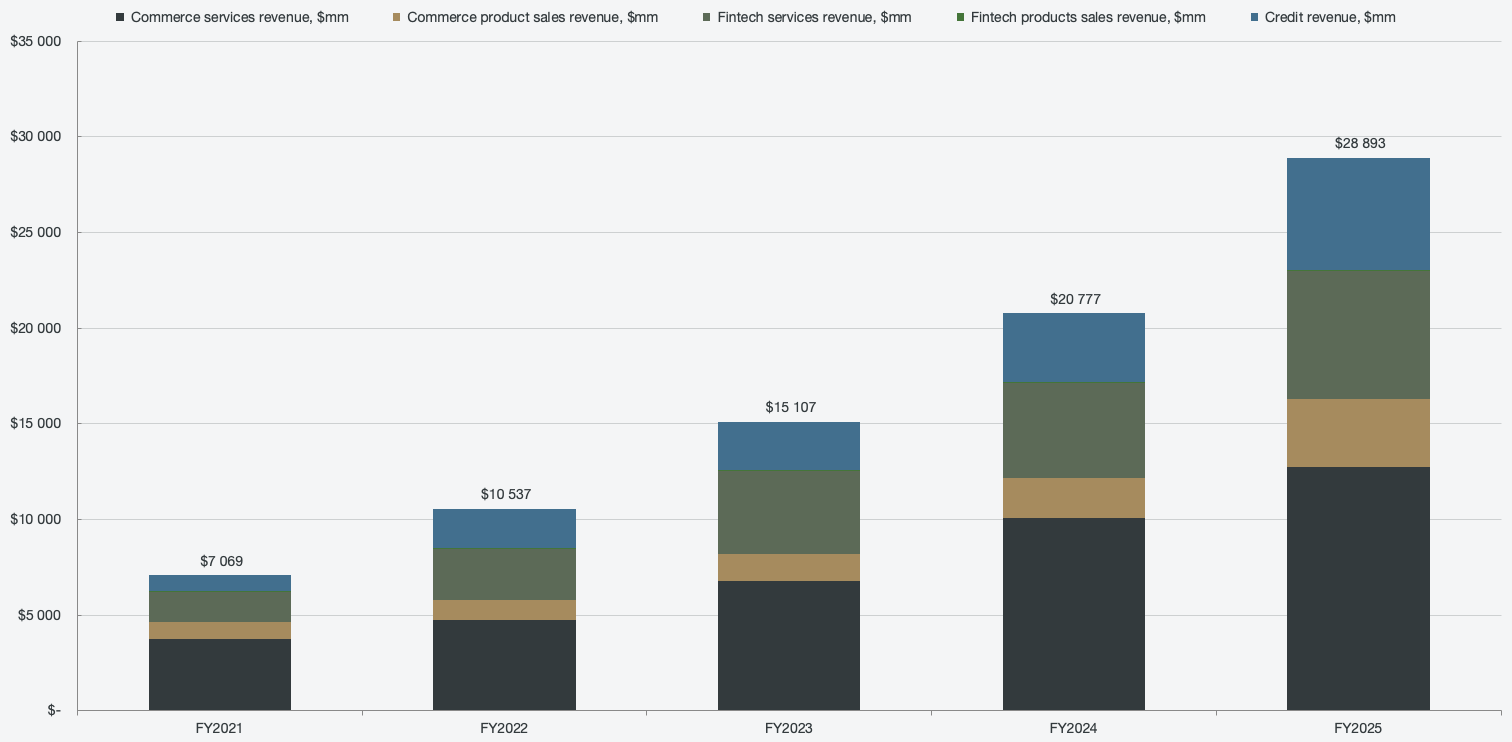

Figure 1: Segmented revenue

In a sense, MercadoLibre has built the rails and is now renting them back to an entire economy. Comparing MercadoLibre to Amazon is fair in the sense that both encompass entire ecosystems in the commerce space and are ambitious across layers. The offerings are comparable as well: both offer a marketplace, logistics services, payment solutions, subscriptions, and advertising. However, the paths diverge when it comes to core details. For one, the profit engines are vastly different. Amazon’s profits are carried by AWS, while MercadoLibre uses its consumer fintech as its second engine. MercadoLibre lacks the cloud, and Amazon has to lean on external banks and cards. Another large differentiation lies in how the businesses have grown. Amazon has been scaling on top of existing infrastructure, such as reliable carriers, credit bureaus, and ubiquitous credit cards. MercadoLibre operated in geographies where such things didn’t exist, and as such, it had to build payment ecosystems, credit, and logistics. MercadoLibre is structurally more vertically integrated out of necessity.

The result of MercadoLibre’s effort is a monetization ladder, where each step adds another stream of revenue from the same customer, increasingly at a high margin. Running steps at a loss is a good trade-off, as long as it feeds the higher margin ones. MercadoLibre doesn’t just aim to make money from a customer once; it aims to have the same customer spend money over and over, throughout various layers. Each step of the ladder is a way for MercadoLibre to make money from the same customer.

The first step of the ladder is the discovery and transaction step: the marketplace. The marketplace is the core of the cash source, where sellers pay MercadoLibre a commission on their sales. What follows is the shipping and fulfillment step. The logistics step is often subsidised to win volume, and can even be seen as a deliberate loss-maker, but the trade-off is well worth it. It buys frequency and trust, which enables steps three and four. Every time a customer pays with Mercado Pago (both on and off the marketplace platform), MercadoLibre keeps a yield on the transaction. When customers then park a balance in Mercado Pago, the company gains a cheap and sticky source of funding for the credit portfolio. When the customer uses the credit card or takes out a loan, the company earns interest at a high margin.

The fifth step involves monetizing customer attention at near 100% margins. Sellers pay MercadoLibre to promote products to the customers, and since those customers are already on the platform, almost all of that money is profit. The final step involves retaining the customer and turning them into subscribers. When customers subscribe to MELI+ for free shipping and streaming, or to earn loyalty points, it incentivizes them to keep coming back and keeps them sticky.

A customer may not be profitable on their first purchase, but the same customer, over time, as they start using the Mercado Pago card, hold a balance in Mercado Fondo, carry a loan, and click sponsored listings while staying a subscriber to Meli+, the customer becomes highly profitable. The monetization ladder is meant to monetize a customer’s lifetime, not a single transaction.