Sanrio: Hello Kitty Is A Compounding Machine

Equity research report

Sanrio exhibits one of the most impressive turnaround stories that I have come across in the public equity markets. The business was founded half a century ago, sales and margins had stagnated and started dropping, and the business it operates in is not AI or another high-growth market. Despite that, Sanrio has managed to do the unthinkable: from a stagnating legacy business to a thriving cash-compounding machine.

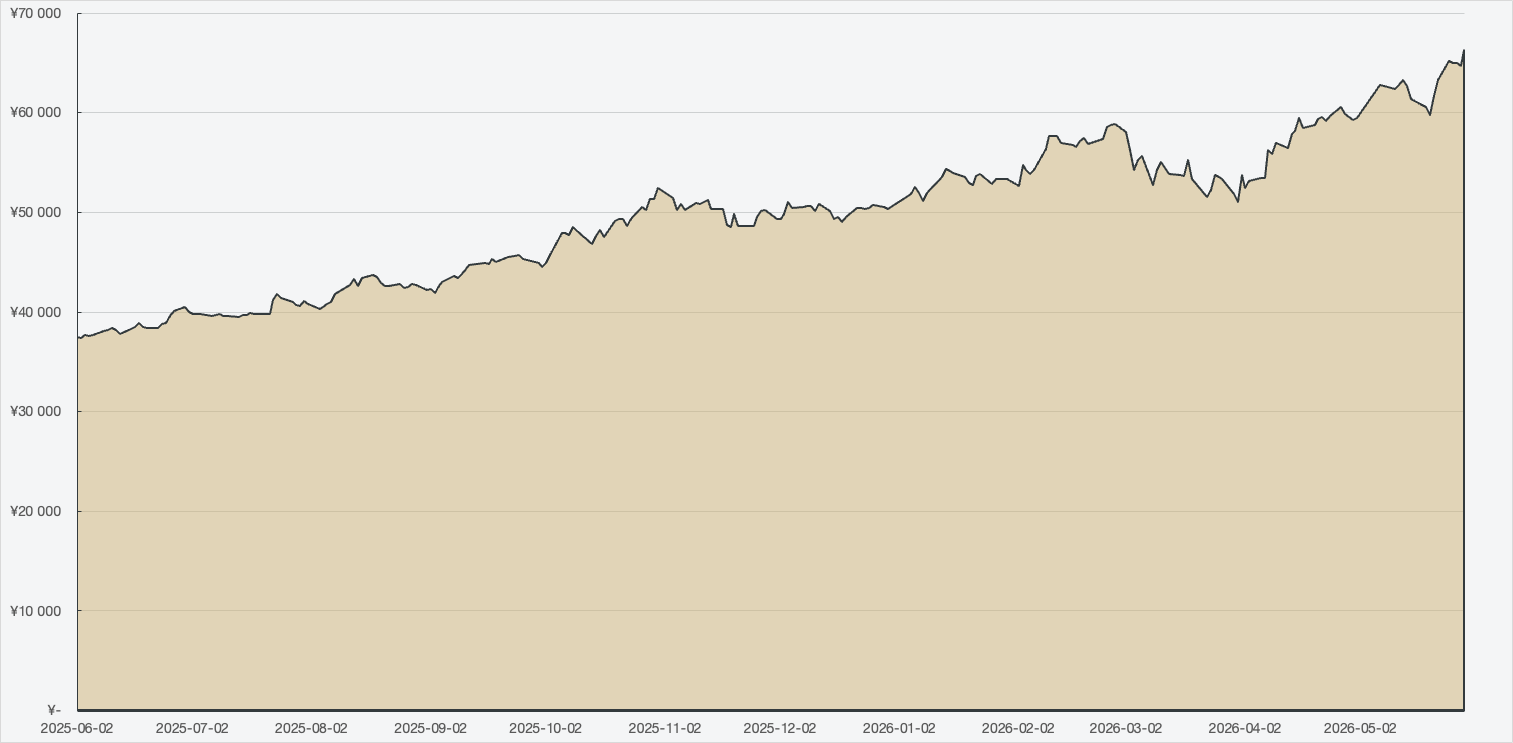

The story somewhat echoes that of the Japanese equity market, which has seen two decades of stagnant returns, only to rise up and accelerate massively. The Nikkei 225-index is up 77% over the past twelve months, and international eyes are turning to the Tokyo Stock Exchange once again. Sanrio is one of the more interesting names on that list, and one that is severely undervalued.

Price chart 1: Nikkei 225 index, 1-year quote history

Company profile

Theme: Compounding, Direction: Buy

Symbol: 8136, Exchange: TYO

Sector: Consumer Discretionary, Industry: Leisure, Apparel & Entertainment Retail

Fair intrinsic value: ¥1 696 (89%), as of June 2, 2026

Market capitalization: ¥1 109 696 million

Pricing data: P/S 6.05x, P/E 14.95x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

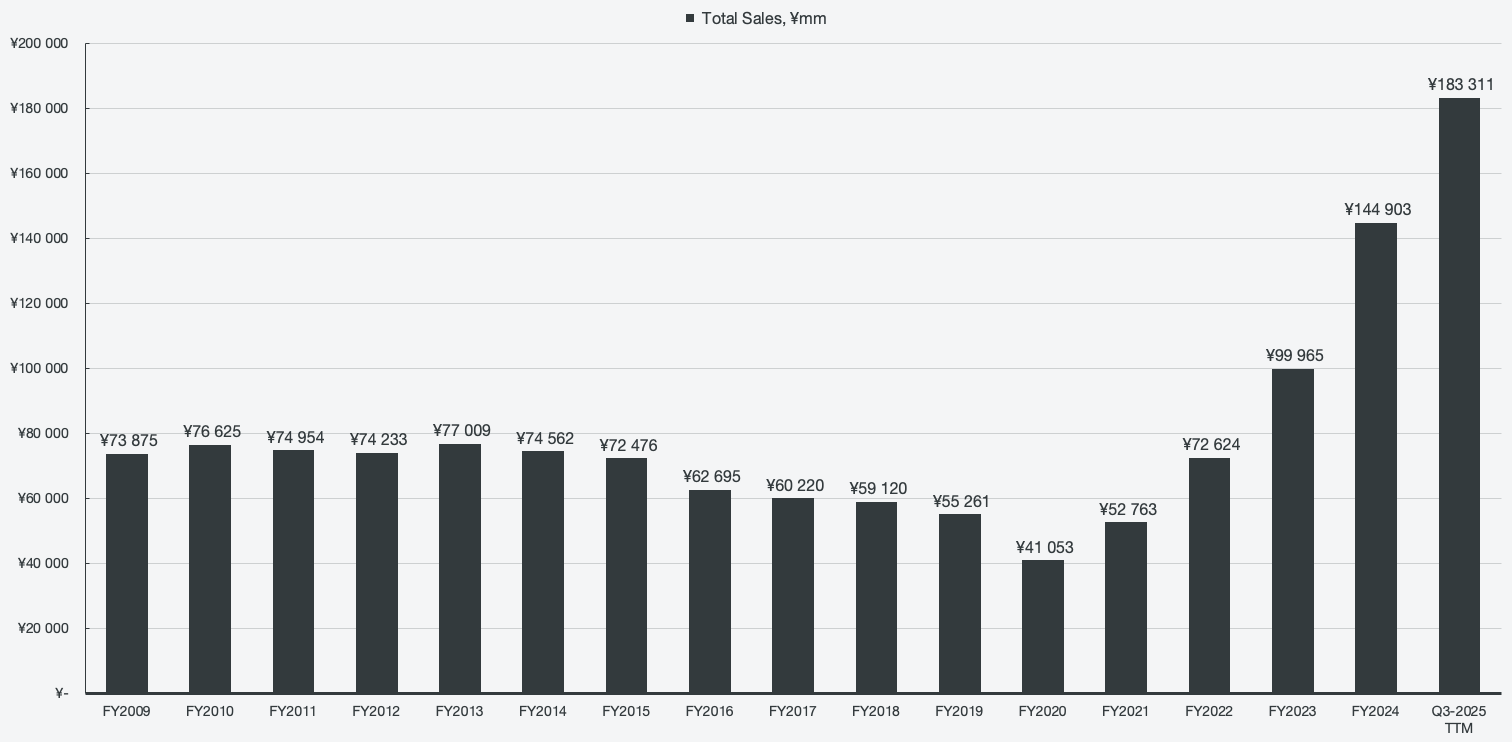

The explosive turnaround

Seldom does a chart paint a visual so vividly as the revenue history of Sanrio. A beloved brand with storied characters that frustratingly stood stagnant as a merchandise company until management recently engineered a revival. By bringing in new leadership and by centralizing brand management from a historically fragmented approach, Sanrio was able to have its second founding in 2020.

Figure 1: Historical revenues

Sanrio, famous for characters such as Hello Kitty, can be described as a character IP platform. Sanrio designs, licenses, and commercializes character-based IP across merchandise, retail, theme park experiences, and other emerging entertainment formats such as VR.

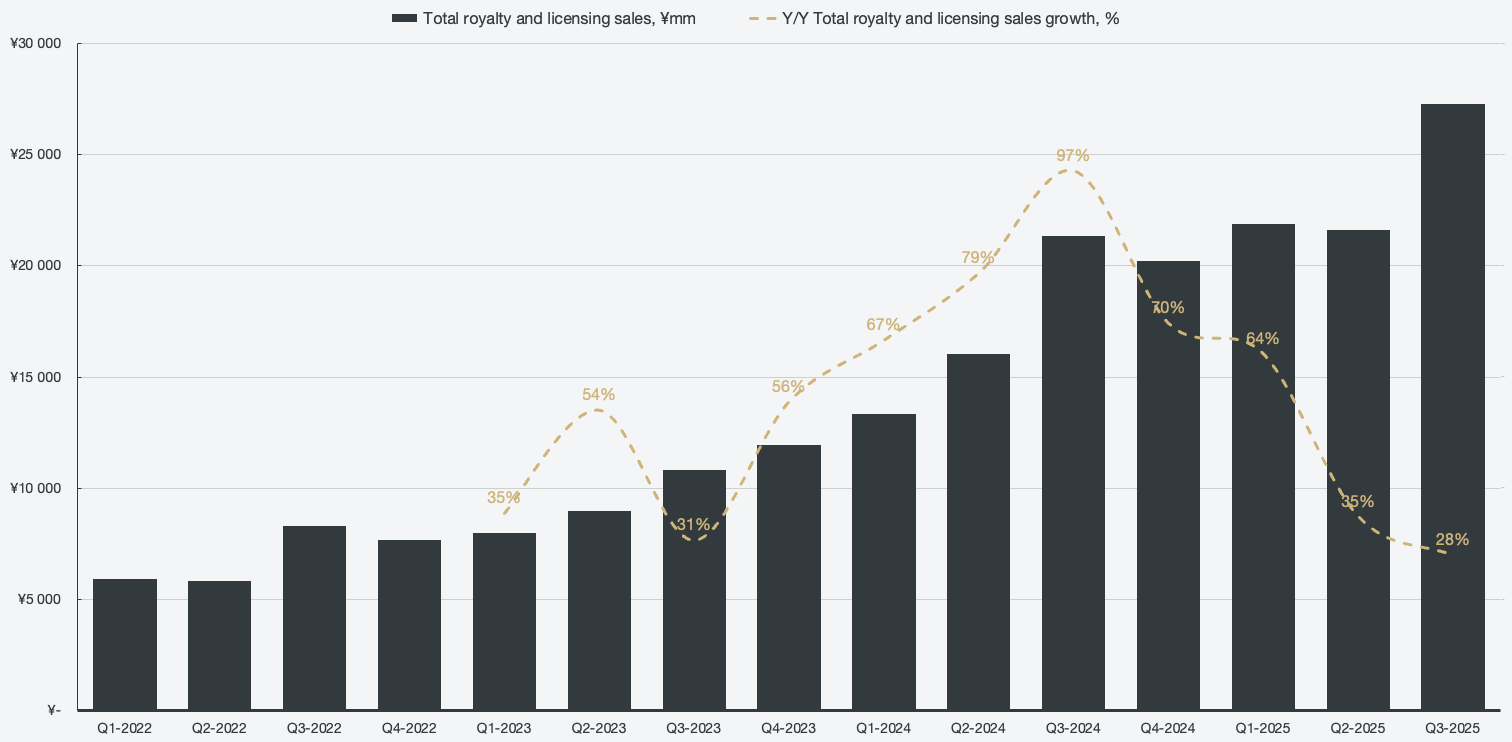

There are three main revenue segments, licensing being the most lucrative line of business. Royalties through licensing feature much more attractive margin profiles compared to traditional retail, are easily scalable, and do not carry inventory risk. Sanrio grants third parties the rights to feature Sanrio characters on merchandise such as toys, plushies, clothing, beauty products, stationery, and even food. It also grants the right to feature the characters in collaborations and various media content. Licensing and royalties currently account for about 42% of overall segment revenues.

Figure 2: Royalty and licensing revenue

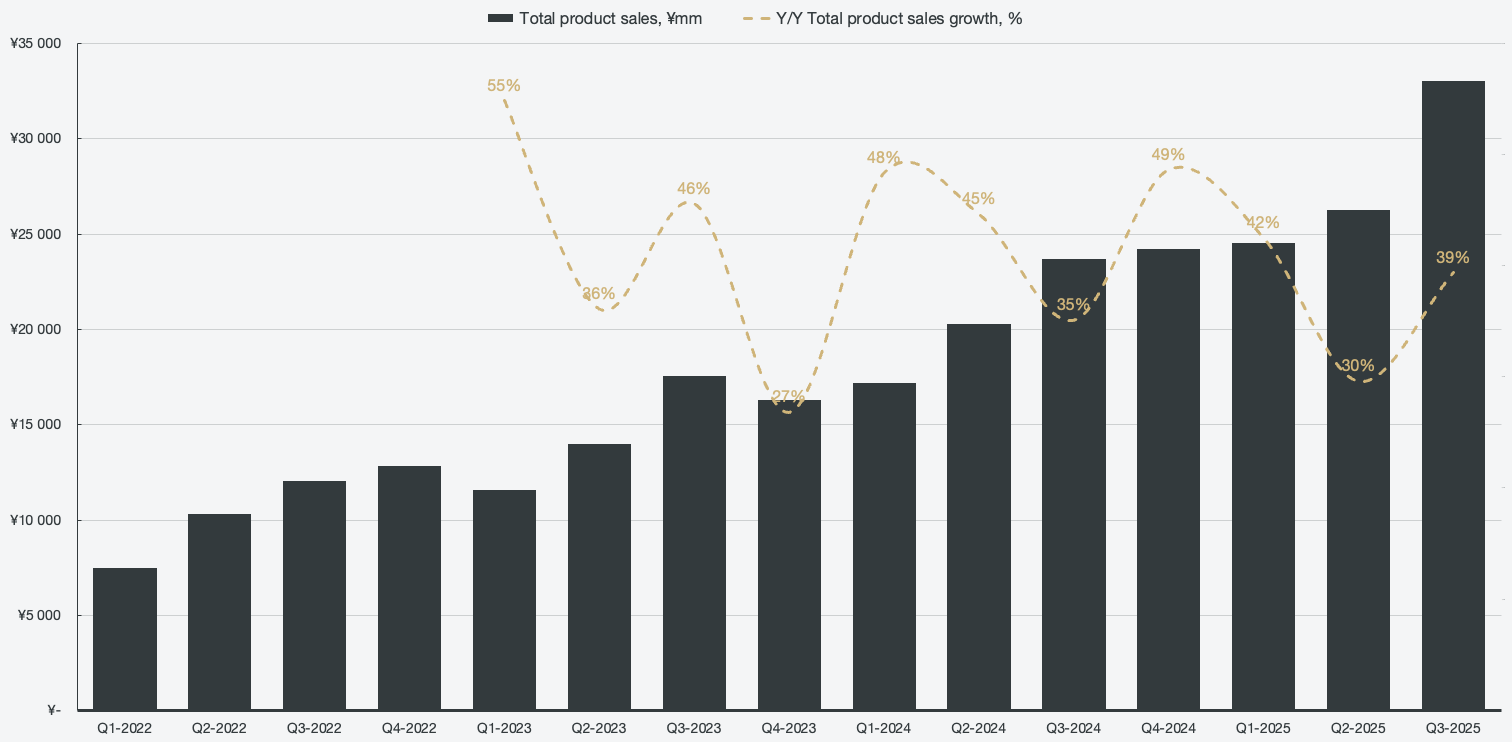

Accounting for about half of overall revenues is product sales, which comprise direct sales of its merchandise through Sanrio retail stores, e-commerce, and outlets. A simple, easy-to-understand line of business that has found rapid growth, even though a mix shift to licensing is preferred from a margin and risk perspective.

Figure 2: Product revenue

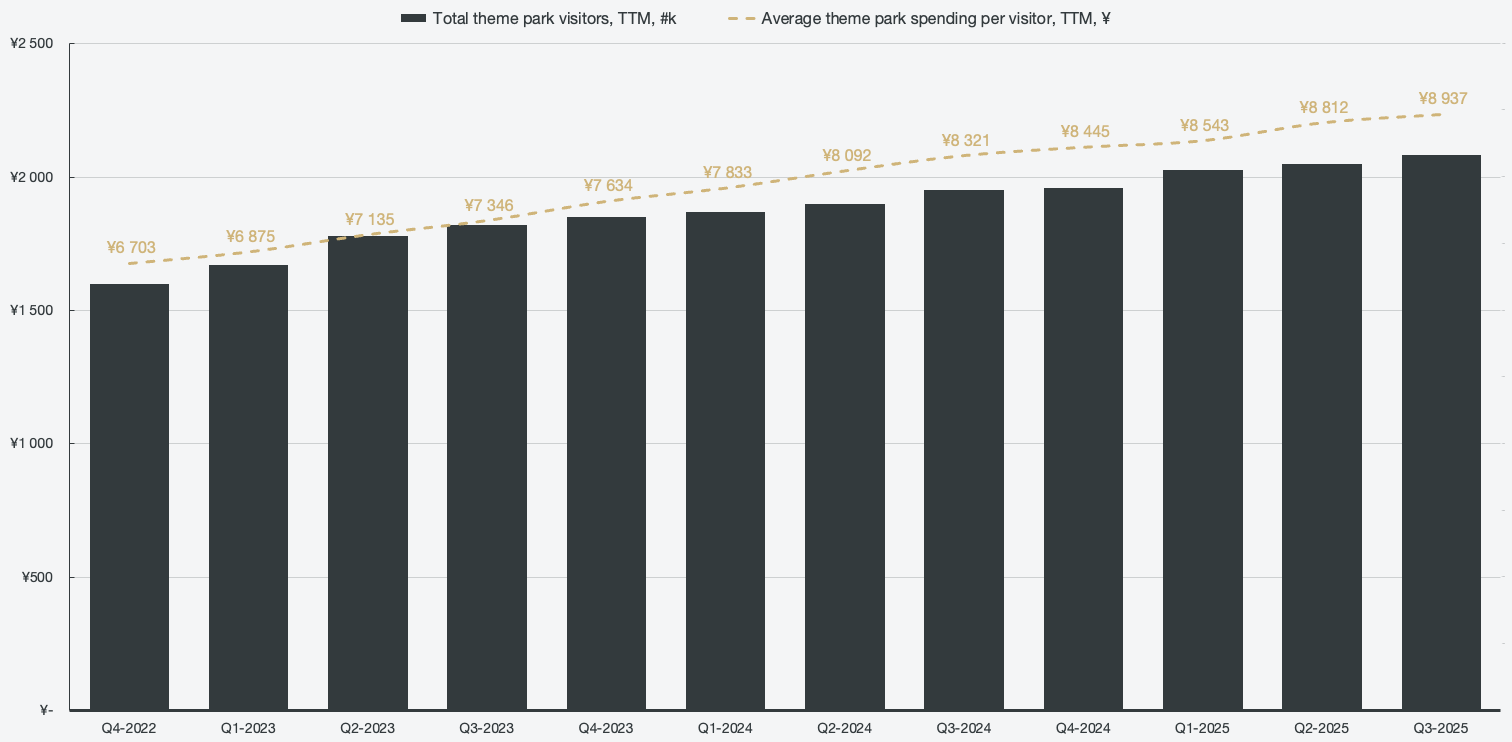

The third main segment is the theme parks Harmonyland and Puroland, as well as other types of experiences. The theme parks feature attractions, parades, character interactions, and in-park merchandise. The revenue the theme parks represent as a percentage of total sales is less than 10%, but their existence is important in order to drive overall enthusiasm for the brand. The average number of visitors to the theme parks keeps increasing, and so does the spending per person who visits the theme parks. The theme parks, despite limited capacity, drive an increasing amount of traffic through seasonal events and limited-edition merchandise.

Figure 3: Theme park visitors and spending per visitor, TTM

The reason the business was able to turn around and accelerate has several key reasons. The company had grown too reliant on Hello Kitty, and there was no clear path forward to grow interest in the character roster that now spans over 450 different characters. The first step was to start monetizing its global IP strategy, which included aggressive pushes into markets outside of Japan and diversification in its licensing. Hello Kitty was joined by other characters such as Kuromi, My Melody, Cinnamoroll, and others, many of whom are now more beloved than Hello Kitty in key markets.

The push for a more diversified portfolio of characters was bolstered by digital marketing in order to appeal to younger fans and new demographics. That included leaning into YouTube, social media channels, games, and other channels frequented by younger demographics in order to gather feedback and reduce reliance on physical retail stores. In the most recent character ranking globally, Hello Kitty ranks fifth, with Pompompurin, Cinnamoroll, Pochacco, and Kuromi ahead, in order from first. In some key markets like the U.S., Hello Kitty is not even in the top 10 at the time of writing. Another key reason for the turnaround was an improved licensing structure, where Sanrio focused on acquiring higher-quality partners and pushed more character mix and category selection. Going for quality over quantity allowed for improved brand control, as well as monetization per license.

Today, Sanrio looks less like a toy and gift seller and resembles a global, multi-channel character operator. The value now stems from a growing, globally monetized IP flywheel with better reach, better licensing, broader character use, and tighter brand control. The flywheel is simple:

Character creation and brand building → Spread awareness through merchandise, stores, digital channels, collaborations, and theme parks → Scale the characters into many product categories and geographies through licensing → Higher visibility feeds fan engagement and character demand → Reinvest in digital content and further expansion, IP protection, and further character creation → Repeat the cycle.

Understanding the geographies and segments

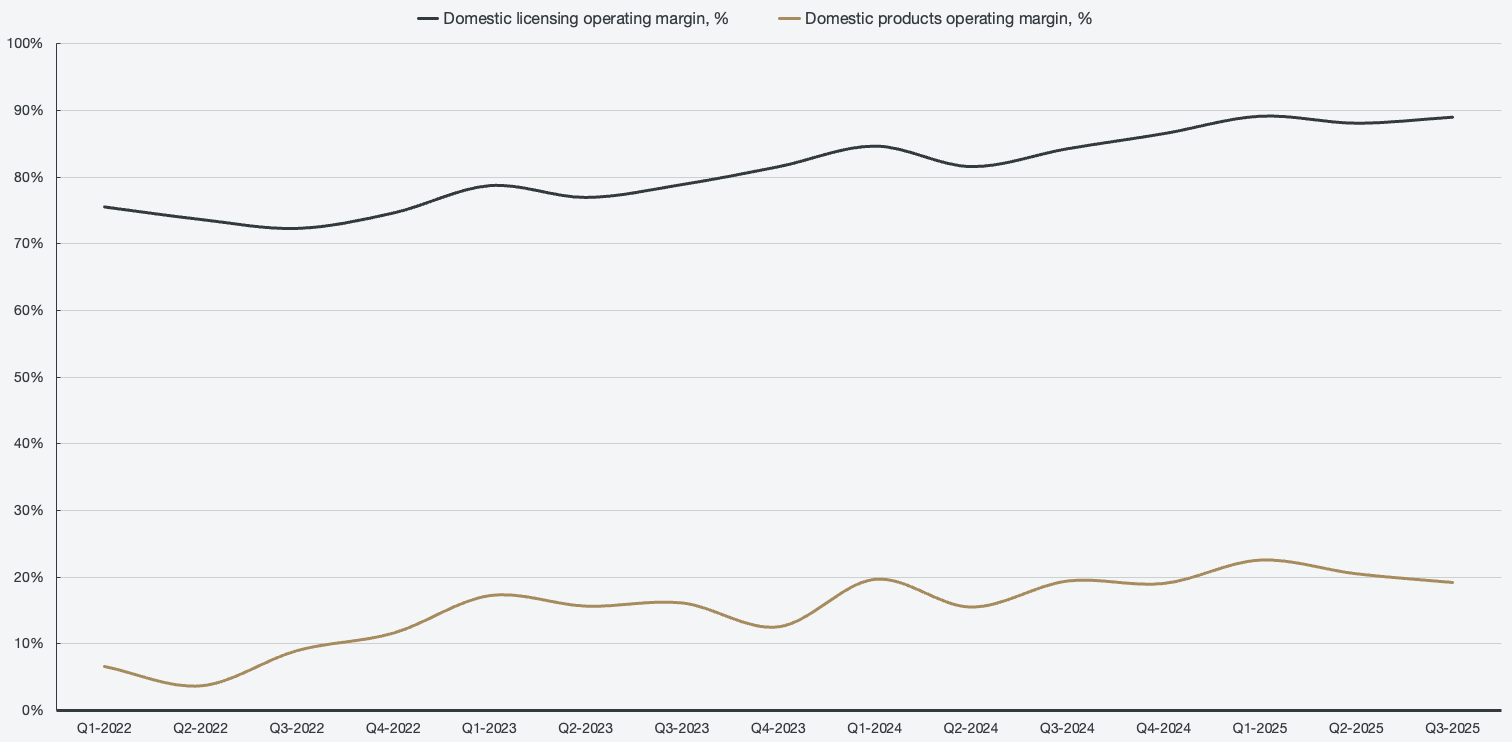

While the revenue chart tells of an impressive turnaround narrative on its own, it is necessary to look deeper in order to grasp the dynamic fueling the growth. Most important of all is understanding why a mix shift towards licensing is substantially more lucrative for Sanrio. I already mentioned that licensing carries less risk and that it has a more attractive margin profile. However, much like the turnaround story, a chart vividly paints the picture of how much more attractive the licensing margins are.

Figure 4: Segmented domestic operating margins

Segmented operating margins in the 80-90% range are on par with the most oppressive, high-moat, and unfair businesses in the world.