Virtu Financial: The Perfect Hedge

Hedging is associated with securing a contrarian position to ones portfolio allocations in order to protect the total value. If one does poorly, the idea is that the other will do well. However, there is a hedge that rewards investors during calamities as well as during good markets, and that is Virtu Financial.

Company profile

Theme: Hedge, Direction: Buy

Symbol: VIRT, Exchange: NYSE

Sector: Financials, Industry: Capital Markets

Fair intrinsic value: $58.40 (+36%), as of June 26, 2025

Market capitalization: $6 650 million

Pricing data: P/S 1.55x, P/E 12.46x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

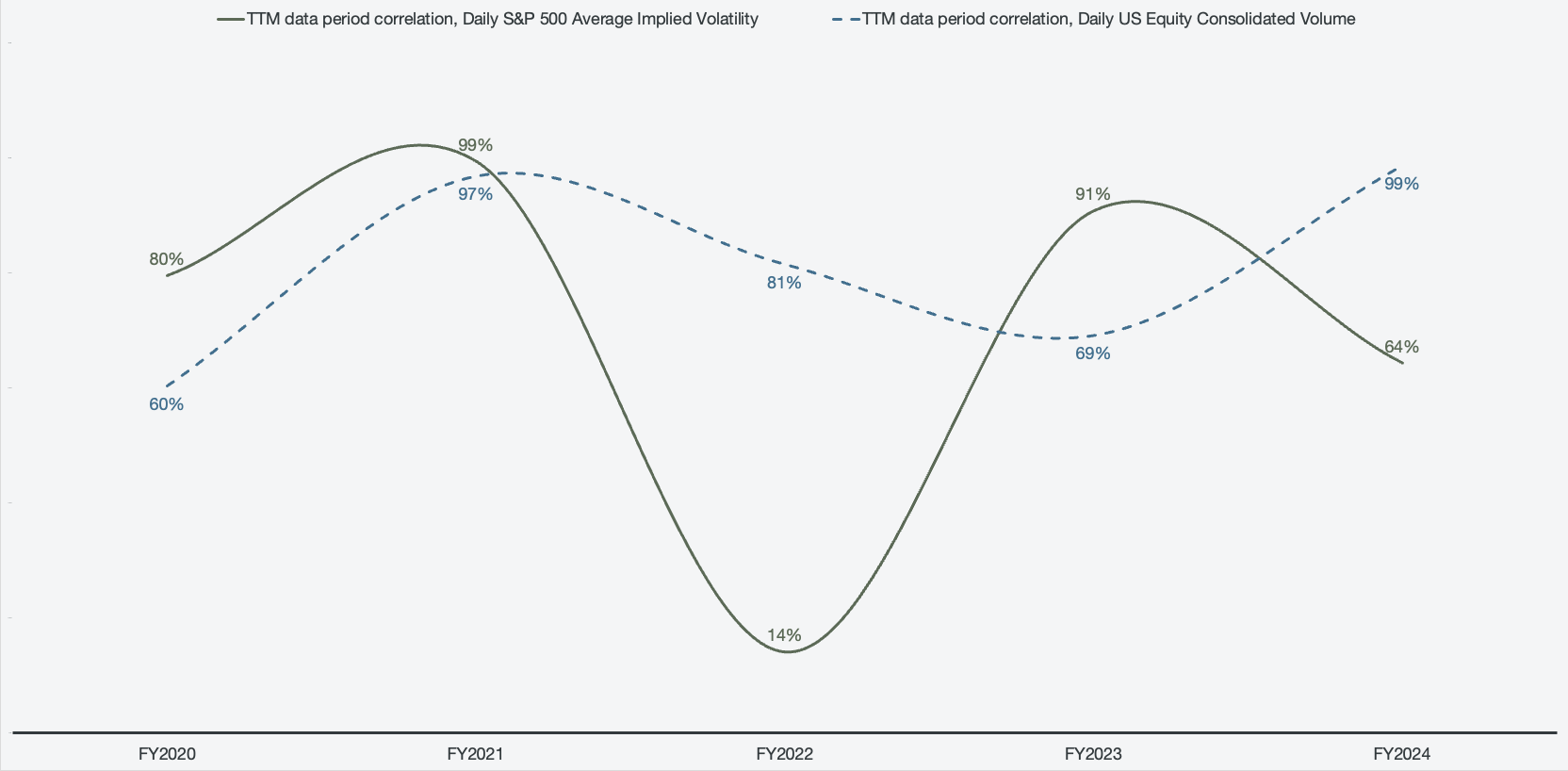

Virtu is a market maker that generates revenue frommarket making, trading, and execution services. The business thrives when there are spread opportunities across various trading instruments, often boosted by a lot of volume as well as volatility. This means that when money is piling into the stock market, it is good for Virtu; likewise, when there is a panic and a lot of selling, it is also good for Virtu.

Figure 1: Net trading income correlation to market activity

The glaring hole in the thesis is: what happens when markets are relatively calm? To cover this inherrent weakness to the business model, there are organic growth initiatives within Virtu; revenue that doesn’t rely on the whims of market activity. However, in terms of driving pure shareholder returns, Virtu is issuing a stable dividend while also repurchasing outstanding shares at an impressive pace. Since 2021, Virtu has repurchased close to 30% of all outstanding shares.

Figure 2: Segmented operating margins, %

This dynamic creates a hedge that rewards shareholders for owning the stock. If capital markets see sell-offs, that volatility event will drive higher trading income for Virtu. If markets are rallying, the volume will drive trading for Virtu. If markets are relatively static, Virtu will return shareholder value through dividends and share repurchases. In addition, the stock is trading well below fair intrinsic value which makes it an attractive buy in all scenarios.

Risks: One of the bigger risks that investors need to be aware of is that Virtu’s business currently heavily relies on external factors out of their control. They are a market maker, and as such, a large majority of their revenue and profitability is directly driven by factors out of their control. To combat this, they have organic growth initiatives since 2021. However, organic growth still only accounts for 12.3% of net trading income, up from 7.8% in 2021.