Brookfield Asset Management: The Backbone Of AI

Equity research follow-up coverage, rating unchanged

Brookfield Asset Management is set to double every metric by 2030, indicating a 16-18% CAGR for all of its key metrics: Fee-bearing capital, fee-related earnings, and distributable earnings. They plan on doing so by using their unique position as one of the largest alternative asset managers in the world to invest in the future backbone of the world.

This is a steady and predictable business by nature, which means that the quarterly intrinsic valuation does not move drastically. However, since my last research report on the business, the stock has traded down slightly, which has opened up the upside to fair intrinsic value significantly.

Company profile

January 19, 2026 Follow-up coverage

Direction: Buy

Previous fair intrinsic value: $67.39, as of August 24, 2025

Symbol: BAM, Exchange: NYSE, TSX

Sector: Financials, Industry: Asset Management

Theme: Compounding

Fair intrinsic value: $69.15 (31%), as of January 19, 2026

Market capitalization: $86 169

Pricing data: P/S 19x, P/E 35x

Previous coverage:

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

Positioning for secular growth

BAM retains its position as one of the best and most consistent capital allocators at scale. A key to BAM’s results and high IRR is positioning for secular megatrends, and that is what they have been doing as of late. The three large megatrends on our doorstep is AI and digitalization, deglobalization, and decarbonization, which are expected to require over $100 trillion of capital.

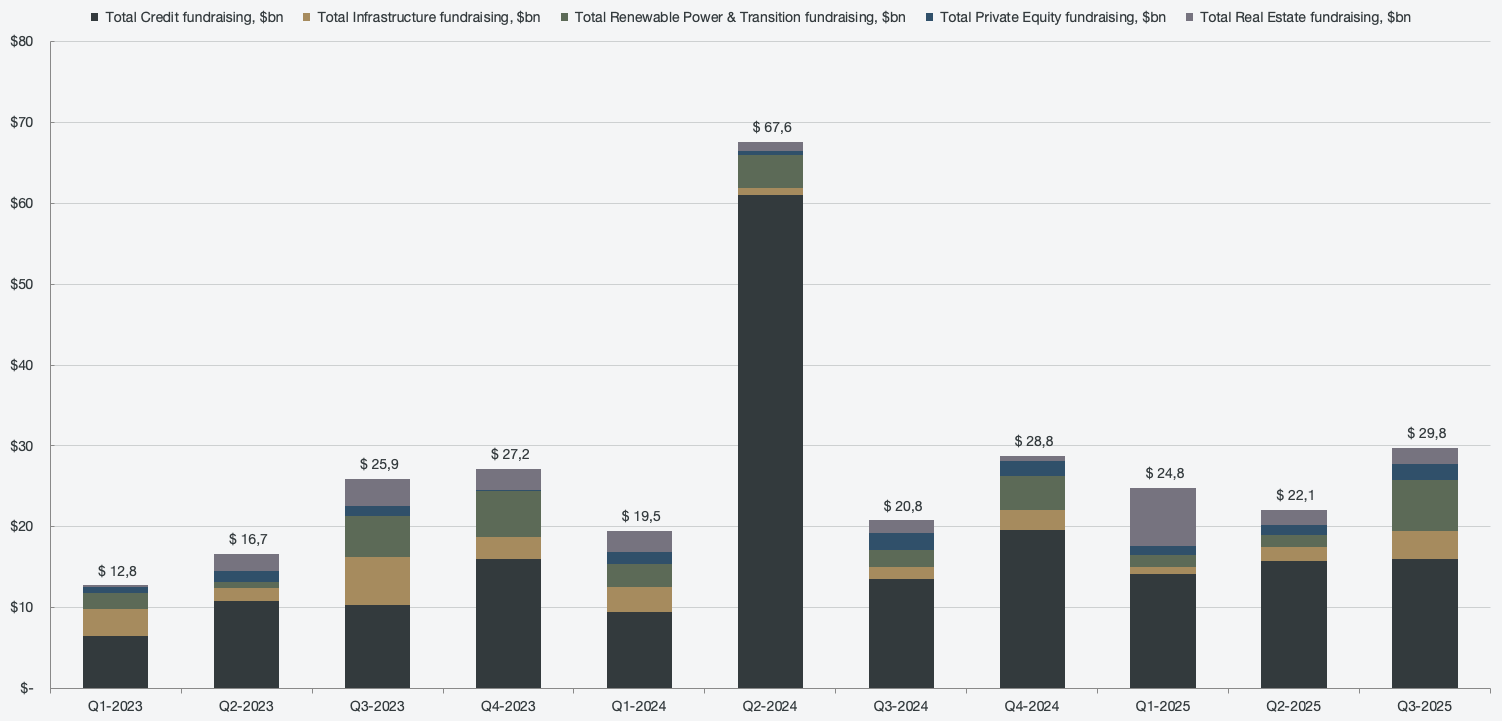

Over the next 10 years, AI infrastructure spend alone is expected to surpass $7 trillion. Each step of the global AI expansion, be it across corporates or governments, are covered by Brookfield’s portfolio strategies. They cover infrastructure, real estate, renewable power, private equity, and credit, and have the ability to raise capital at scale. With access to all major pools of capital (institutional, insurance, private wealth, and public markets), Brookfield has reached another high in terms of fundraising. The company has raised $30 billion in Q3 2025, and $106 over the past twelve-month period.

Figure 1: Segmented fundraising

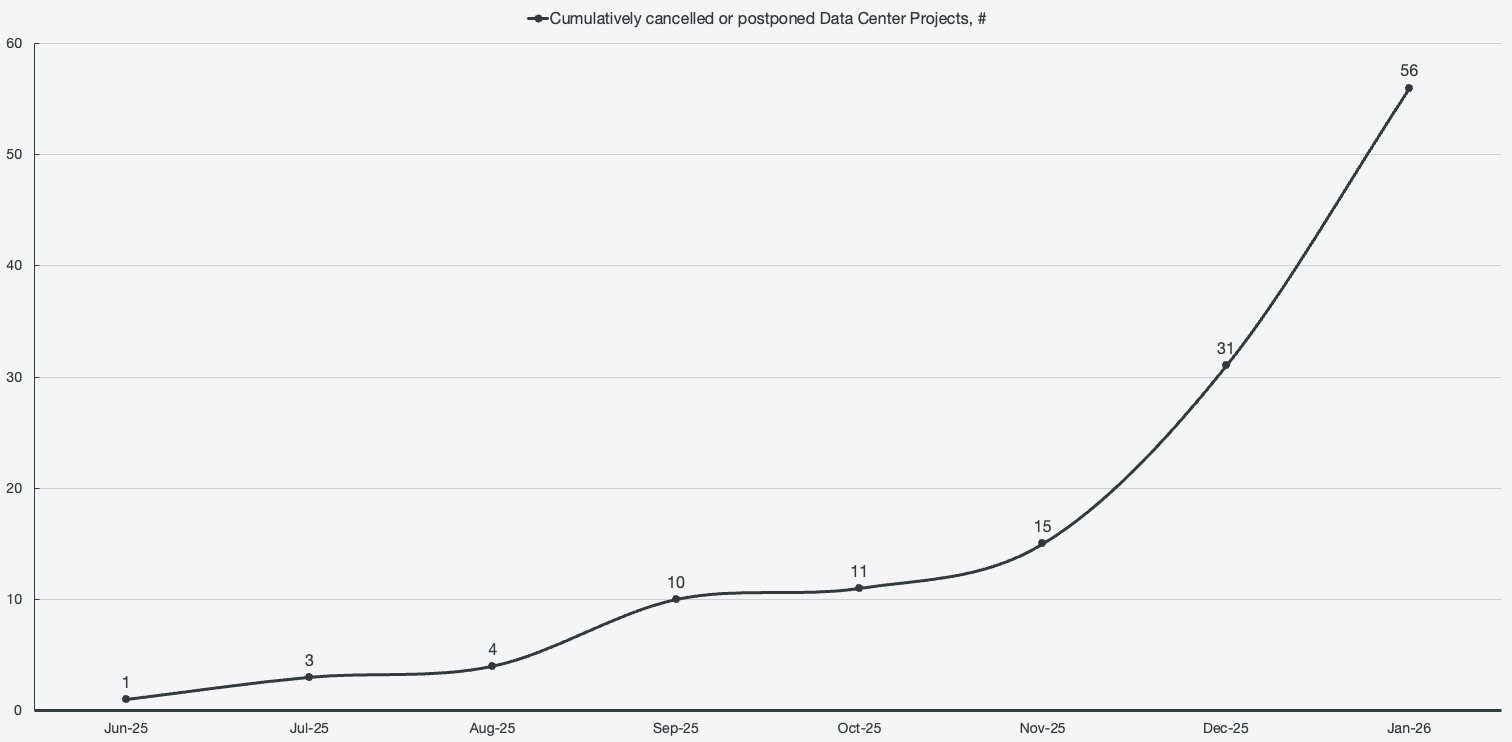

The credibility that Brookfield has built over a long period of time becomes important as they target strategies with a lot of outside excitement. For example, we are all aware of AI compute demand. There are ambitious commitments of trillions in capital expenditures across the world’s largest companies. However, since June of 2025, there has already been 56 postponed or cancelled data center projects. That trend is starting to exponentially increase, creating a playing field where Brookfield can differentiate itself as a world class operating partner.

Figure 2: Cancelled or postponed data center projects, cumulative

Among alternative asset managers, Brookfield is widely regarded as the global leader across infrastructure, renewable power, and energy transition, which makes them the natural partner for this type of project. The two other “super majors” in the space are Blackstone, which is the undisputed leader in real estate, and Apollo, which is the leader in credit and insurance. Brookfield is differentiated from peers since they have always been an owner-operator of industrial assets. The reputation for having operational boots on the ground has resulted in significant credibility for having expertise in engineering and project management, rather than simply being a capital allocator like peers. That moat makes them the first call for projects within the current secular themes.

On pace for doubling the business

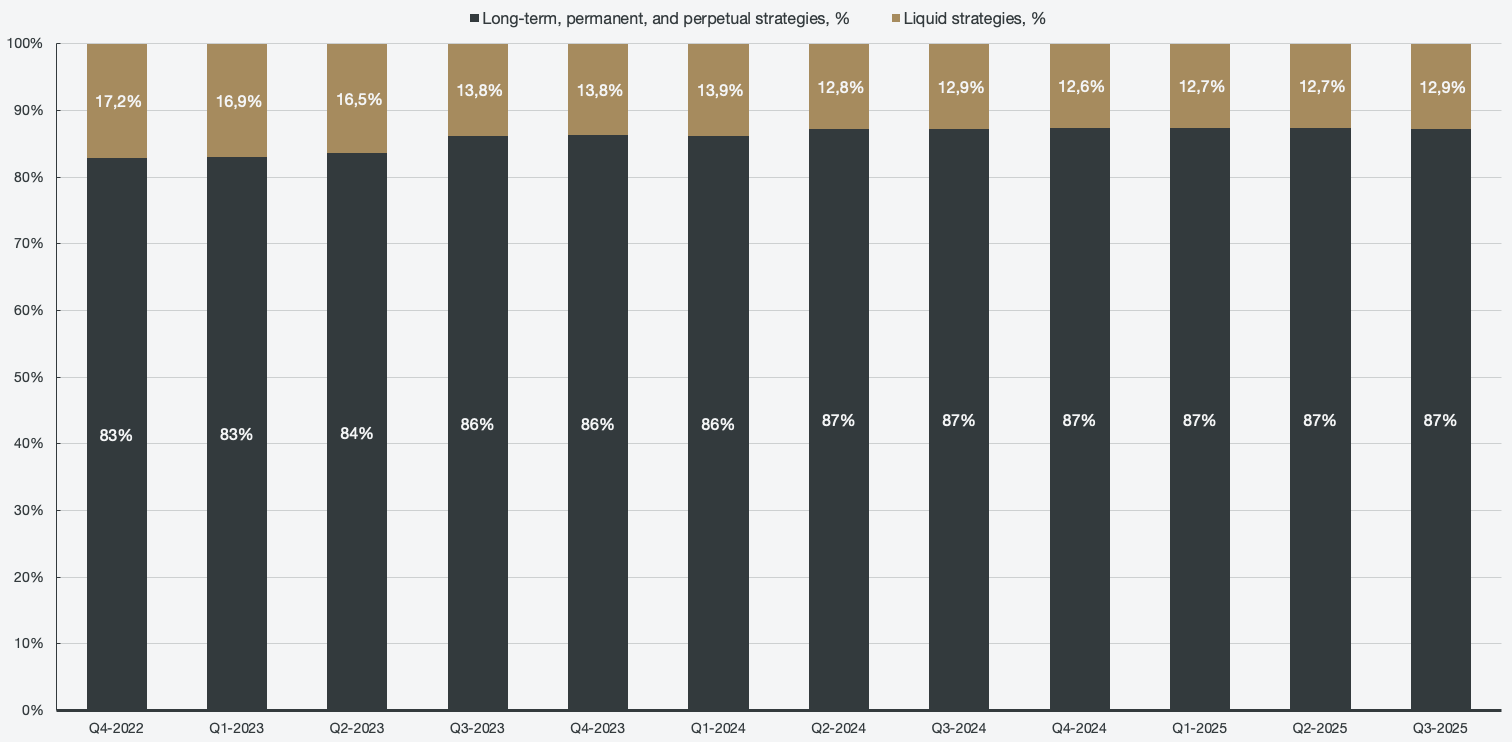

As mentioned in my previous piece, Brookfield has the ambitious intention of roughly doubling the business by 2030. The core characteristics of the business makes financial performance largely predictable. These characteristics include a large majority of the fee-bearing capital being held for long-term, permanent, or perpetual capital. Only 13% of FBC is allocated to liquid strategies as of Q3 2025.

Figure 3: Fee-bearing capital by strategy

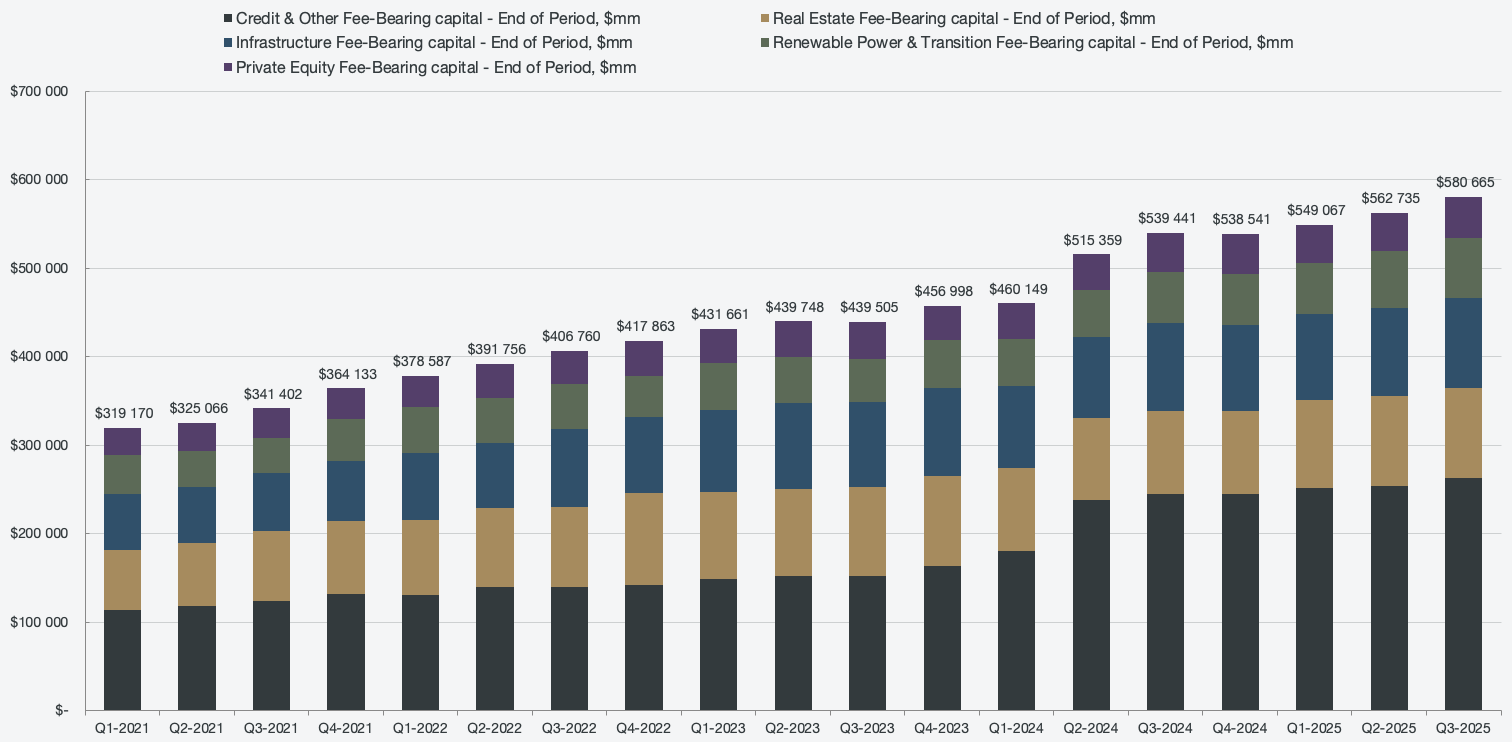

The most important metric to track for BAM is the total amount of fee-bearing capital, as not all AUM generates fees. The annualized net flows for the Q3 2025 period were 14.8%, with a net increase of $17,93 billion, an 8% increase Y/Y.

Figure 4: Segmented fee-bearing capital

However, simply growing fee-bearing capital does not tell the full story. Different segments of the FBC have different yield profiles. For example, credit is currently the largest segment but features the lowest yield in terms of fees at 0.17%. The highest yielding strategy is renewable power & transition at 0.34%, and on a consolidated basis, yield currently sits at 0.24%.

The MER is another metric that allows us to track how much the company is being paid for managing capital.

Where F=base management & advisory fees, A=average fee-bearing capital, d=days in period, D=days in year.

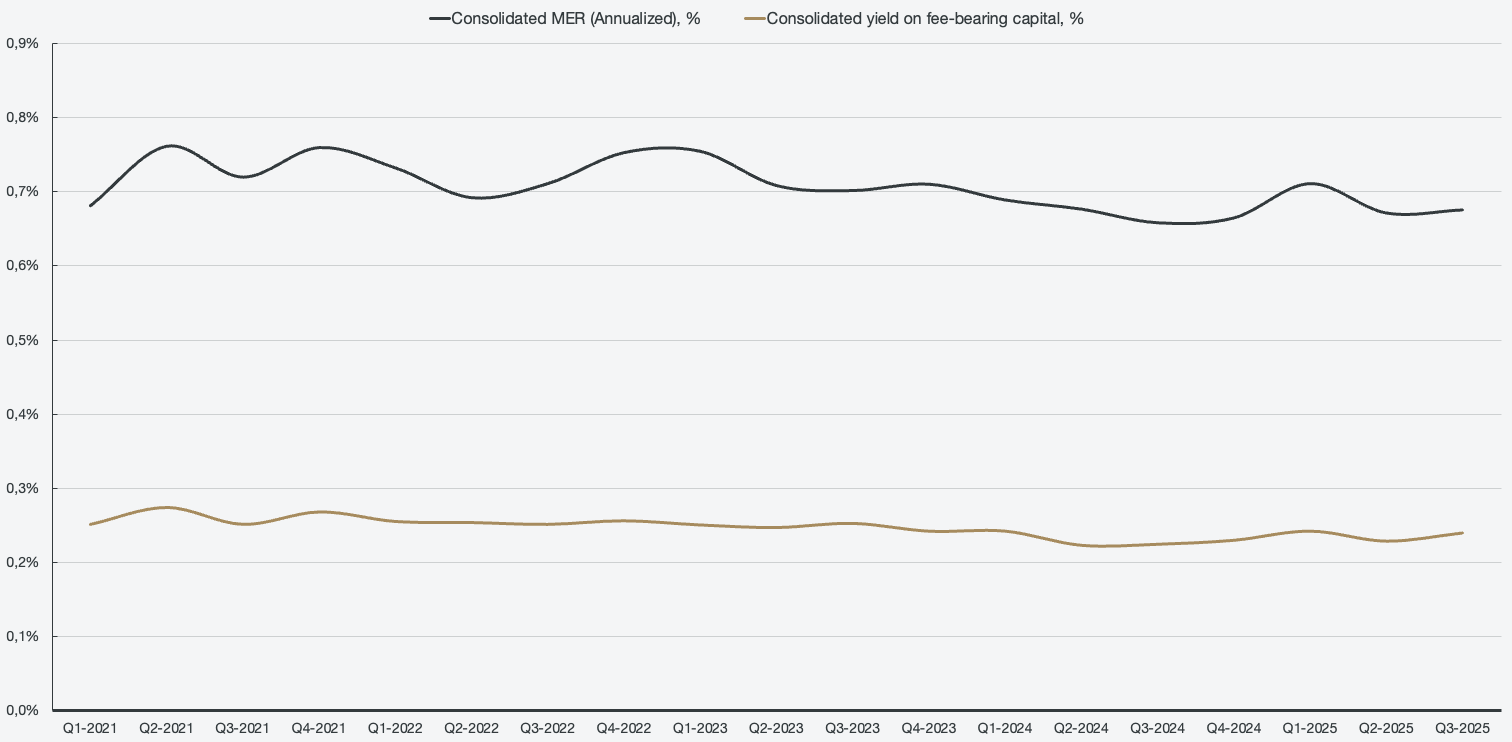

Figure 5: Fee-bearing capital yield, management expense ratio

The average FBC yield over the past three years is 0.24%, which is exactly where it sits for Q3 2025. The average MER is slightly below where it has been on average for the past five years, which is explained by leaning heavier into the credit strategy since 2023 and onwards. Management makes it clear that the long-term goal is to scale credit to the same yields as the other strategies and emphasizes that lower yield does not mean lower margin. The credit segment is highly strategic for the business since it allows Brookfield to raise scale capital. In addition, credit accounted for 51% of inflows for the quarter, showing how lucrative the strategy is to outside investors.

As mentioned in the previous research piece on BAM, this is a compounder by nature, and by all metrics, business is as usual. This is one of those boring kind of companies that grow seemingly perpetually and return shareholder value. Therefore, it is unlikely that any one single quarter will showcase divergence. As long as Brookfield operates according to the saying “business as usual”, then it is on the right track.