Palantir Technologies: I Was Wrong About Palantir, And So Were You

Equity research follow-up coverage, rating upgrade

For three quarters in a row now, Palantir has posted what I believe to be the best SaaS earnings the stock market has seen. For four quarters in a row now, Palantir has posted what I believe to be the best SaaS earnings the stock market has seen.

The intrinsic value growth that this business has been exhibiting over the past twelve months is nothing short of extraordinary. Not only because Palantir keeps accelerating its pace of growth and expanding its margins, but because of how durable the growth is. This is not short-term; this business will accelerate for a long time into the future.

For the observant investors, the interest in Palantir is skyrocketing, and it’s not only sourced from Palantir’s own commentary. CEO Alex Karp and other executives have been saying that the volume of inbound they are receiving is more than they can keep up with for several quarters now, and that was reiterated once again.

To double-check the interest, I ran a screen on the word “Palantir” across all publicly traded companies in the U.S., and the results surprised me. There are 647 separate instances of Palantir being mentioned across different companies’ investor relations. The customer testimonials are exactly what Palantir has been saying; they are changing the unit economics of businesses at scale, and as Palantir’s numbers also suggest, the customers can’t get enough of Palantir.

On Palantir, our partnership continues to deepen. I am convinced this relationship remains underappreciated by the market. Their Foundry operating system is empowering completely new ways of work.

From improving efficiencies in our manufacturing, logistics, planning, procurement to the automation of workflows throughout the company, we continue to believe that the upside to this body of work is well beyond anything approaching historical normality from traditional system upgrade efforts.

Scott Ford, Chief Executive Officer

Westrock Coffee Company, Q1 2026 Earnings Conference Call

The reason I highlight this particular customer is that the CEO was an AI skeptic. He does not follow hype on social media or delve into AI thoroughly. He thought that AI was a mere chatbot, with no tangible benefits to his business.

I realize that what I read and what we see talked about in the AI world and what Palantir’s operating system actually is, I can barely recognize the reality of what they’re doing on the ground with the talk that goes on around AI.

[…]you’re talking to a guy who’s not on social media, doesn’t know anything about it, doesn’t care to know anything about it. I was full grown when that came out. I skipped all of that. I thought AI and the chatbot and having conversations with an AI system was of the same ilk.

What I see, though, is the reality that Palantir creates a walled garden, if you will, where every piece of data in our network across all the systems and all of the handoffs and all of the spreadsheets and all of the memos and the hundreds of hours a week that we spend as individuals trying to explain and connect information from one system to another to another to then even be able to guess what our profitability is, let alone audit it.

Palantir’s Foundry system contains all of that information and drains the need for all of those systems and all of that activity. We’re talking tens of millions of dollars of benefit over the next three to five years annually in a business our size at only a $1.3 billion run rate.

Company profile

9 May, 2026 Follow-up coverage

Direction: Buy

Previous fair intrinsic value: $204.45, as of February 5, 2026

Symbol: PLTR, Exchange: NASDAQ

Sector: Technology, Industry: Software - Infrastructure

Theme: AI Software

Fair intrinsic value: $268.5 (94.85%), as of May 9, 2026

Market capitalization: $354 273 million

Pricing data: P/S 80x, P/E 220x

Previous coverage:

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

Note: Type-F sells an aggregated Excel sheet of Palantir’s historical financial data, containing ~1000 rows of both company-reported metrics, but also calculated KPIs, contract data, and more. The sheet also includes my valuation model, a charting tool (internal in Excel and on the web), and a dashboard overview of the business.

Available at: https://typefcapital.com, with free quarterly sheet updates.

Growth is exceeding everyone’s expectations

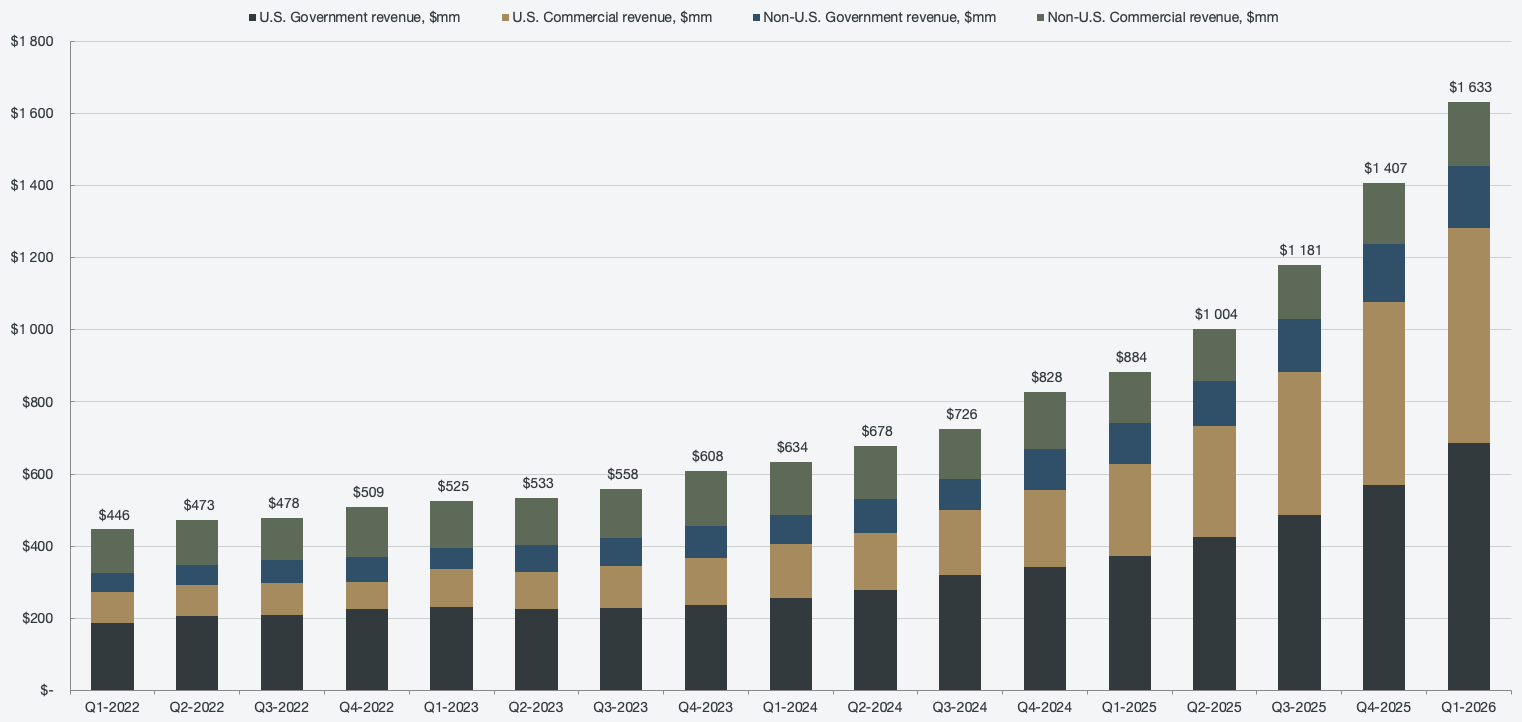

Palantir has once again exceeded Wall Street’s expectations, my own expectations, and their own guidance in terms of topline growth. Q1 2026 saw 85% Y/Y revenue growth, but as always with Palantir, the mere number is not the impressive part; it’s the composition of the number that tells the whole narrative.

Figure 1: Segmented revenue

When a company is exhibiting accelerating growth to an extent that it becomes exponential in nature, the natural question is to ask “how long can this be sustained?” That is why I find it important to understand the pillars supporting the growth that the company is experiencing, which also allows investors to understand the scalability of the business. Looking at where the growth came from on a cohort basis, 50% of the overall growth came from existing customers, and 35% came from new customers. That means, even if Palantir saw no new customers in the past year, they still would have grown 50% in Q1 2026 purely through their existing customer base from a year ago.

Figure 2: Existing customer and new customer cohort growth

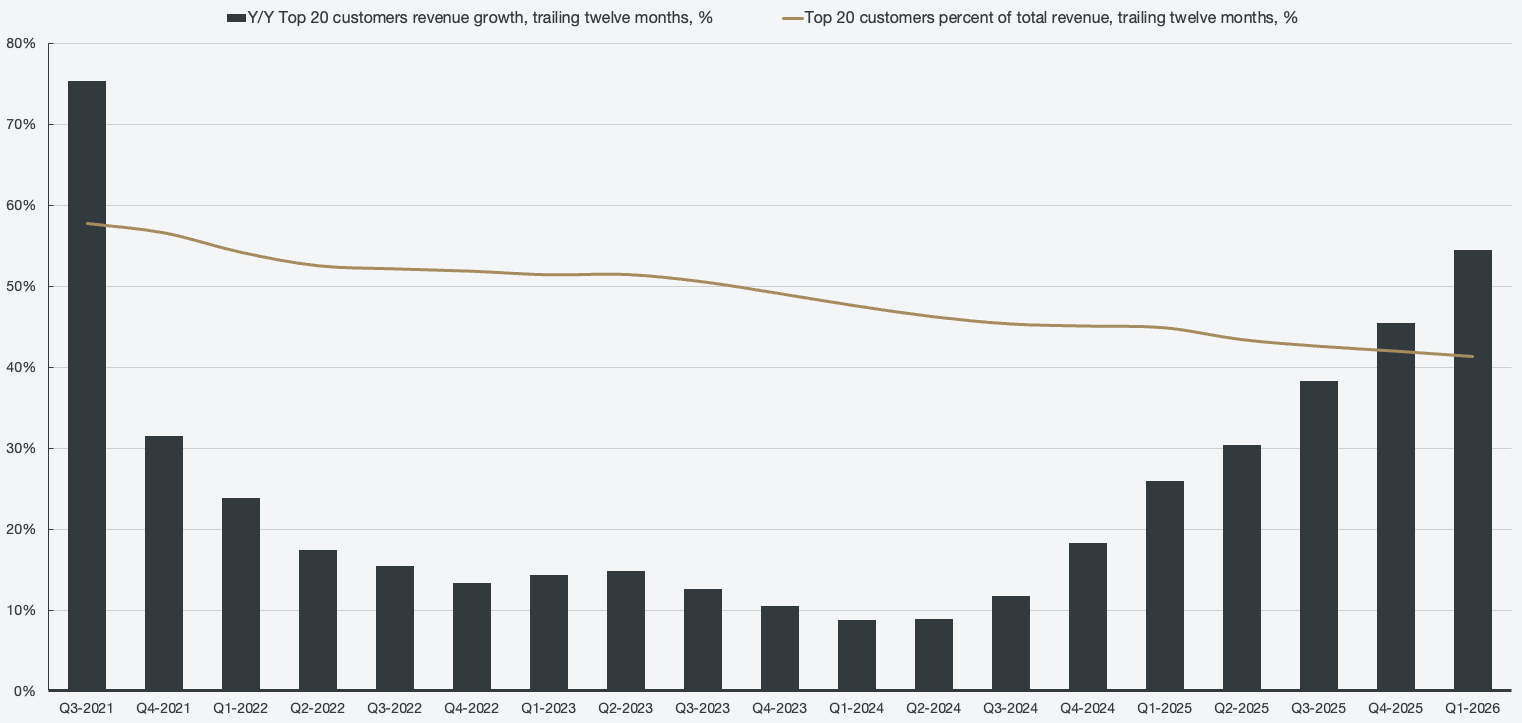

The accelerating trend in how much existing customers are spending on Palantir software is truly a marvel to behold, but it does not end there. Palnow now has over 1000 customers, and 2% of those (top 20) account for 41% of overall revenues. Over the trailing twelve months, the top 20 customers average $108 million in revenue per customer, while the average customer outside of the top 20 averages $3.1 million. The top 20 customers’ average spend is 3500% higher than the average of customers outside the top 20.

What’s astonishing is that these massive companies that are already spending huge amounts on Palantir software are actually growing their spending faster than the overall average of existing customers. The companies that already utilize Palantir on a large scale are still extracting so much value from Palantir that they find it necessary to increase their spending at an increasingly accelerating pace.

Figure 3: Top 20 customer cohort revenue growth (TTM), and percent of total revenue (TTM)

Those 3 charts are really all you need to tell the narrative of how Palantir is the only company in the enterprise software world that is actually delivering real, tangible value from its AI platform to its customers. The customers, who are already spending millions of dollars annually on Palantir software, are rapidly accelerating their pace of spending because they see how much value they are extracting from utilizing Palantir. In addition, the ones who are spending the most are the ones who want to also increase their spending the most.

While contract configuration seems to vary, we know from historical research that AIP has usage-based pricing. Meaning, implementing AIP to solve only a single use case may not yield a large increase in contract value, but those expanding AIP to power most of their business could yield a contract value increase of 2-3x, without a real ceiling. The more you employ Palantir, the more value you extract from it, and the more you want to keep implementing it. The reason Palantir can charge over $100 million annually for its software is that it generates more than $100 for the customers who are using it; meaning, if Palantir can save your business a hypothetical $100 billion in annual spending, you wouldn’t mind paying $50 billion per year for that software.

The scalable nature of the software is a core part of the sustainability of Palantir’s growth, but the more you dig, the more convincing it becomes. Existing customer cohorts and their accelerated growth are impressive, but there are many more financial results that point toward the sustainability and even acceleration of the growth that Palantir is seeing, for a long time into the future.

One of the more shocking comments from Palantir’s Q1 earnings call was Alex Karp mentioning that he will drive the company to double U.S. revenue in 2026 and also extend that to 2027. Two years of consecutive 100% growth in U.S. revenue, which is ~80% of total revenue, raises the intrinsic value of the business massively.

We are at our limit doing 100% this year, which I am going to drive the company to, and maybe we can do 100% next year in the U.S.

Alex Karp, Chief Executive Officer

Palantir Technologies, Q1 2026 Earnings Conference Call

The comment can be analyzed from multiple angles. First, Palantir has continuously implied that they do not have the capacity to handle all the inbound demand.

[…]we have 70 salespeople. A normal company of our size would have 7,000. Only seven of our salespeople actually even really sell. We are doing what a normal company would do with 7,000 salespeople, with seven people.

Alex Karp, Chief Executive Officer

Palantir Technologies, Q1 2026 Earnings Conference Call

So the question then becomes: why isn’t Palantir increasing its sales force to meet customer demand? The answer to why Palantir is intentionally not meeting demand, that I can think of, is quite attractive for Palantir.

There are two angles that I see this from. First, more demand than what can be met implies increased pricing power. Second, we know that AI FDEs (forward-deployed engineers) are being scaled out. AI FDEs solve several of the most expensive components of integrating Palantir across a business. AI FDEs can quickly and efficiently build out ontologies (the context of a business so that it can be effectively used by AI), which would otherwise require human resources and time, a pain point since Palantir has a limited number of FDEs.

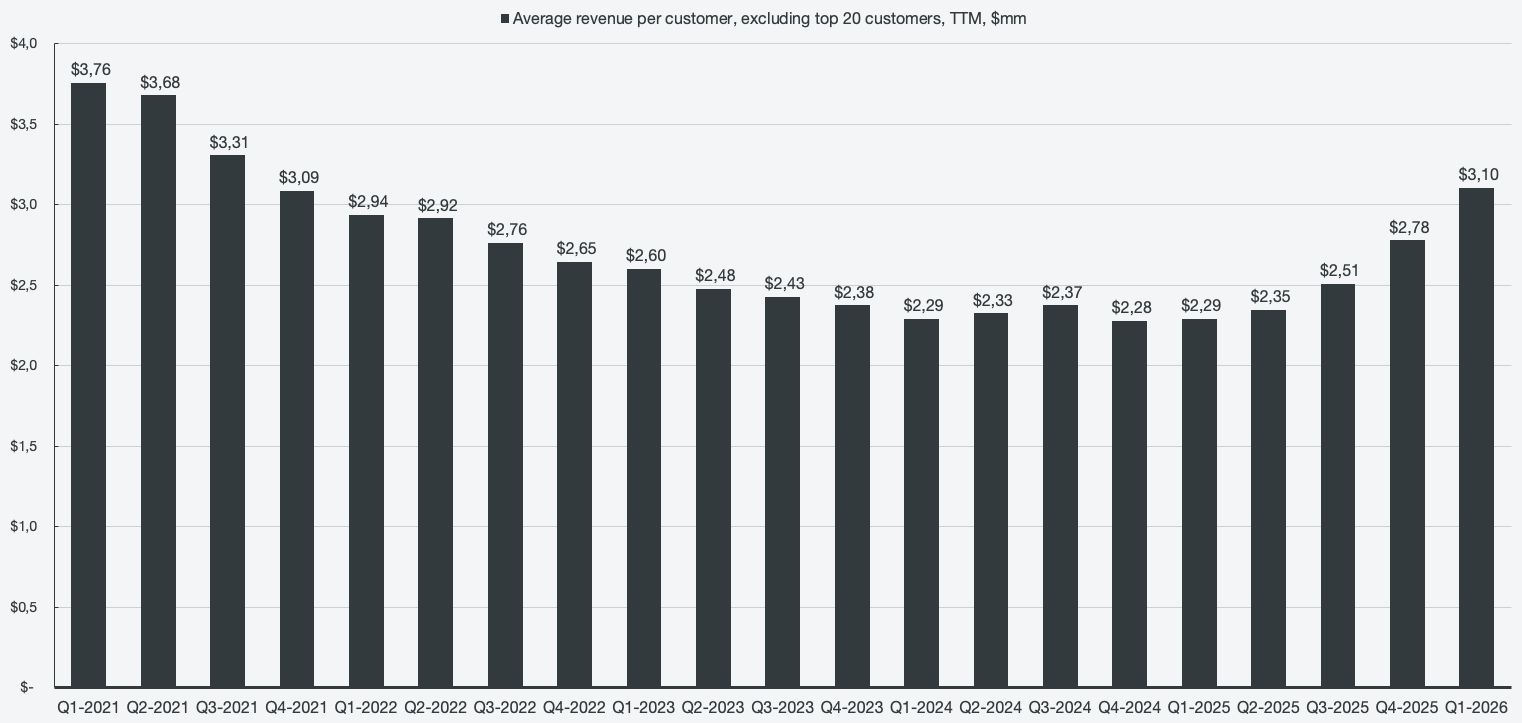

As for improved pricing power, it is starting to show up in average revenue per customer. As mentioned, the top 20 customers’ growth is outpacing that of the overall existing customers on average. The revenue per customer metric is really difficult to maintain, let alone increase, as a business starts to scale with an efficient go-to-market strategy (Palantir’s bootcamps). The metric was steadily declining until Palantir AIP launched, upon which it stabilized. Now that customer acquisition is slowing down due to Palantir’s inability to capture all the demand, the pricing power is being shown through the average revenue per customer (TTM), reaching 2021 levels in Q1 2026. I expect this metric to continue to accelerate over the coming quarters.

Note: the metric excludes the top 20 customers. Since 2% of customers account for 41% of all revenue, it would inflate the metric.

Figure 4: Average revenue per customer, TTM

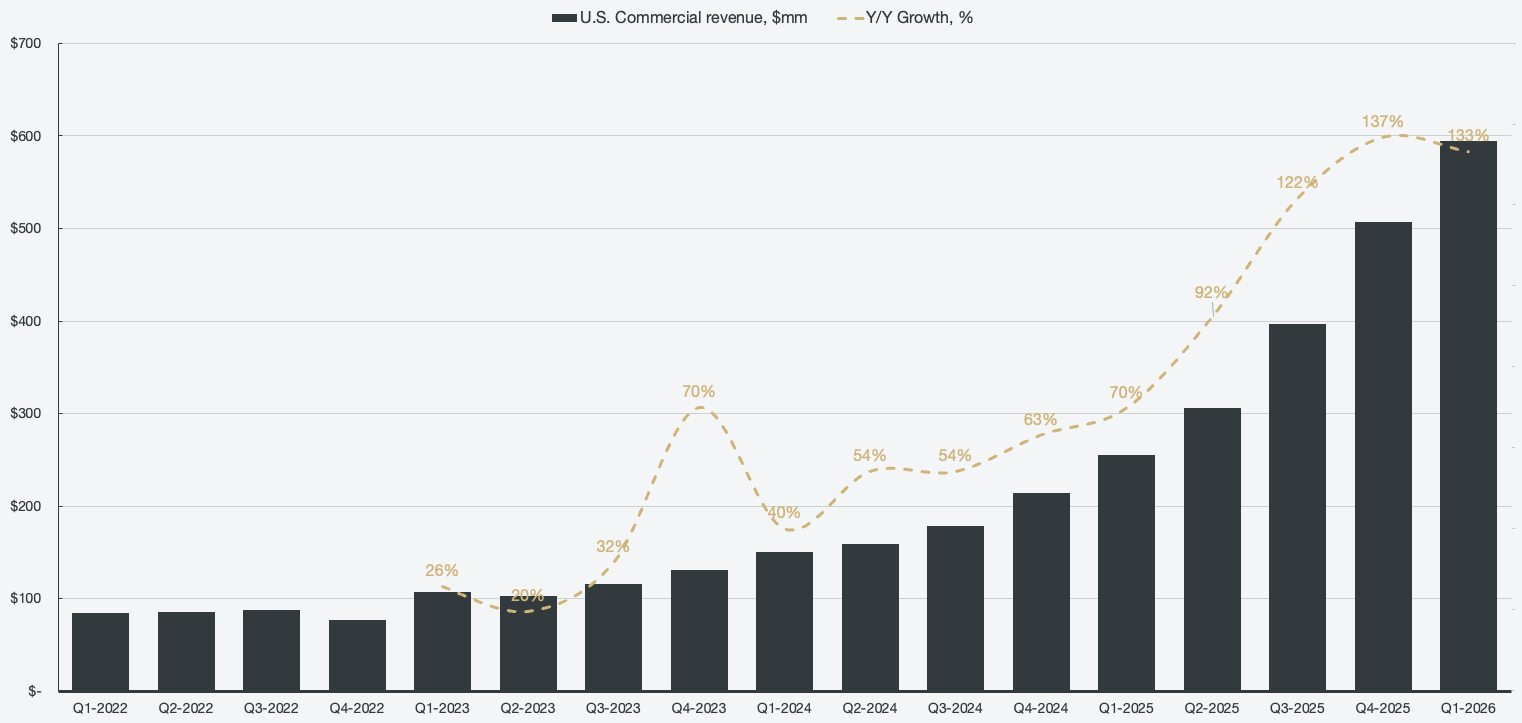

As an investor, it is difficult to complain about any perceived lack of growth due to not meeting demand when the business is accelerating the way it is. The stock sold off on a perceived U.S. commercial revenue estimate miss of $605 million versus a reported $595 million. The miss also resulted in a deceleration in Y/Y revenue growth for the segment since Q1 2024 (which is when AIP got momentum). However, that is simply due to Palantir reclassifying a major U.S. commercial customer as a U.S. government customer, and without the reclassifiation, Palantir would’ve grown U.S. commercial revenues to 143% Y/Y, to $620 million, handily beating estimates.

Figure 5: U.S. commercial revenue and revenue growth

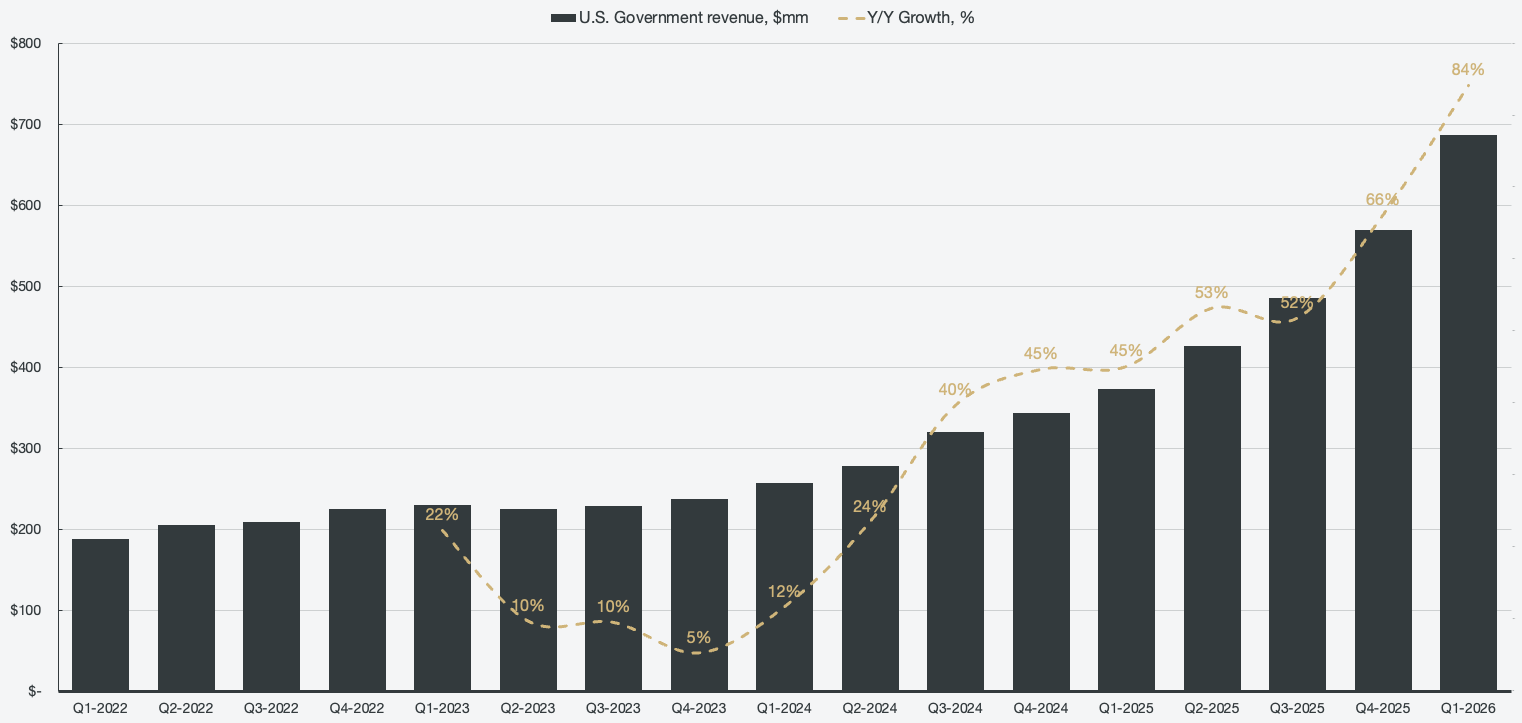

The U.S. government side of the business would have kept accelerating even without the reclassification during the quarter. With the addition, USG saw a large jump in growth from 66% in Q4 2025 to 84% in Q1 2026. USG is often undermined because the U.S. commercial segment is taking all the spotlight, but the USG business is also expanding rapidly. Much of the growth can be seen as a result of recent geopolitical events, and while that is true, Palantir is also widely expanding across multiple agencies simultaneously. Palantir software, much like on the commercial side, is delivering immense value to the agencies that adopt it, and Palantir is continuously receiving new contracts and expanding existing ones.

Figure 6: U.S. government revenue and revenue growth

As time passes, more and more international business is thriving as well. Until now, the exponential growth has only been observed within the U.S., but other regions of the Western world are starting to adopt Palantir at a wider scale as well. With global geopolitical tensions, NATO allies and other Western allies are likely to adopt Palantir solutions such as Maven Smart System NATO. There are several contracted awards regarding intelligence, data analytics, AI-enabled warfighting, and operational decision-making being awarded to Palantir across various nations. There are seldom any specific details as to what exact products are being adopted, but nations that are on the international government list include the UK’s MoD, Australia’s defense department, Canada’s DoND, France’s DGSI, Germany’s state-level police, Europol, and others, such as Ukraine and Israel.

Besides the warfighting context, there are examples of large and expanding international government contract awards, such as the NHS federated data platform (FDP). The NHS in the UK has seen a lot of media backlash, on the pretenses of Palantir mining UK citizen data, but the results are objectively massively beneficial to the UK taxpayers. Here are a couple of statistics:

Over 100,000 additional patients have undergone procedures.

800,000 patients safely removed from waiting lists through validation tools.

300,000 patients safely discharged (15.3% reduction in average discharge delays).

7% improvement in patients with suspected cancer referrals receiving a diagnosis.

28% reduction in waiting list size.

36% fewer patients stay over 21 days, improving patient flow.

The list is long, and there are many trust-specific improvements widely reported and tracked by NHS England.

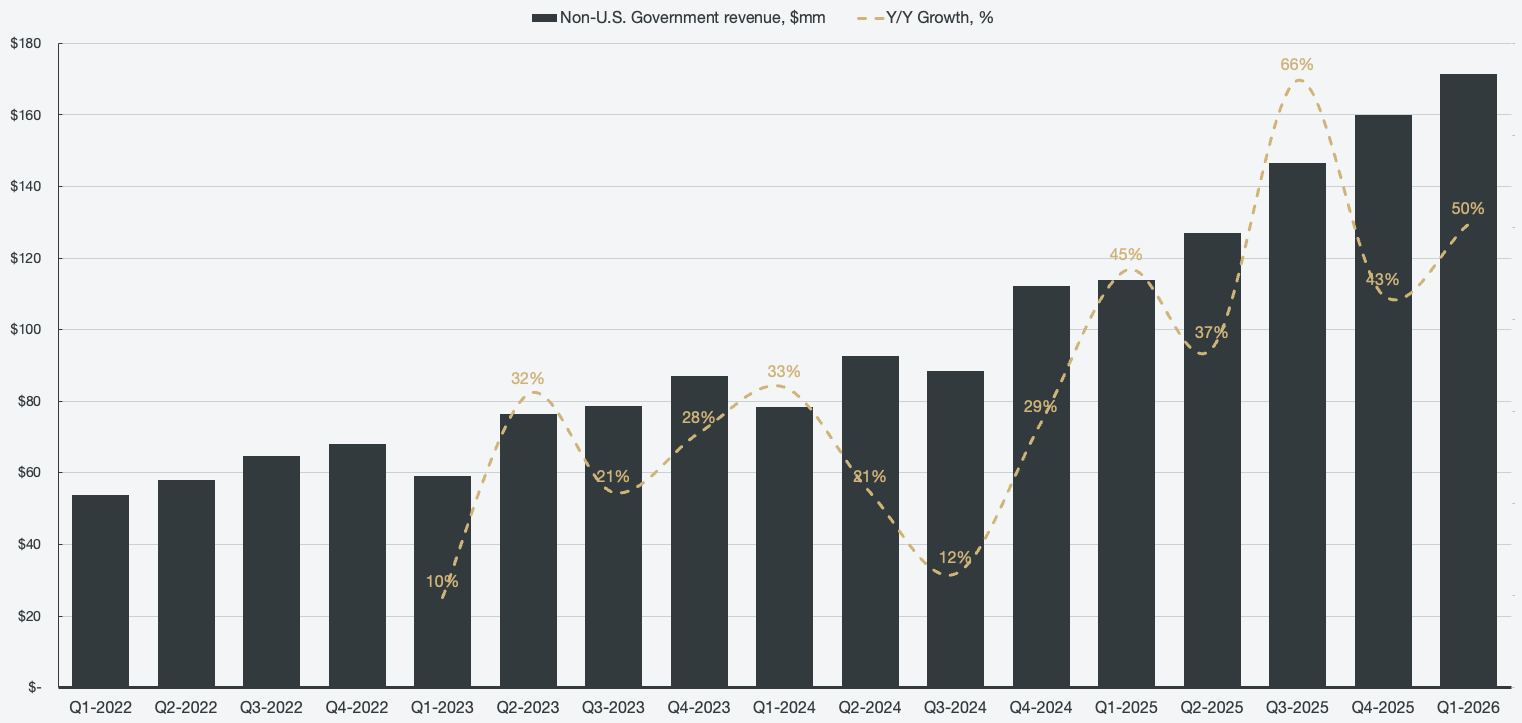

Figure 7: International government revenue and revenue growth

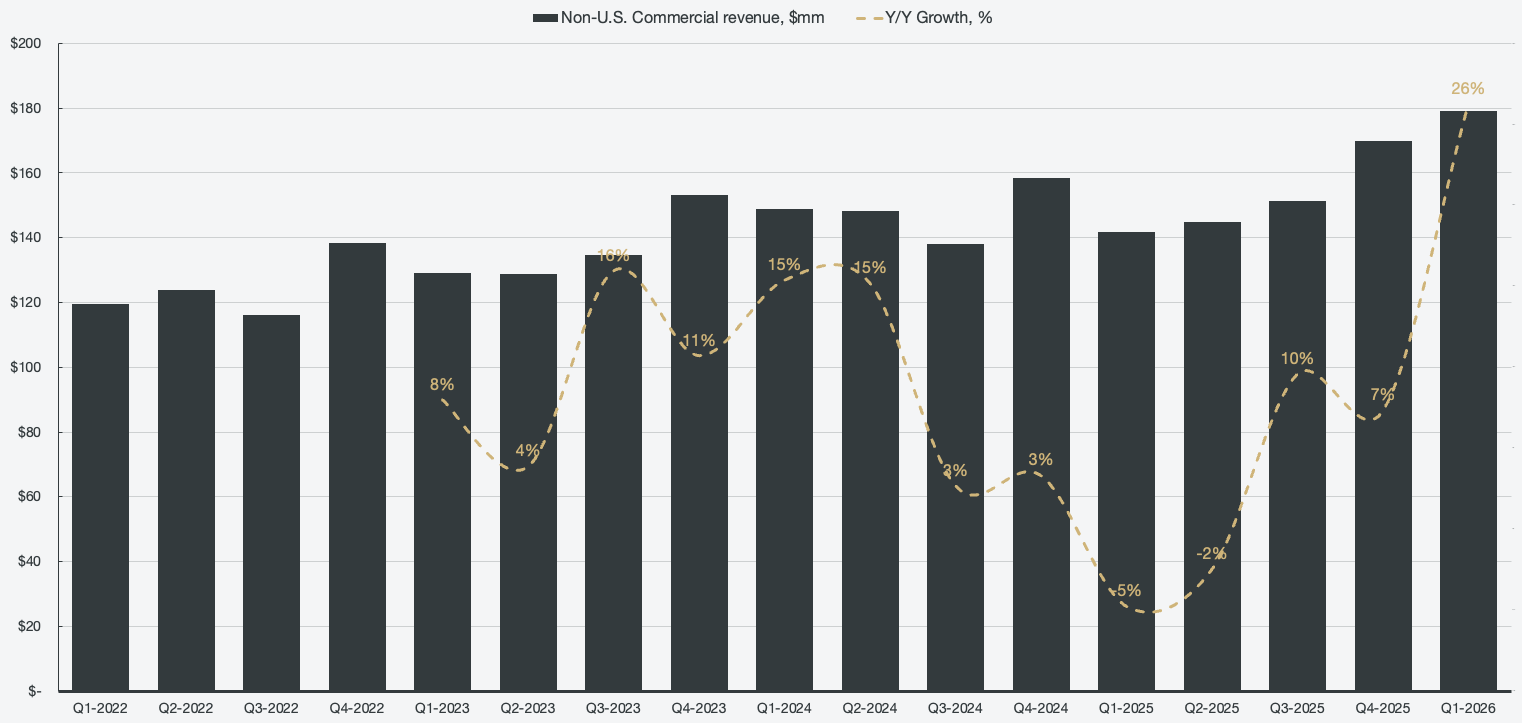

International commercial revenue has been more or less static since Palantir went public, with frequent commentary during earnings calls about Europe's unwillingness and inability to adopt AI solutions. However, other geographies have been more willing to use Palantir, primarily seeing large customers stemming from Japan and South Korea. The growth, despite Europe staying stagnant, is finally starting to accelerate, seeing 26% Y/Y growth, which is the fastest growth recorded for the segment in trackable history.

Figure 8: International commercial revenue and revenue growth

Efficiency and profitability have no ceiling

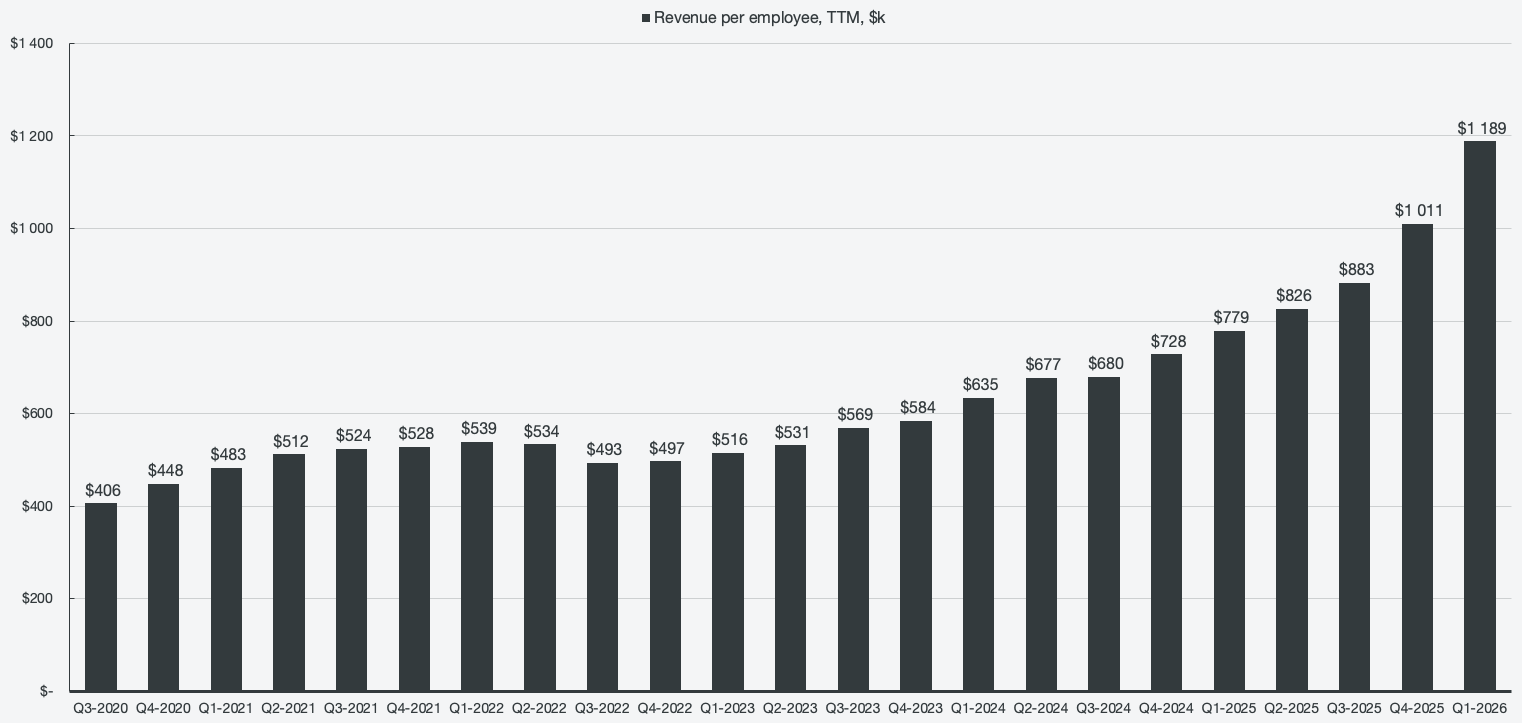

Palantir’s employee force is often touted as maybe the most brilliant group of engineers in the world. A simple approach to measuring employee efficiency across an industry is to look at revenue per employee. If Palantir’s engineers are world-class, they should generate more revenue per employee compared to peers, and Palantir does that handily. In fact, Palantir’s revenue per employee is more than double compared to some SaaS peers, including Palo Alto Networks, Salesforce, Autodesk, ServiceNow, Datadog, Fortinet, CrowdStrike, and Oracle.

Figure 9: Employee efficiency

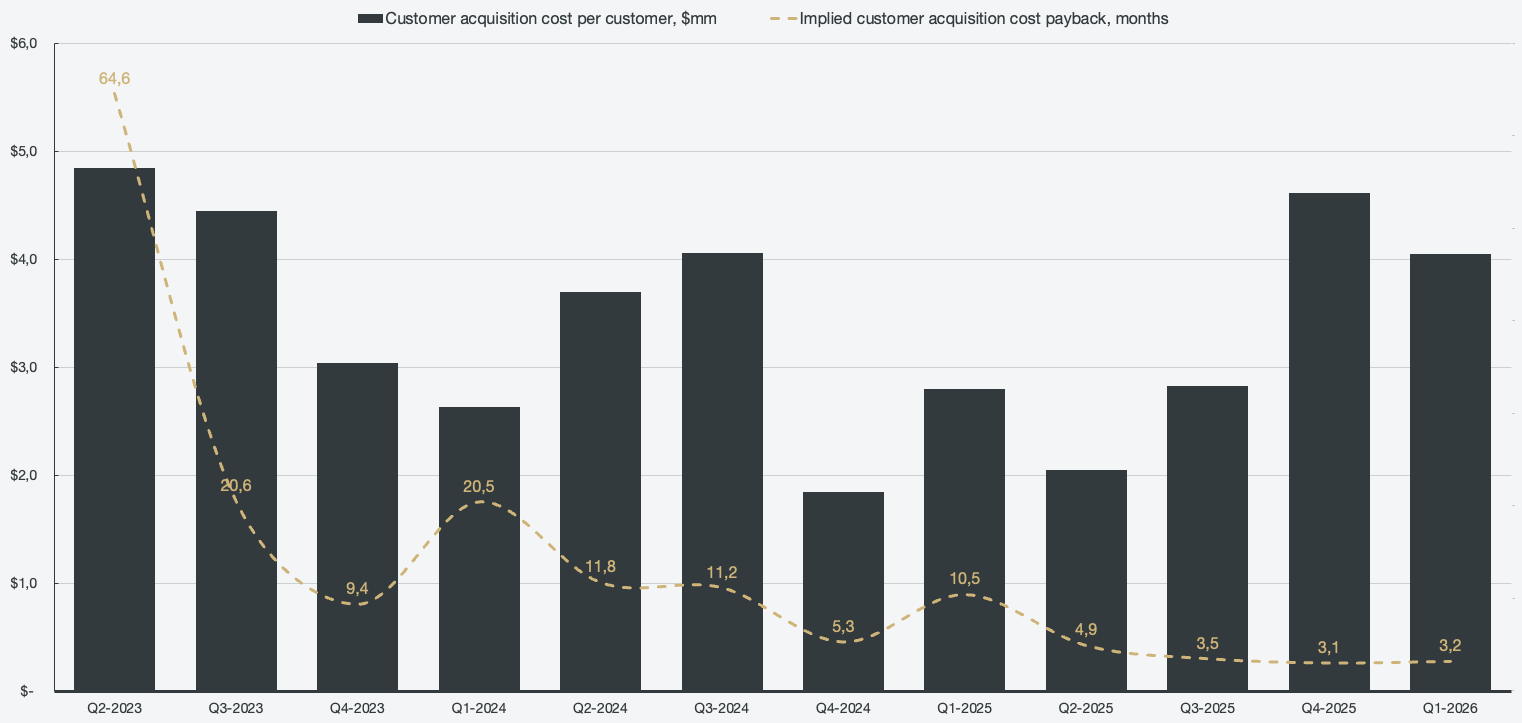

Efficiency extends across the whole business; no matter which stone is turned, there is a metric that is improving massively. Since the launch of AIP, Palantir went from having an implied customer acquisition cost payback time of 65 months down to 3 months in the past few quarters. This implies that any acquired customer has paid for themselves within one period, which is a very impressive dynamic.

Figure 10: Customer acquisition cost and CAC payback time

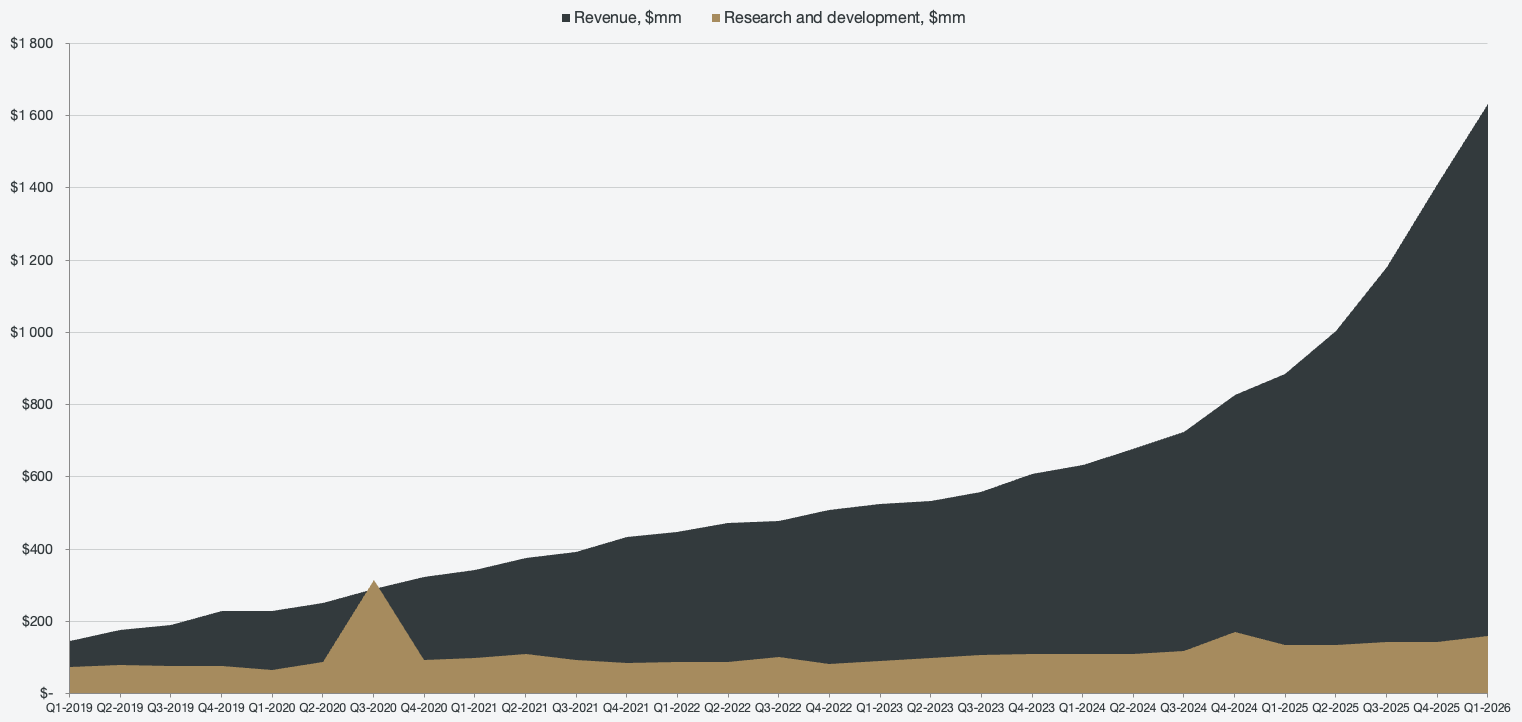

When you have efficient operations, it is only natural that margins expand as well. Palantir has immense operating leverage, managing to accelerate growth from 13% to 85%, all while also expanding margins. As Karp mentioned in an earlier quote, Palantir does not have a big sales force. In addition, while the engineers are world-class, R&D expenses are not really going up. Palantir has been shipping major platforms, services, and launching new products without meaningfully increasing R&D spending since the start of 2019. G&A and S&M are also incrementally inching upwards at a very slow pace, despite the business growing massively in scale in a relatively short period of time.

Figure 11: Operating leverage

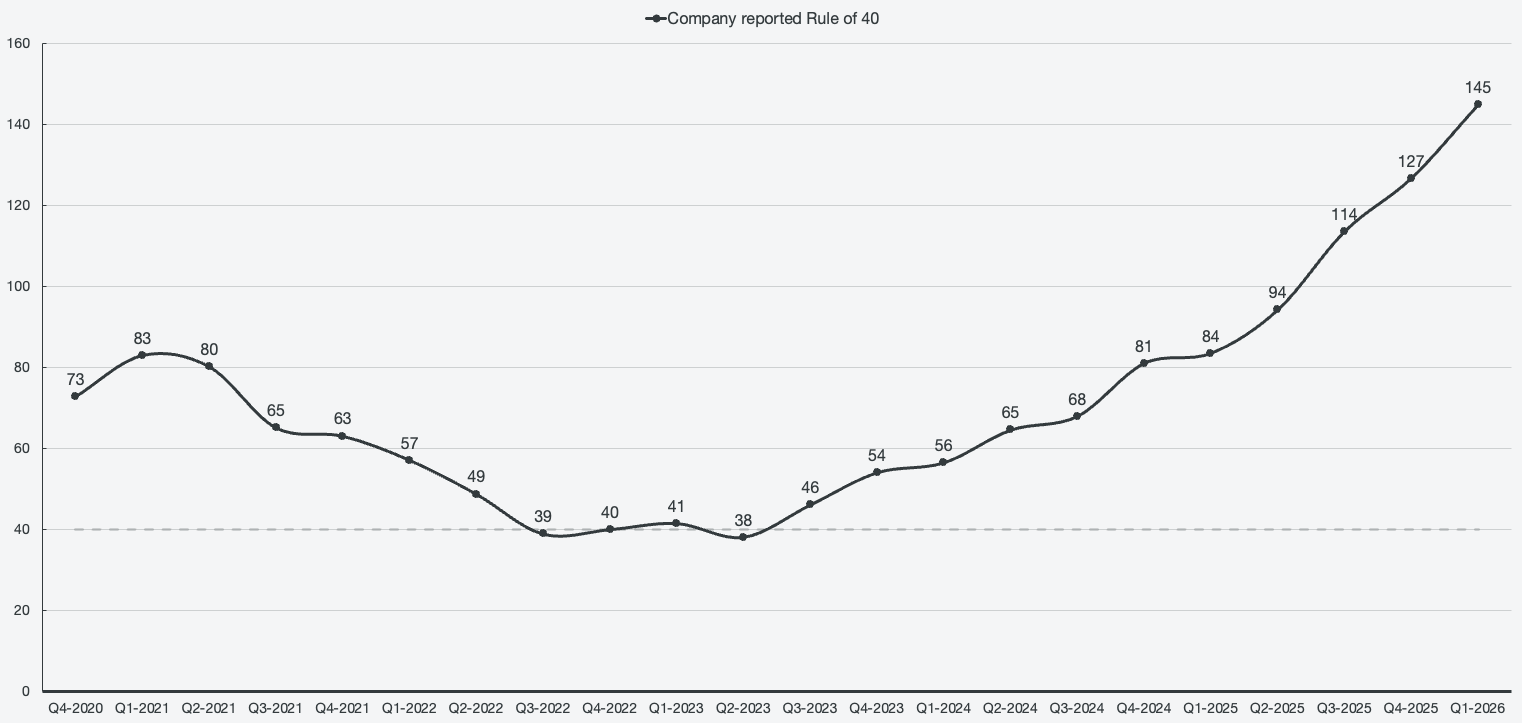

Palantir is unique in the whole stock market in being able to grow revenue and profitability simultaneously to an unprecedented extent. Some companies can have brief periods of matching Palantir in terms of measuring the quality of growth through the rule of 40, but no one is consistently improving the metric to levels seen by Palantir. For example, Palantir recorded a rule of 40 score (Y/Y revenue growth, adjusted operating margins) of 145 for the quarter, but is outpaced by Micron and SK Hynix (265 and 270, respectively), which are seeing explosive cyclical demand. Those companies don’t have the inherent robustness and consistency of Palantir, since they are cyclical in nature, while Palantir is operating towards a linear market with an essentially unlimited addressable market.

Figure 12: The rule of 40

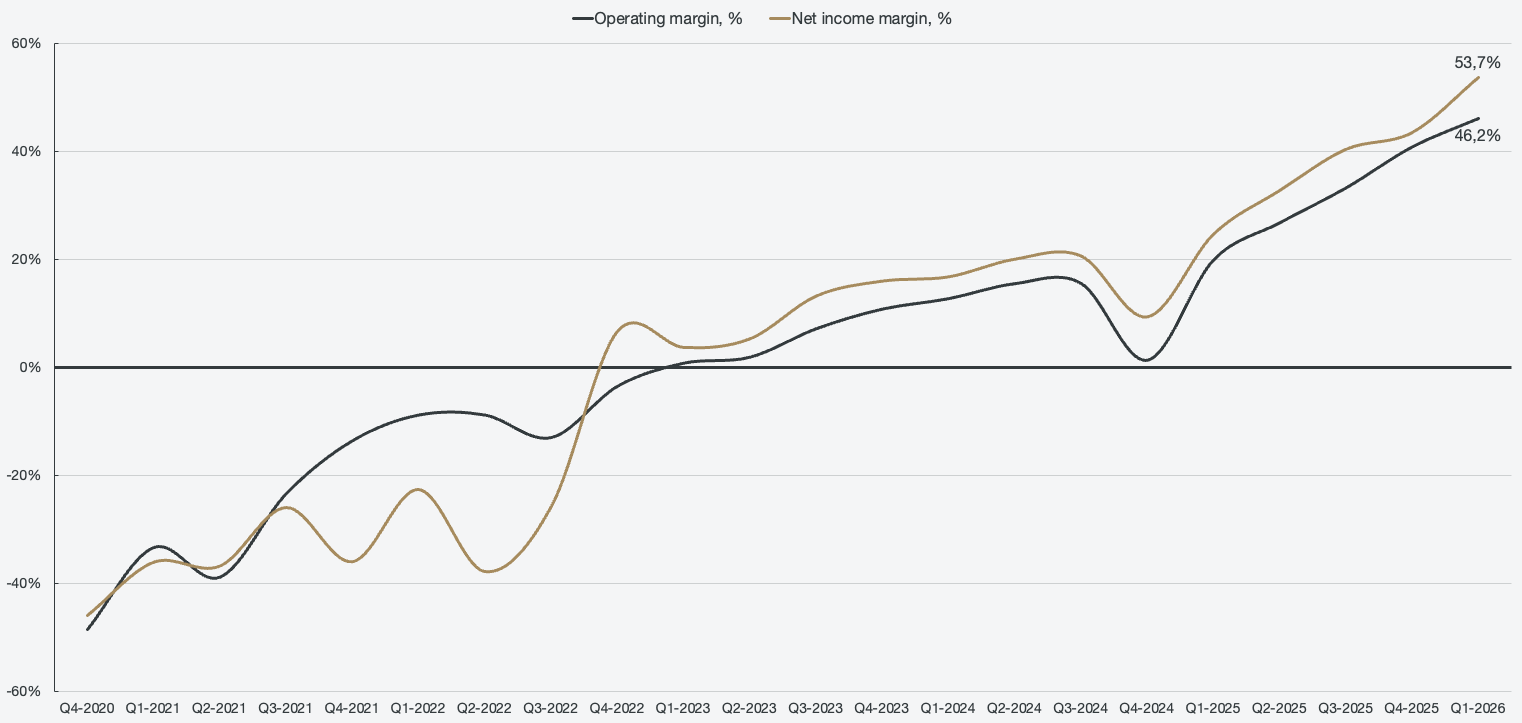

Looking at the resulting margin expansion, it has far outpaced any historical expectations from Wall Street and me. I don’t know where the ceiling for Palantir operating margins may lie, and my valuation model caps operating margins at 50%. I see Palantir achieving 50% operating margins by 2029, but they could report 50% as soon as the next quarter. That is the magic of Palantir; they keep surpassing everyone’s expectations each passing quarter.

Figure 13: Operating margins and net income margins

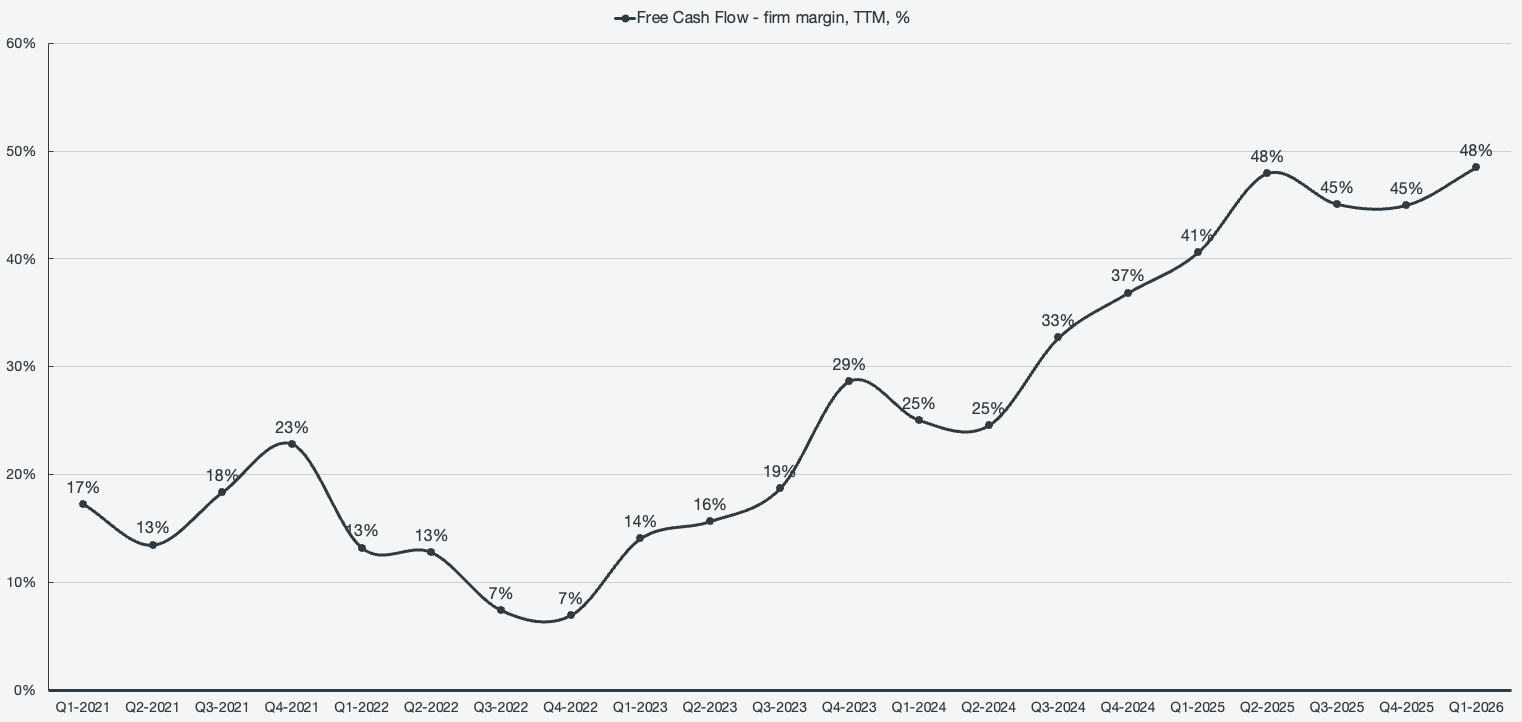

A majority of Palantir’s revenue is already being converted into cash, as the business is very capital-light. On a TTM basis, Palantir has already had a full year of over 50% FCF margins, and in terms of FCFF (which accounts for reinvestment needs), the figure is 48% in Q1 2026.

Alex Karp had an interesting quote during the earnings call, which I had not considered prior to him mentioning it. It really goes to show how quickly this business is moving.

Our free cash flow this quarter is larger than our revenue a year ago in the same quarter. Think about that. Same company, same people, extended products. It’s all being extended.

Alex Karp, Chief Executive Officer

Palantir Technologies, Q1 2026 Earnings Conference Call

Figure 14: Free cash flow - firm margins, TTM

We are all still early to the Palantir story

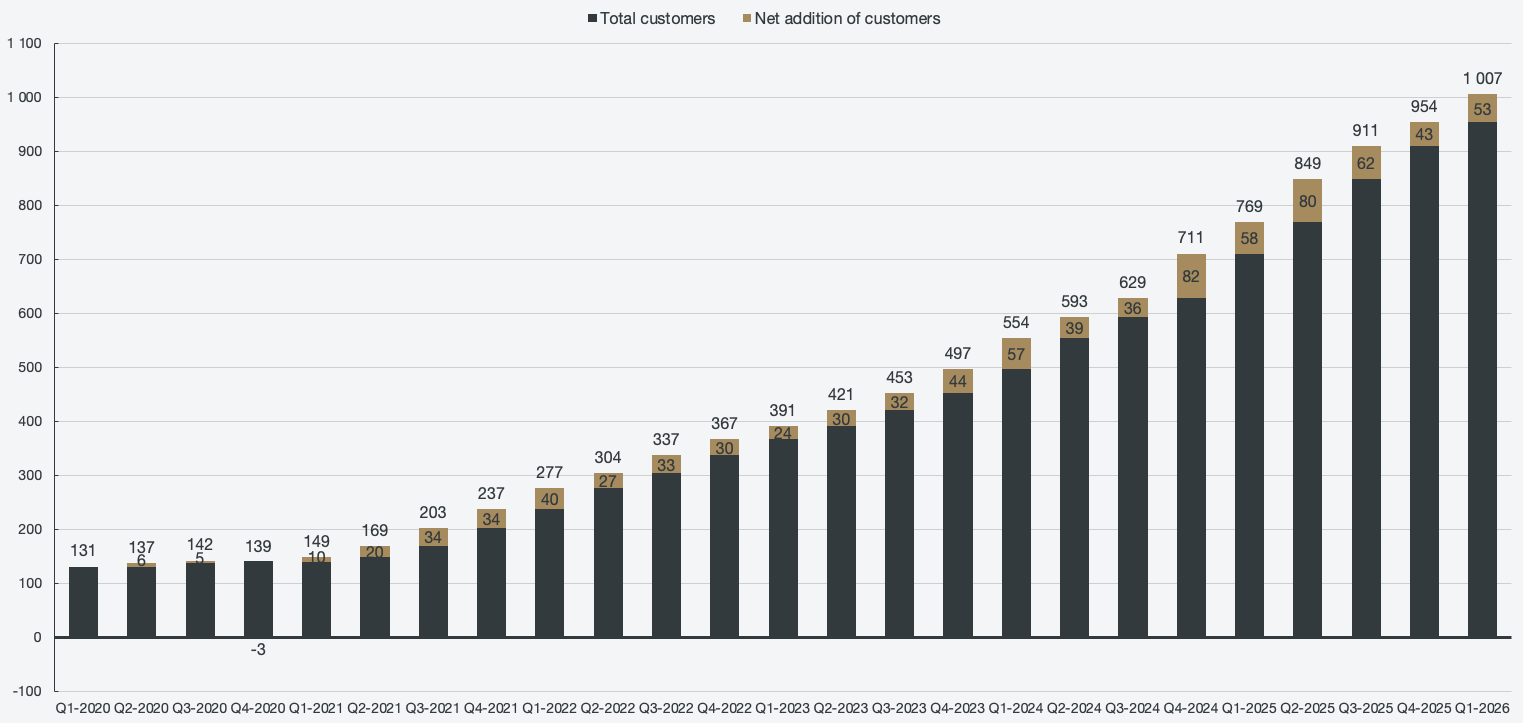

One of the most common comments I see whenever I discuss Palantir is that investors recognize Palantir as a great company now, but that they are too late to the story. The question being asked is “What’s the next Palantir?” instead of looking at Palantir itself and realizing that Palantir is the next Palantir. We are still very early to the narrative, and despite a sharp increase in the stock quote from the single-digit days a few years back, there’s still a lot of upside in Palantir. Palantir passed 1000 customers this past quarter, which is still marginal. As a reference, Salesforce is approaching 200,000 customers, while fast-growing peers CrowdStrike have more than 20 times the customer count of Palantir.

As we have seen, growth is not tied to growing the customer base quickly. The majority of Palantir’s growth is coming from scaling existing customers, and if the top 20 customers are any indicator, each commercial client has the potential to grow massively for Palantir. If Palantir stops growing customers and only focuses on scaling its current customer base to the same level as the top 20 customers, Palantir would have annualized revenue of ~$110 billion. But Palantir is growing its customer base, and there are a lot of customers, both on the commercial side and government side, for Palantir to keep growing for a long time to come.

Figure 15: Total customers

U.S. commercial saw an increase of 44 customers to 615, government saw 1 to 175, and international commercial increased by 8 to 217, after losing 3 customers in Q4 2025. The customer count in no way indicates anything near maturity. The customer growth can be argued to be relatively slow given how much demand there is, but that should change once AI FDEs roll out on a larger scale. That also gives support for the narrative that there is a long runway of hypergrowth still ahead for the company.

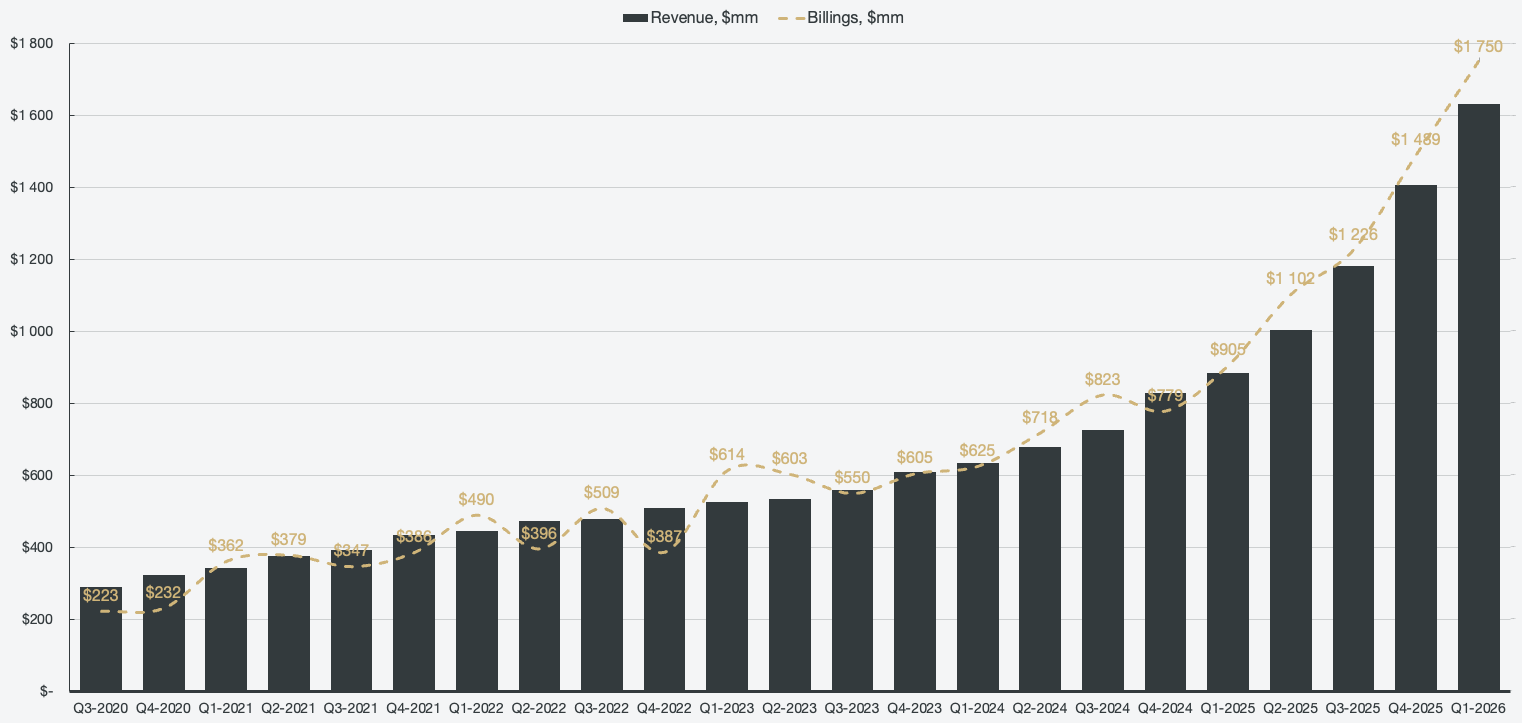

Another good indicator for future growth is billings, since GAAP rules prevent recognizing upfront payments for future services as revenue. Billings grew 93.3% Y/Y, and is accelerating for each passing quarter over the last twelve months. If billings are above revenues, it indicates that further revenue acceleration can be expected.

Figure 16: Billings

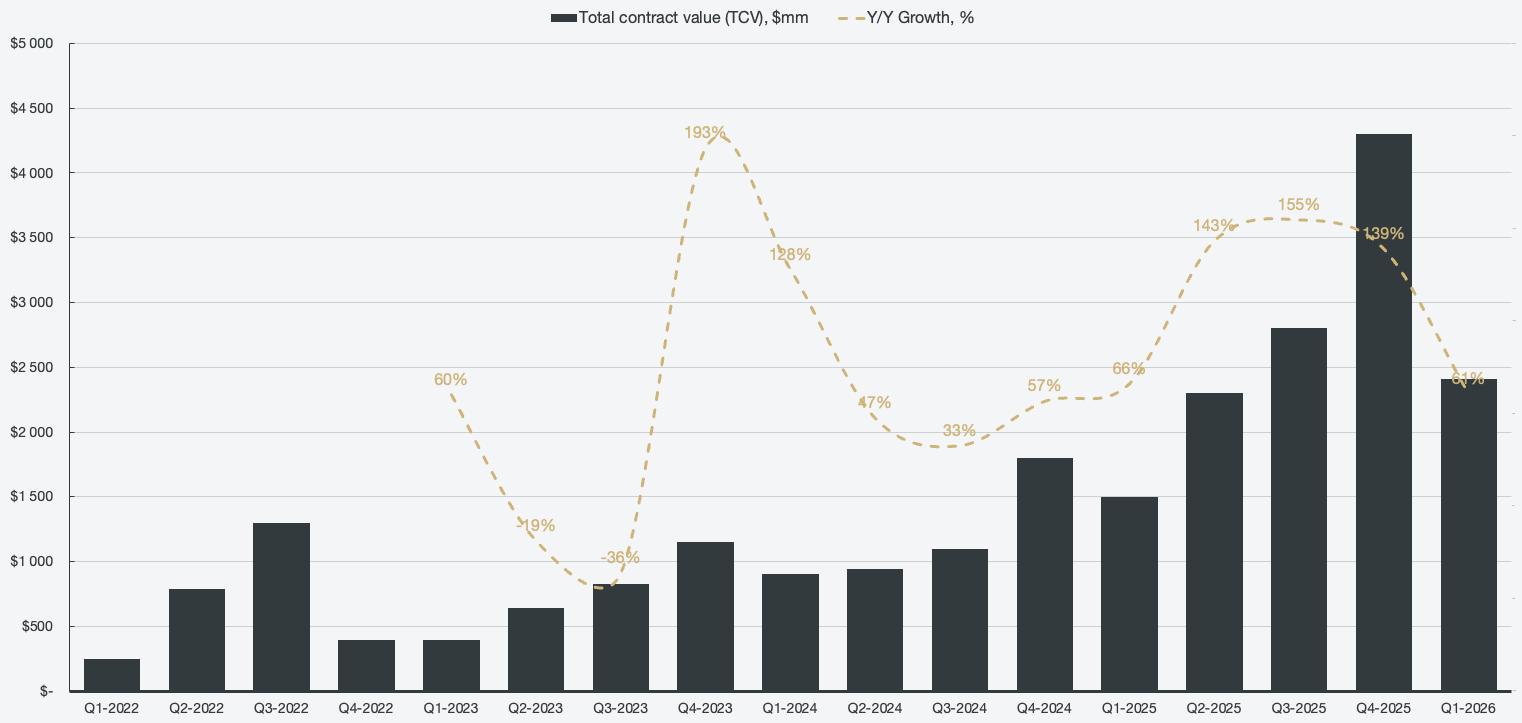

Q1 is seasonally the slowest quarter in terms of new contract value, and we see a sharp drop-off compared to Q4 2025. TCV is still up 61% Y/Y, and should accelerate into Q2 and the rest of the fiscal year. Not observing the seasonality may have left some investors worried about the metric.

Figure 17: Total contract value

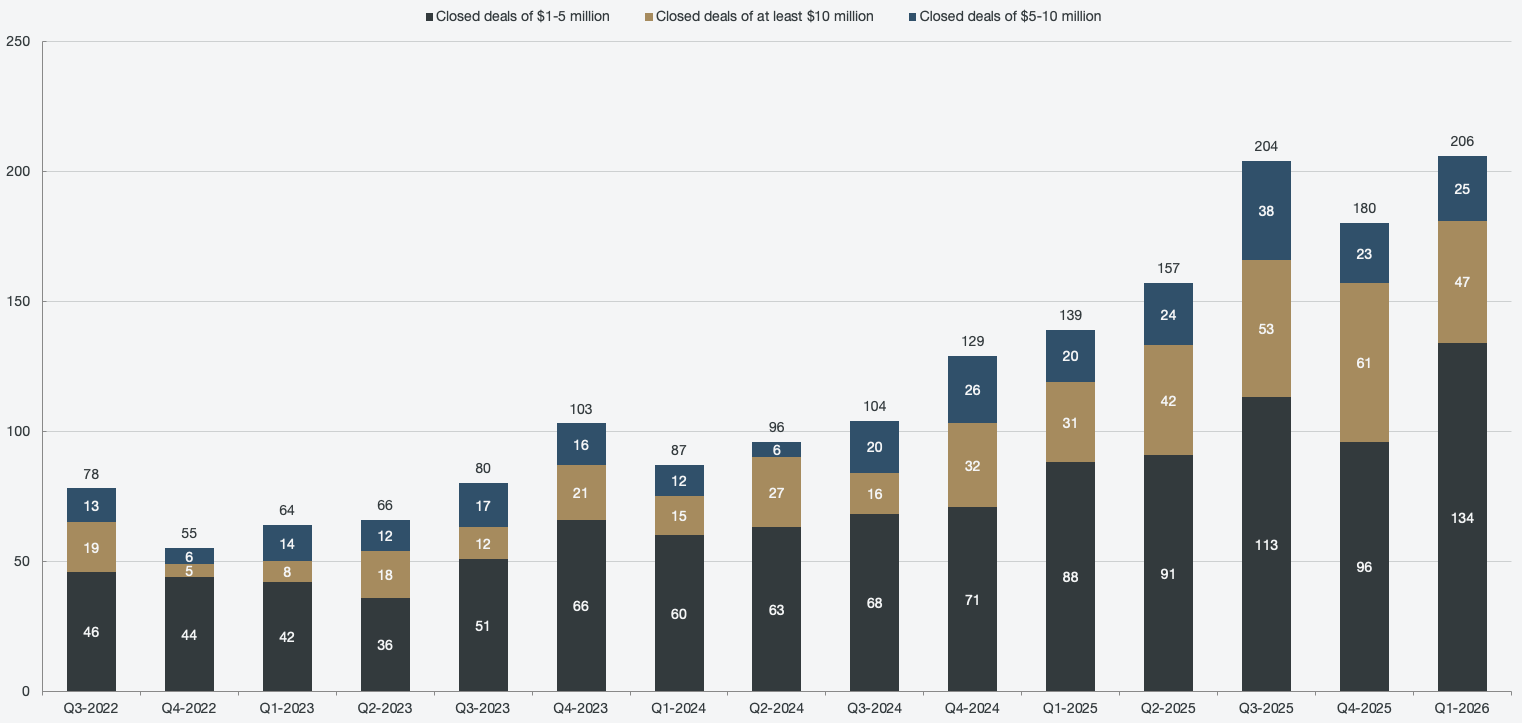

TCV is made up of the deals signed during the quarter, and looking at all deals signed of at least $1 million, Palantir reached a new all-time high in Q1 2026 despite TCV looking weak. The composition is strong on deals closed between $1-5 million, but weaker on larger deals. A similar dynamic can be observed in Q1 of 2025, and is not alarming, knowing the seasonal nature of contracts.

Figure 18: Deals closed of at least $1 million

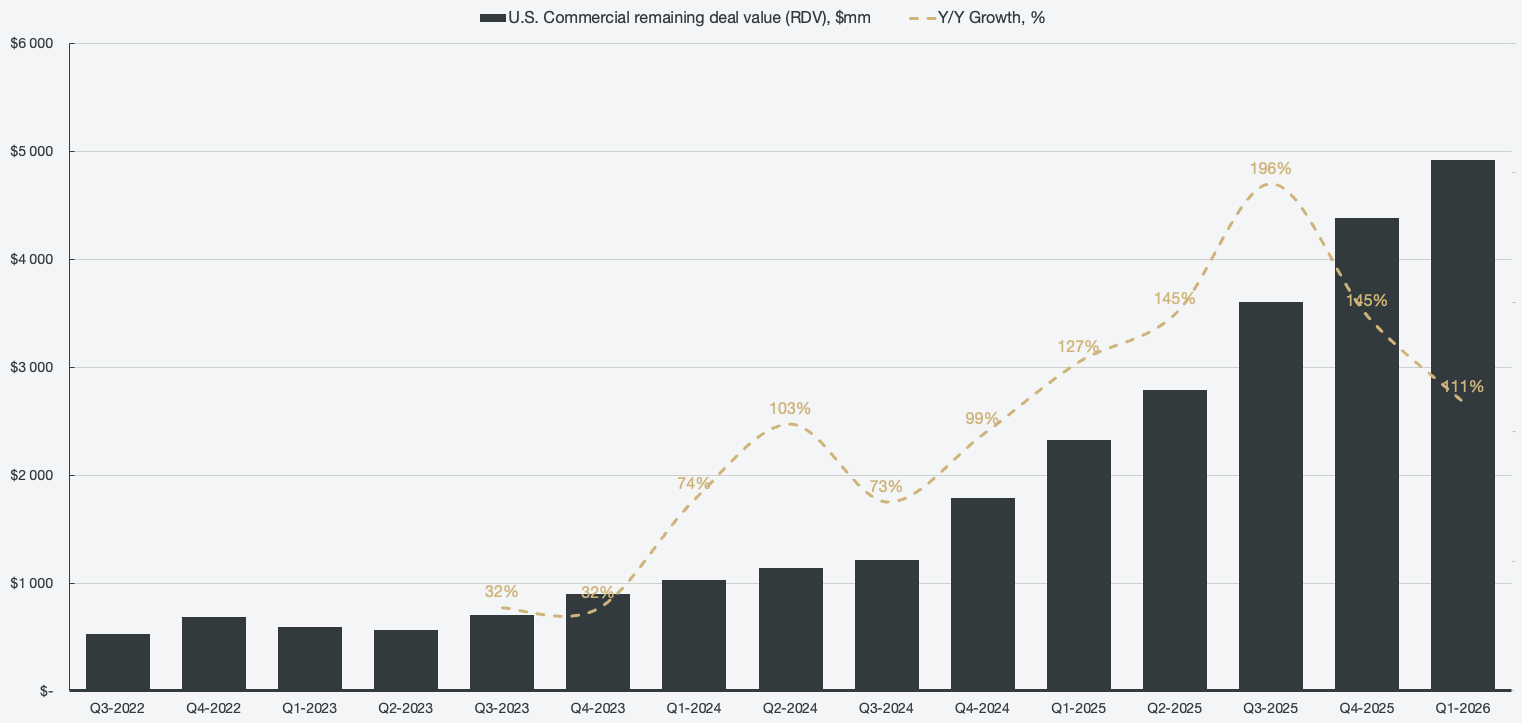

Remaining deal value reached $11.8 billion, which means that there is a lot of revenue left to recognize across both commercial and government. While up 98%, the increase looks small relative to the Q3-Q4 2025 jump. Even if Palantir were to cease acquiring new customers and expanding existing customers, it would still recognize ~$12 billion in revenue from existing contracts and options. To note regarding RDV is that not all the revenue is guaranteed, as it also includes contractual options that may not be recognized.

U.S. commercial RDV is 42% of total RDV at $4.92 billion, and grew 111% Y/Y.

Figure 19: U.S. commercial remaining deal value

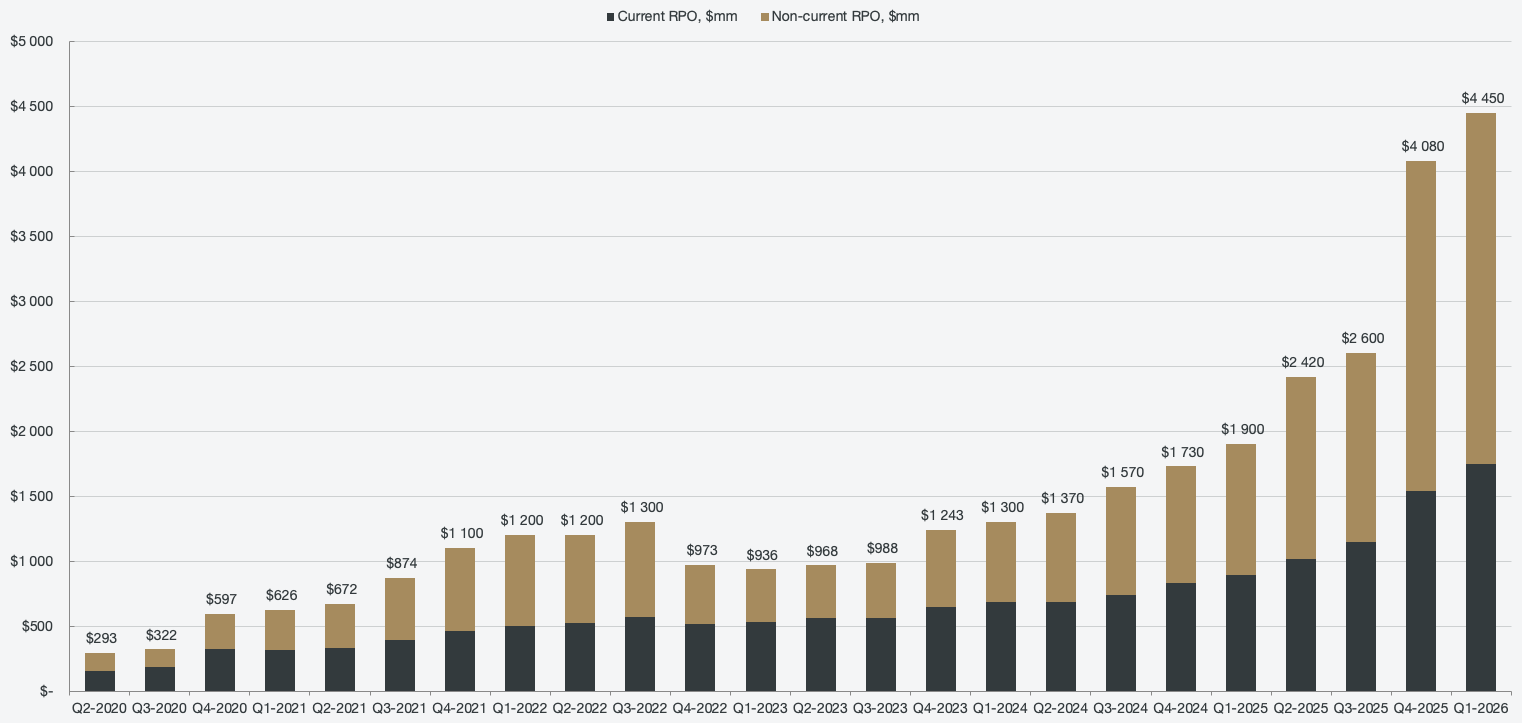

Looking at the remaining performance obligations, which, unlike RDV, are guaranteed revenue, it grew 134% Y/Y to $4.45 billion. RPO is primarily composed of the commercial segment, since government contracts tend to be uncertain in nature, relating to timing and recognition. Of the RPO, 39% (~$1.75 billion) will be recognized over the next twelve months, which is higher than the total revenue recorded in Q1 2026. Keep in mind that a major customer was reclassified from commercial to government during the quarter, which may have impacted total RPO.

Figure 20: Segmented remaining performance obligations

Contract balances and the aggressively scaling existing customers all point towards a continued acceleration of growth across the business. The trends also point towards an extensive period of hypergrowth, meaning it is not about to end anytime soon. This further strengthens the argument that Palantir is still early. Palantir has relatively few customers, is seeing more demand than it can handle, and contract balances show that there is a lot of growth still to recognize, even among the existing contracts.

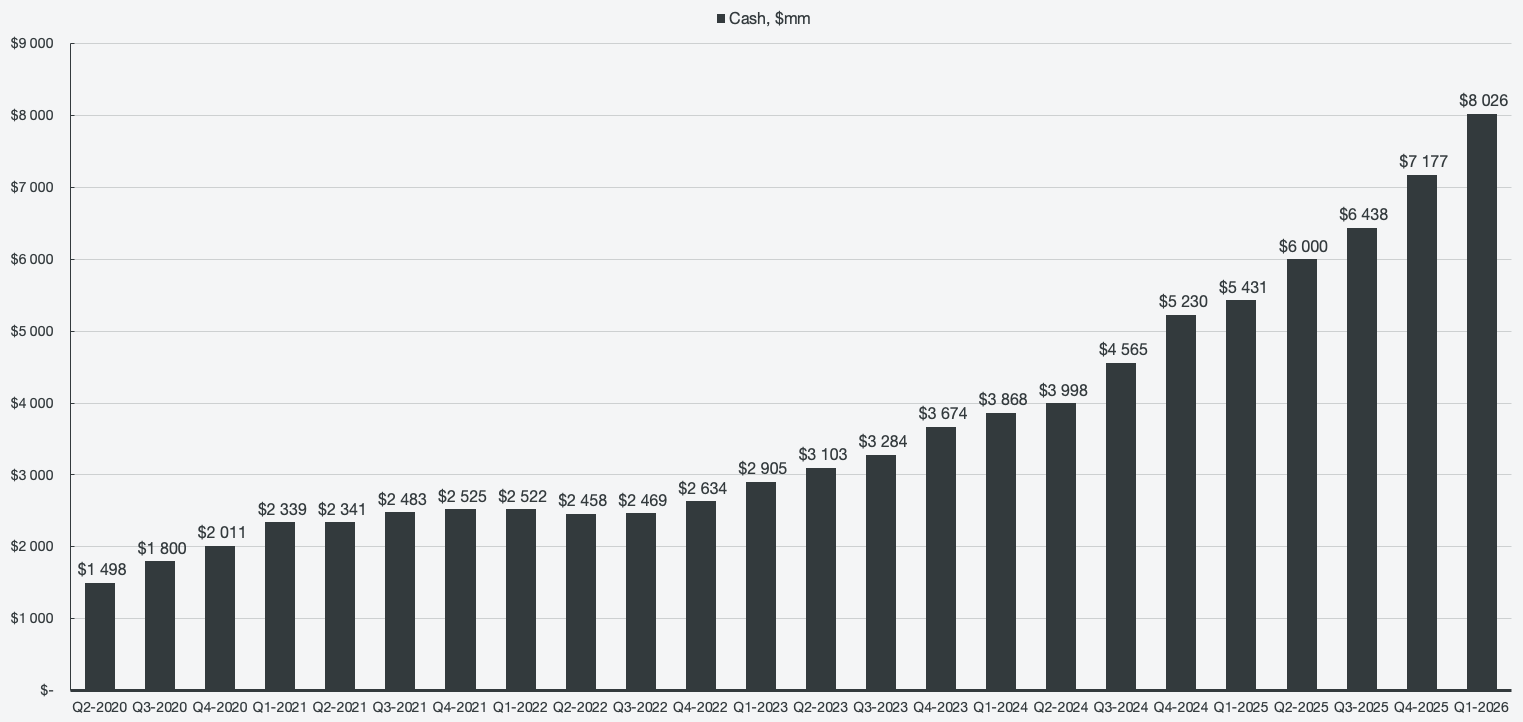

Another forgotten dynamic is that Palantir has no debt. They are not expending excessive amounts of cash to achieve the current hypergrowth cycle, nor do they need to put capital to work in order to develop new products. The business is highly efficient across each vertical, and the cash keeps accumulating. The question is, what happens when that cash gets put to work, what may growth look like then? I personally don’t see a need for Palantir to burn cash, as they have already proven that they can be at the forefront of the most exciting revolution in the history of the financial world. Instead, I would like to see them invest across high-quality, aligned businesses. Former employees of Palantir have left to found their own businesses, some of which are doing extremely well. Also, there are obvious synergies across other companies with aligned values, such as Anduril, which Palantir could acquire a stake in. For now, treasury yields are still attractive, and I don’t mind parking cash inside of treasuries until yields drop. However, that won’t last forever, and it will be interesting to see how Palantir utilizes the cash pile in the future.

Figure 21: Net cash

Diminishing returns risks

Business risk has been absent from the company for quite a while; all investors had to worry about was not overpaying for Palantir stock. That sentiment has now turned into a risk of not owning enough Palantir before it is too late, as they keep increasing intrinsic value tremendously for each passing quarter. The risk is related to not having enough foresight into the aggressive expansion of revenue and margins that we are seeing.

Similar to past quarters, political risk remains material, and Palantir is seeing a lot of pushback driven by a false media narrative against the company. The outcry against Palantir is politically driven and does not seem to be impacting the business on a corporate level at all, as evidenced by the demand for the product.

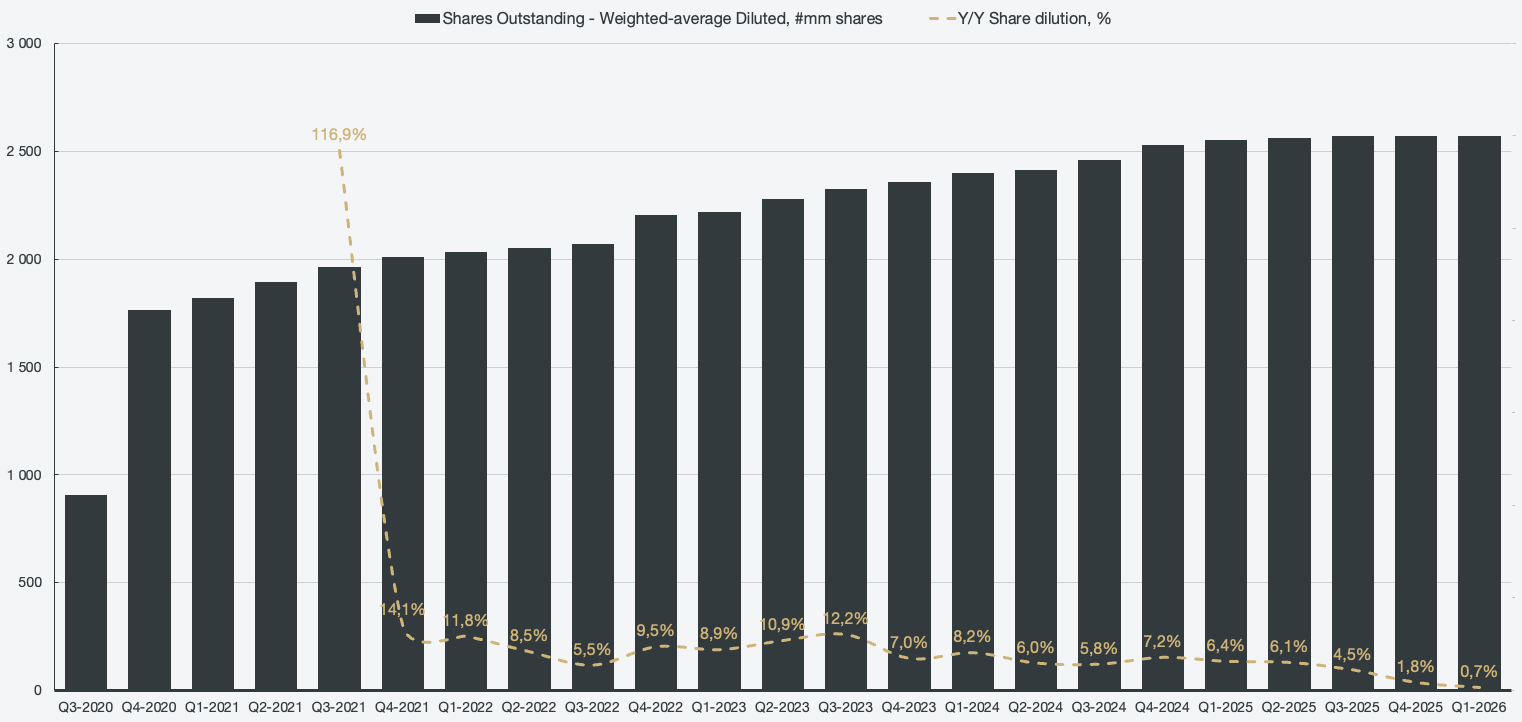

The bear arguments are dwindling for each passing quarter as well. Most of the historical bear arguments have already been dismantled, such as the one relating to Palantir purchasing revenue (SPACs), Palantir only being profitable due to interest from treasuries, and now also the argument that Palantir diluted shareholders into oblivion. Historically, an argument could be made that Palantir was paying excessive amounts of stock-based compensation and, in turn, diluting shareholders. However, SBC as a percentage of revenue is about half of what the SaaS average is, and continues to drop. Furthermore, the current dilution of existing shareholders was only 0.7% Y/Y (1.8% in Q4 2025), which is considerably low when looking at the stage of maturity Palantir is in.

Figure 22: Weighted-average diluted shares outstanding and share dilution

Intrinsic valuation and fair value

The market is currently experiencing a sector-wide sell-off due to fears of AI labs disrupting software companies, and Palantir is among those punished. Despite the jaw-dropping financial results, the stock traded down post-earnings. We saw P/E ratios in the 400-500 range, and P/S ratios over 100. However, I am not so sure that most people in the markets could call Palantir expensive now. Price-to-sales is at 68 times, which in isolation seems expensive, but then you look at the growth that Palantir is exhibiting. Is 68 P/S expensive in the context of Palantir growing 85% Y/Y and ~100% for the year, and another 100% next year? I would even argue that the P/S ratio is looking cheap for this kind of business, especially considering the sustainable nature of the growth we are seeing.

It does not matter to me personally, as I do not put weight into short-term pricing when evaluating businesses; I strictly focus on intrinsic value in my research and investing. From an intrinsic value perspective, it is almost scary how undervalued Palantir became over a single quarter. Then again, I have been saying that for each passing quarter. The intrinsic value growth, as we learn more and more about the business for each passing quarter, has been remarkable.

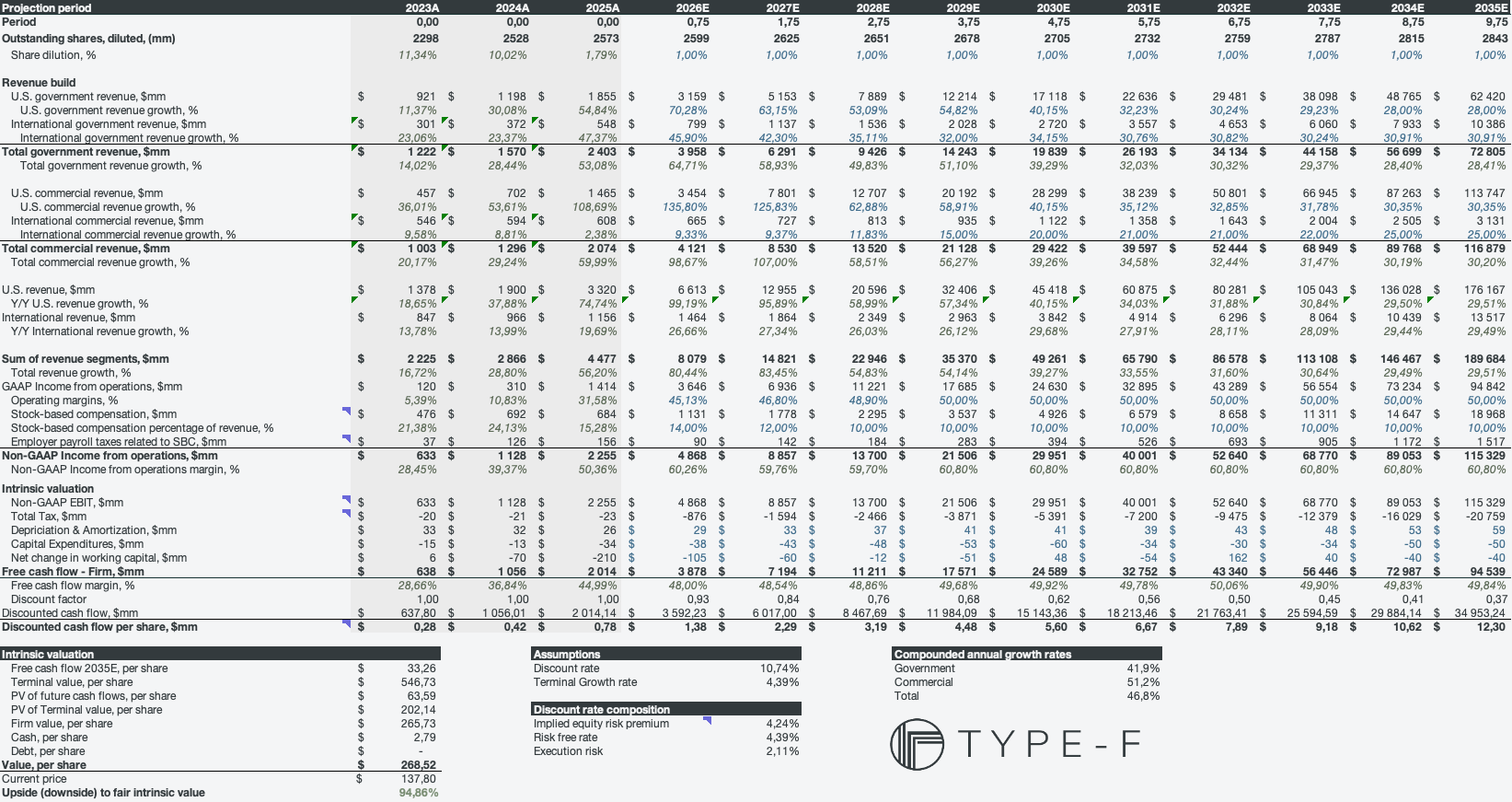

The model sees a revision down on dilution per period, as Palantir is now below 1% Y/Y dilution. That change has boosted the intrinsic value to increase substantially. In addition, I have revised U.S. revenues to align with the expected 100% into 100% growth as per Alex Karp’s commentary. I am also relatively conservative with operating margins, still expecting 45% for FY 2026, and not reaching 50% until 2029. With these changes, Palantir has ~95% upside, with a fair value per share of $269. It looks crazy at first glance, given where Palantir traded a mere year or two ago, but the narrative is clear and easy to defend.

Table 1: Intrinsic valuation model

A capital-light business that is growing massively while simultaneously expanding margins aggressively is the recipe for perhaps the most dominant business in software.

Type-F Capital, Palantir Technologies: Absolute Dominance, February 5, 2026