Nvidia Corporation: The Most Important Company In the World

Initiating equity research coverage

The world’s largest publicly traded company conquered perhaps the most significant secular tailwind that we will witness in our lifetimes. Nvidia has played a pivotal role in advancing AI by serving as the go-to vendor for training models. It is not by chance; Nvidia has consistently been an early mover in several large, groundbreaking industries, often resulting in winner-takes-most scenarios.

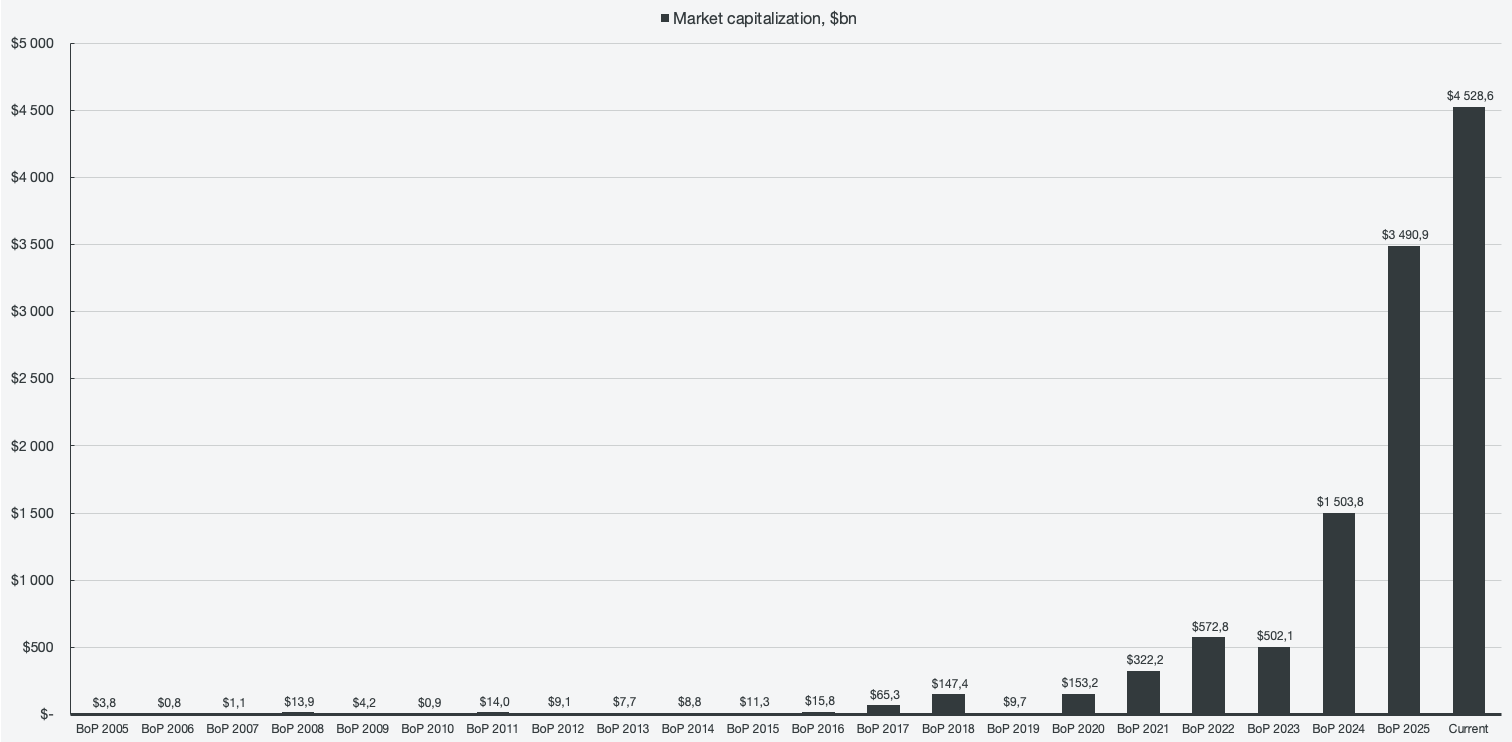

Figure 1: Nvidia Corporation market capitalization

As evident from the market cap expansion, it has been an explosive ride since the launch of ChatGPT. The question is, for how long can it continue?

Company profile

February 18, 2026 Initiated coverage

Direction: Buy

Previous fair intrinsic value: N/A, as of N/A

Symbol: NVDA, Exchange: NASDAQ

Sector: Technology, Industry: Semiconductors

Theme: AI Hardware

Fair intrinsic value: $210.44 (14%), as of February 18, 2026

Market capitalization: $4 528 621 million

Pricing data: P/S 24x, P/E 46x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

Not by coincidence

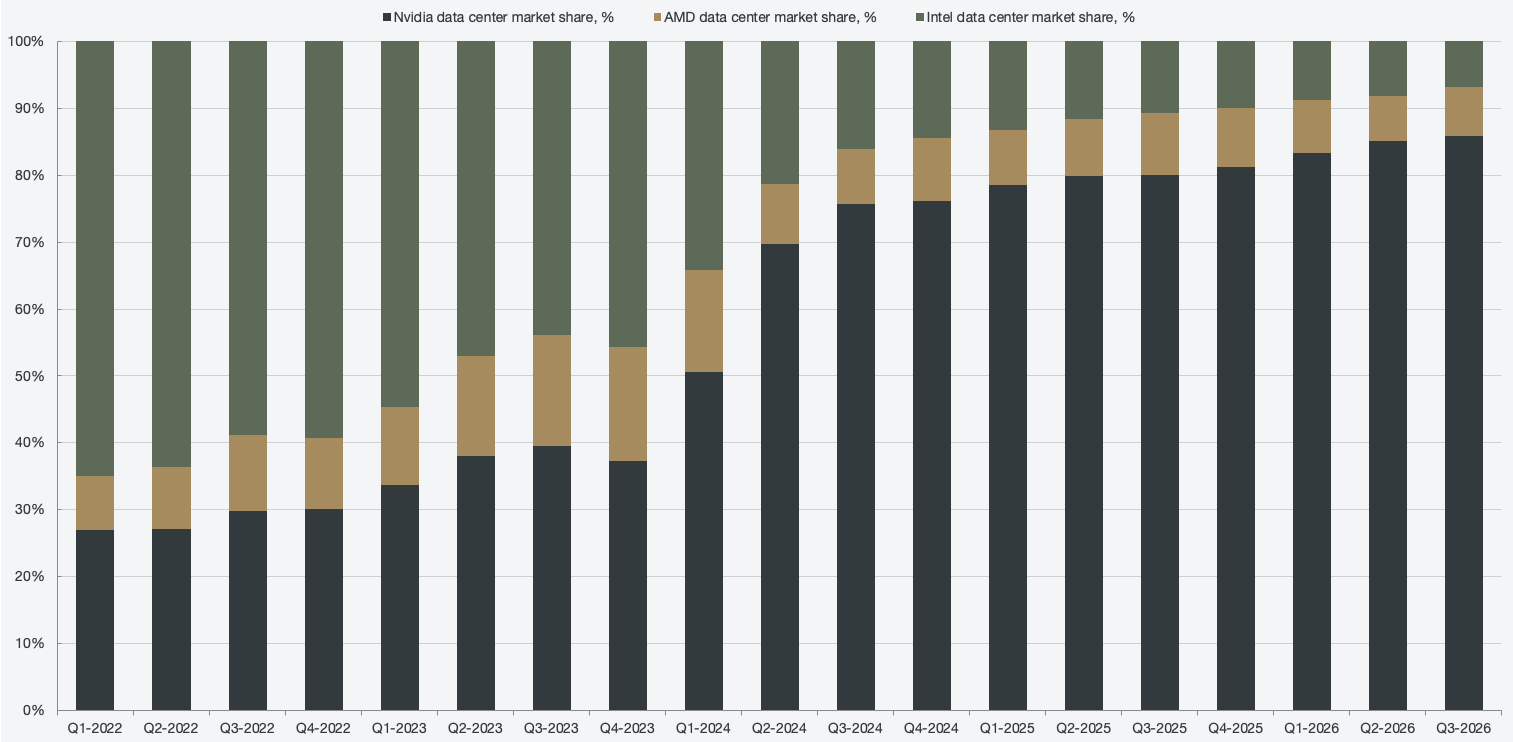

Nvidia has built dominance time and time again by being the first mover into new markets. The company was founded in 1993 with the goal of bringing 3D graphics to the consumer PC market. With the release of the GeForce 256, the term “GPU” was coined for the first time. Since the company’s inception, they have held a dominant share of the gaming market. They were first to release semiconductors aimed at crypto mining, capturing a majority of that market itself. Now, after the launch of ChatGPT, they also pivoted the whole business and have since gained a dominant market share in the data center segment.

Figure 2: Data center market share distribution

ChatGPT launched in 2022 and triggered a structural panic across the whole tech industry. Hyperscalers began expending capital as if their survival depended on it in order to train and run large language models (LLMs). Nvidia was the first to pounce on the secular tailwind, and they never let go of their grip. The way Nvidia managed to dominate can be attributed to several factors, none of which are mere luck.

Data centers historically ran on CPUs, which are built to solve sequential problems one at a time. GPUs are inherently unsuited for data center workloads as they are meant for rendering, not solving complex problems. What GPUs thrive at, however, is solving many simpler tasks simultaneously. LLM training involves many simple matrix multiplications that have to be solved, something CPUs are very inefficient at. This was when the market realized that they needed parallel processing, and Nvidia was the most sophisticated parallel processing hardware that was available in the market.

The most significant reason that Nvidia has managed to retain its dominance is its Compute Unified Device Architecture (CUDA) platform. It allows programmers to use GPUs for computing, not just game rendering. Nvidia has been making CUDA available to researchers and universities for over a decade, which has resulted in a majority of available open-source AI libraries, math frameworks, and deep learning models being specifically written for CUDA. Having CUDA created a deep moat and makes customers reluctant to switch to a different vendor, as it would entail rewriting many years of code from scratch.

Nvidia is relentless in its ambition; it doesn’t merely stop at semiconductors. In 2020, Nvidia acquired Mellanox to develop its NVLink product. NVLink is a proprietary technology that allows multiple GPUs to process as a single, efficient cluster. When a hyperscaler places a large order of GPUs, they can’t buy loosely from various vendors; they need an integrated system. Nvidia has managed to not only supply the semiconductors for AI training but also the networking capabilities, server architecture, and the software stack as one complete package.

There was no time in the AI arms race to wait for AMD and Intel to catch up, since Hopper was already available. This made the inbound volumes at Nvidia explode, and the hyperscalers were insensitive to price. By the time there were equivalent offerings from competitors, Nvidia had already absorbed a majority market share and was on to the next generation.

The culmination of the AI revolution so far

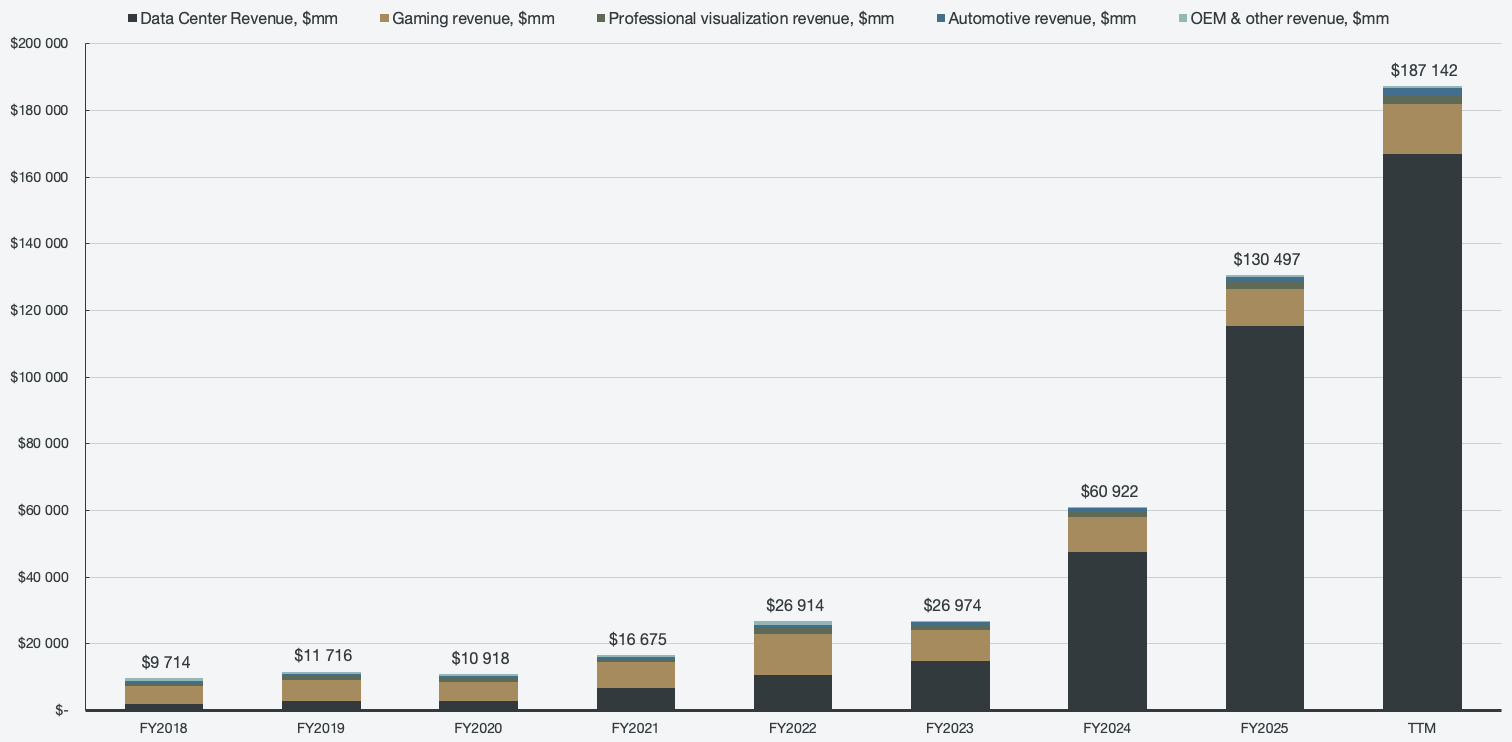

The unprecedented demand in an explosively growing market has allowed Nvidia to reap the rewards drastically. After a flat year in 2023, Nvidia grew revenues >110% for two years in a row and is close to having increased total revenues by 10 times over three years.

Figure 3: Segmented revenue

In April of 2021, data center revenue made up 39% of Nvidia’s total revenues, a figure that has now reached 89% in the trailing twelve months. In terms of overall data center market share, Nvidia grew from 27% in April of 2021 to 86% at the time of writing. Over the same period, competitor AMD decreased from 8% to 7%, and Intel collapsed from 65% to 7%.

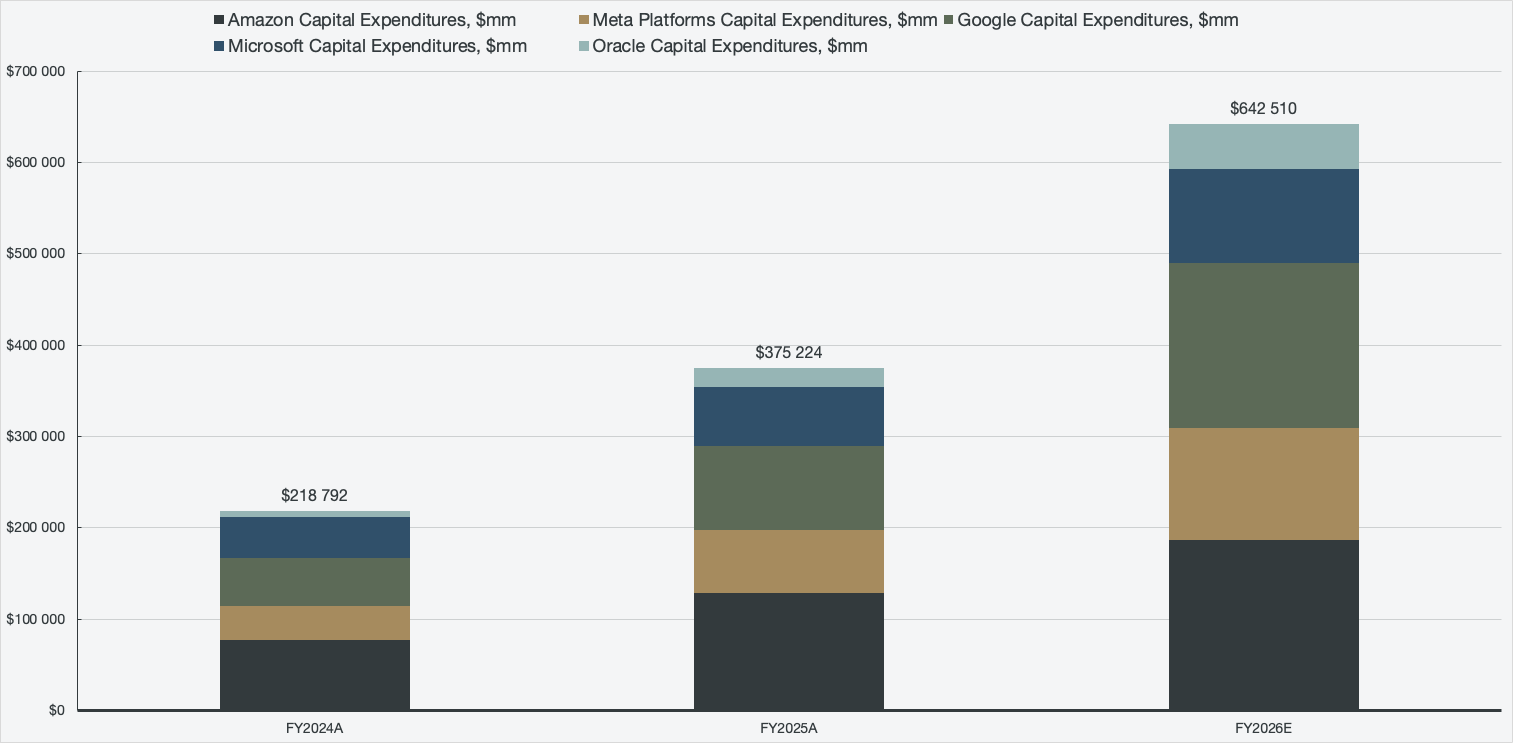

The money being poured into the semiconductor industry is largely attributed to the hyperscalers Meta META 0.00%↑ , Google GOOG 0.00%↑, Amazon AMZN 0.00%↑, Microsoft MSFT 0.00%↑, and Oracle ORCL 0.00%↑. The capital expenditures at these companies increased by 71% Y/Y in 2025 and are currently expected to increase by another 71% in 2026, totaling $0.64 trillion.

Figure 4: Hyperscalers capital expenditures

At the end of the day, someone has to pay for Nvidia’s semiconductors. Capital expenditures at these companies can’t triple every other year indefinitely. That is where the risks start to appear for Nvidia.