S&P Global: A Robust Fortress Built To Weather Every Scenario

It is quite rare to encounter a business that has an operational segment with ~60% operating margins, high predictability, and sustainable double-digit growth. S&P Global operates more than one such segment. It’s a capital-light, diversified business of high-quality, high-barrier-to-entry segments with high margins.

Company profile

Theme: Quality, Direction: Buy

Symbol: SPGI, Exchange: NYSE

Sector: Financials, Industry: Financial data

Fair intrinsic value: $567.10 (+11%), as of May 29, 2025

Market capitalization: $159 530 million

Pricing data: P/S 11x, P/E 41x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

The crown jewel of S&P Global’s business segments is the credit rating business. It has been around for more than a century and involves assessing the credit risk of corporations, governments, and various debt instruments. What makes the ratings business so robust is that credit is needed in all economies to survive harsh times as well as accelerate growth during good times. However, there is cyclicality to the business, in particular in relation to rates.

2022 saw a harsh pandemic-related spike in the 10-year U.S. Treasury yield, going from ~1% at the beginning of the year to a peak of above 4%. Due to this, refinancing of debt and new credit issuances were substantially less attractive. However, issued debt has a maturity date, and by tracking the maturity schedule, the ratings business becomes a lot more predictable.

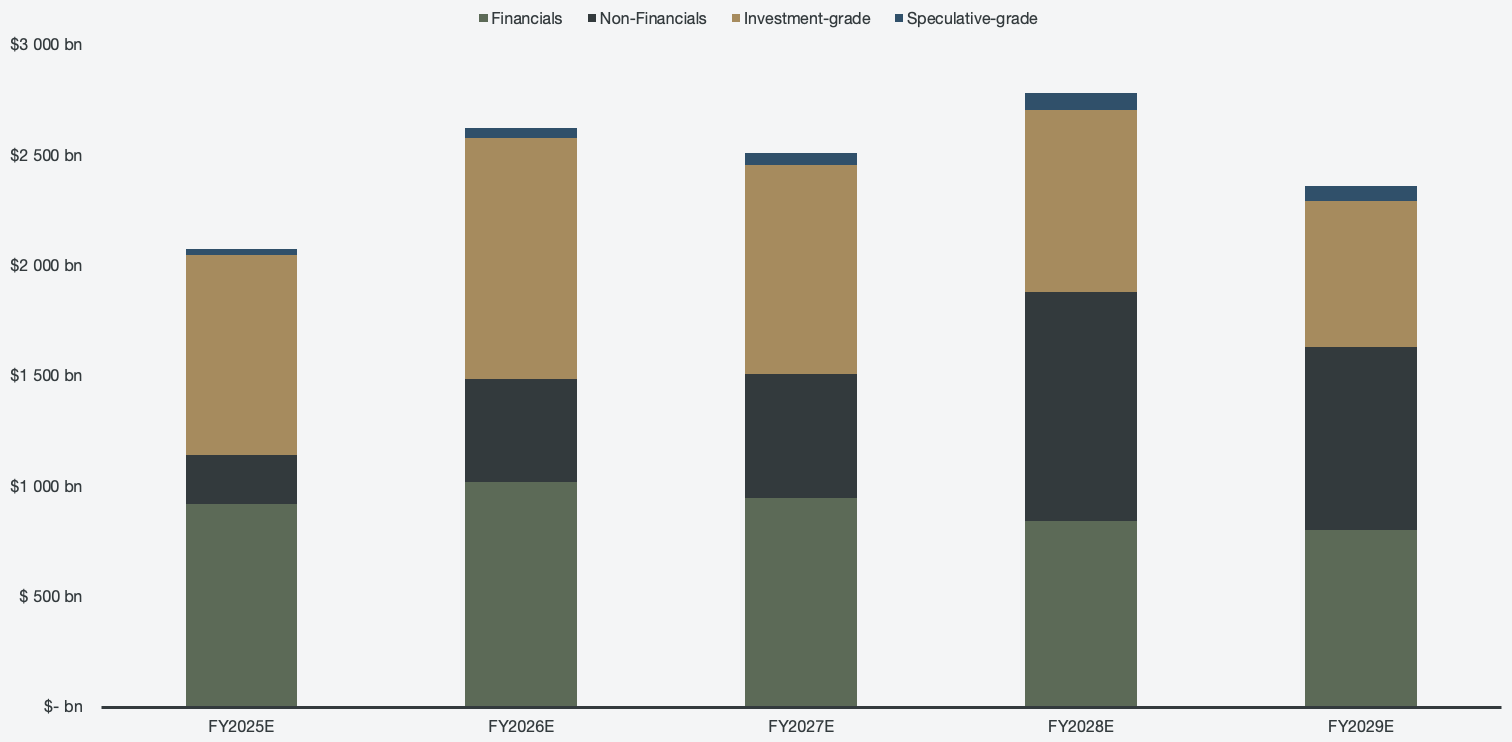

There is a debt maturity wall for the remainder of the decade, meaning periods with large concentrations of maturing debt. Investors can view this as a bridge; everyone needs to cross it within a deadline, but we don’t know exactly when. However, when the bridge is crossed, S&P Global collects fees as a toll booth.

Figure 1: Global maturity schedule, $ billions

The ratings business is high revenue and high margin, but it’s not the only one. The indices business has ~70% operating margins, as an example, and on a consolidated basis, the operating margin is ~40% across all segments. What’s more impressive is that S&P Global is very capital-light and doesn’t require a lot of reinvestment, which translates to 43% free cash flow to the firm margins in 2024.

Figure 2: Segmented operating margins, %

Risks: Even the most robust businesses have risks, and for S&P Global, that risk is the market intelligence segment. It is a competitive product but faces strong competition from the likes of Bloomberg Terminal, FactSet, Refinitiv, and more. We are also entering a period in time where institutions are downsizing software spending for market analytics and instead choosing to incorporate AI solutions, which could mean that the segment may face more challenges.