FICO: Q2 Proves That FICO Is Undisruptible

Equity research follow-up coverage, rating unchanged

Near as we can tell, nobody’s paying for VantageScores. The bureaus send along the VantageScore for free when someone buys a FICO Score. You know, when you see the big VantageScore score volumes that VantageScore talks about, you should know that they’re largely unpaid for. You know, are they? Is anyone using them? Don’t know. Is anyone paying for them? Our sense is not much. You know, it’s pretty hard to triangulate on what their market share is. I mean, I think it’s trivial, is what I would say. I think you see that in our numbers, right? I mean, if we were losing market share, you’d see it in our numbers, and you don’t see any of that.

William Lansing, Chief Executive Officer

Fair Isaac Corporation, Q2 2026 Earnings Conference Call

CEO William Lansing reiterated what he said back in 2024: VantageScore is not a competitive threat. VantageScore is not taking any market share from FICO, and the large volumes are credited to the bureaus shipping a free VantageScore with each FICO pull. Even though VantageScore is being offered for free, no one is switching over.

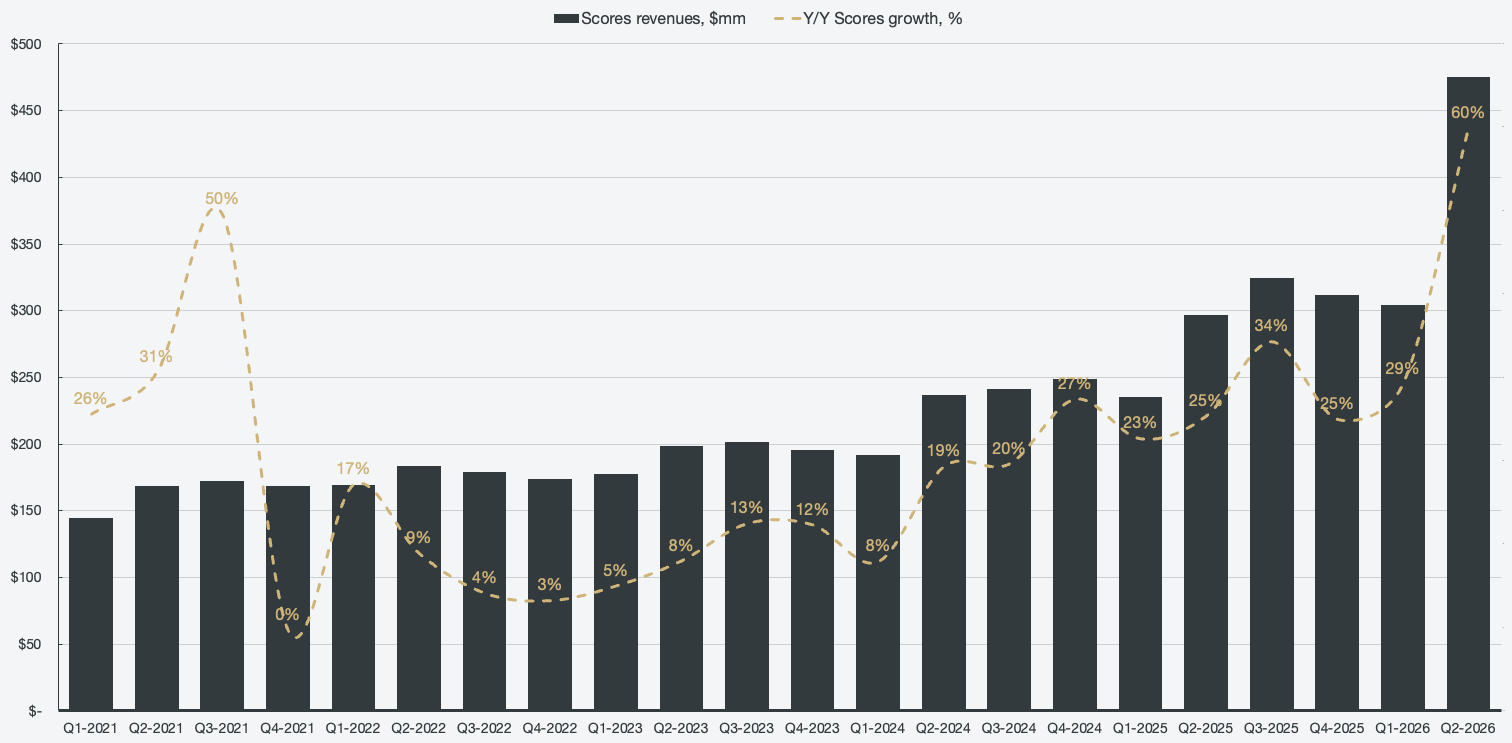

As Lansing said in the Q2 earnings conference call, if FICO was losing market share, you’d see it in the numbers. What the numbers showed was a 60% Y/Y growth in Scores. The market has not yet woken up to the fact that FICO is undisruptible, presenting potential investors with a very attractive opportunity.

Company profile

May 2, 2026 Follow-up coverage

Direction: Buy

Previous fair intrinsic value: $2051.6, as of March 31, 2026

Symbol: FICO, Exchange: NYSE

Sector: Technology, Industry: Software - Application

Theme: High quality

Fair intrinsic value: $2116 (104%), as of May 2, 2026

Market capitalization: $25 433 million

Pricing data: P/S 11.3x, P/E 33.5x

Previous coverage:

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

The best business model in the world continues to dominate

In my previous research coverage of FICO, I detailed how FICO’s stock collapse is more or less fabricated. The FHFA Director and, most recently, Senator Hawley have both targeted FICO for its pricing power. The claim is that FICO’s price increases have been hurting borrowers. The reality of the situation is that the total production expense per loan started increasing sharply before FICO’s price hikes. After increasing the price to pull a score by 725%, the TPE/loan remained static compared to when FICO began increasing prices, proving that FICO scores have no meaningful impact on the borrower’s costs. A FICO pull makes up ~0.03% of TPE.

The real reason is probably that the optics are bad for FICO. A cold housing market needs a scapegoat, and pointing at FICO, which is exercising its pricing power, is the simplest approach to avoiding scrutiny in areas that are actually causing housing to be unaffordable. However, before FICO’s price increases, the bureaus and resellers had a 1844% markup, and after a 725% increase, the markup is still ~650%. FICO is, in my opinion, fully justified in increasing prices, as the muddied line item that traditionally comes with a FICO pull does not break down the excessive margin that bureaus are charging. FICO’s direct licensing program makes the process a lot more transparent for lenders, while also making it more difficult for others to charge excessive markups. For more details, see my previous piece on FICO.

To combat FICO, FHFA has allowed GSEs to use VantageScore, a score that the industry has not switched over to, despite it being sent along for free with each FICO score. As Lansing said in various earnings calls (including Q2 2026), VantageScore’s volumes are fabricated, and in reality, VantageScore has ~2% market share or even less. The whole industry speaks FICO, and even free is too high a cost to make the switch to VantageScore. However, the market still views VantageScore as a real threat, despite FICO reporting 60% Y/Y growth in the segment.

Figure 1: Score revenue and score revenue growth

FICO, throughout the noise, has managed to find a way to increase pricing even further, while being perceived more lightly. The old performance model in the mortgage direct licensing program was priced at $4.95 per score, with a funding fee of $33. The new performance model is $0.99 per score, with a $65 funding fee, a 74% increase, while also addressing a point raised by Senator Hawley in his letter:

These price increases are most damaging to the Americans who can least afford them. First-time homebuyers bear a disproportionate burden of the cost. They typically undergo multiple credit checks during the home-buying process—at prequalification, at formal application, and often again before closing—and frequently pay for credit pulls on applications that do not result in a funded loan.

Senator Hawley’s oversight letter to FICO, March 23, 2026

We already know from my last piece that the prices of FICO pulls are immaterial, but this way, the perception is improved, which should help with scrutiny over FICO’s pricing power.

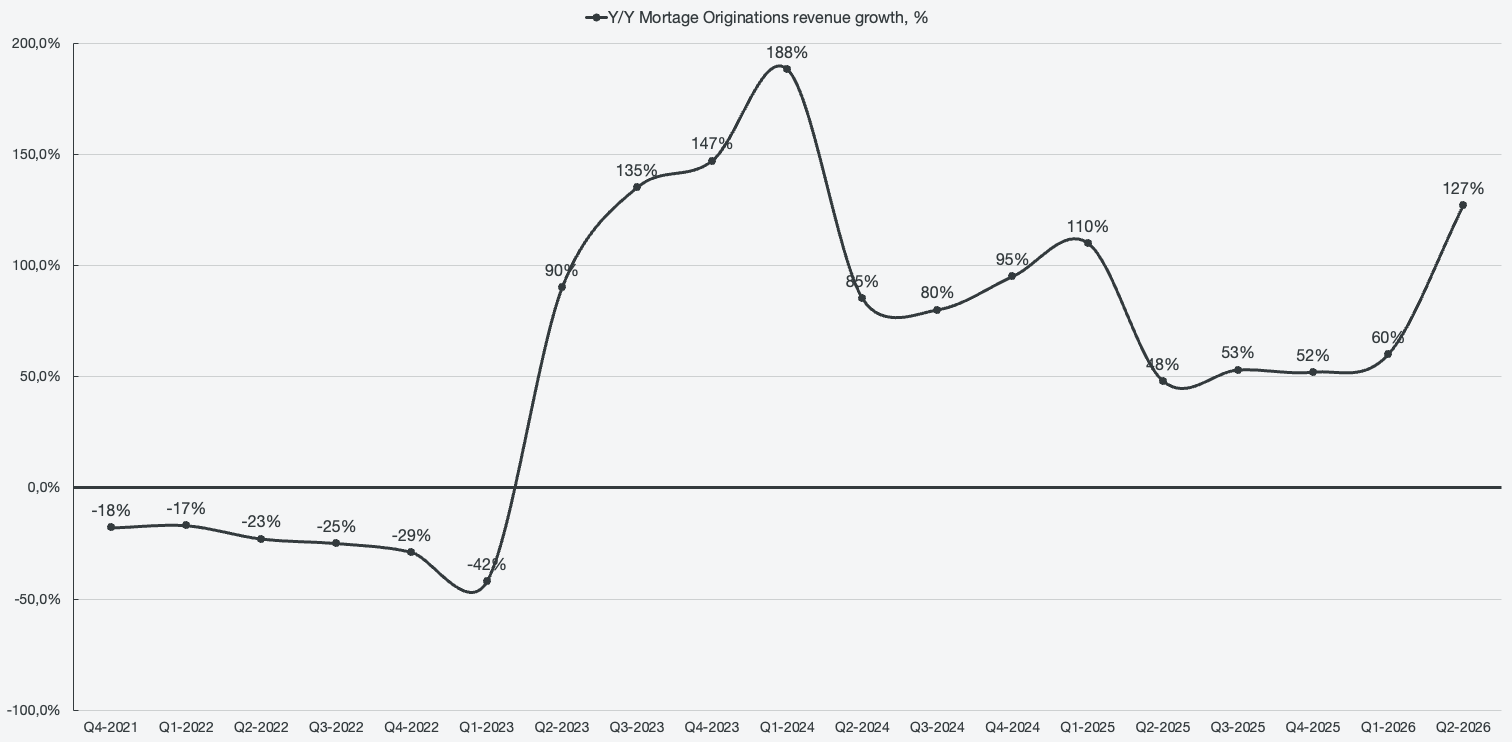

Looking at mortgage originations revenue growth, we saw another massive quarter, growing 127% Y/Y. That is another nail in the coffin against the argument that FICO’s price increases are actively hurting the mortgage market. With the performance model reducing average per-score fees by 50% or 90% (for classic FICO and FICO Score 10T, respectively), and the per-score model being the same price on average as in 2025, FICO was confident enough to increase the revenue guidance for the fiscal year to $2.45 billion from $2.33 billion.

Figure 2: Mortgage originations revenue growth

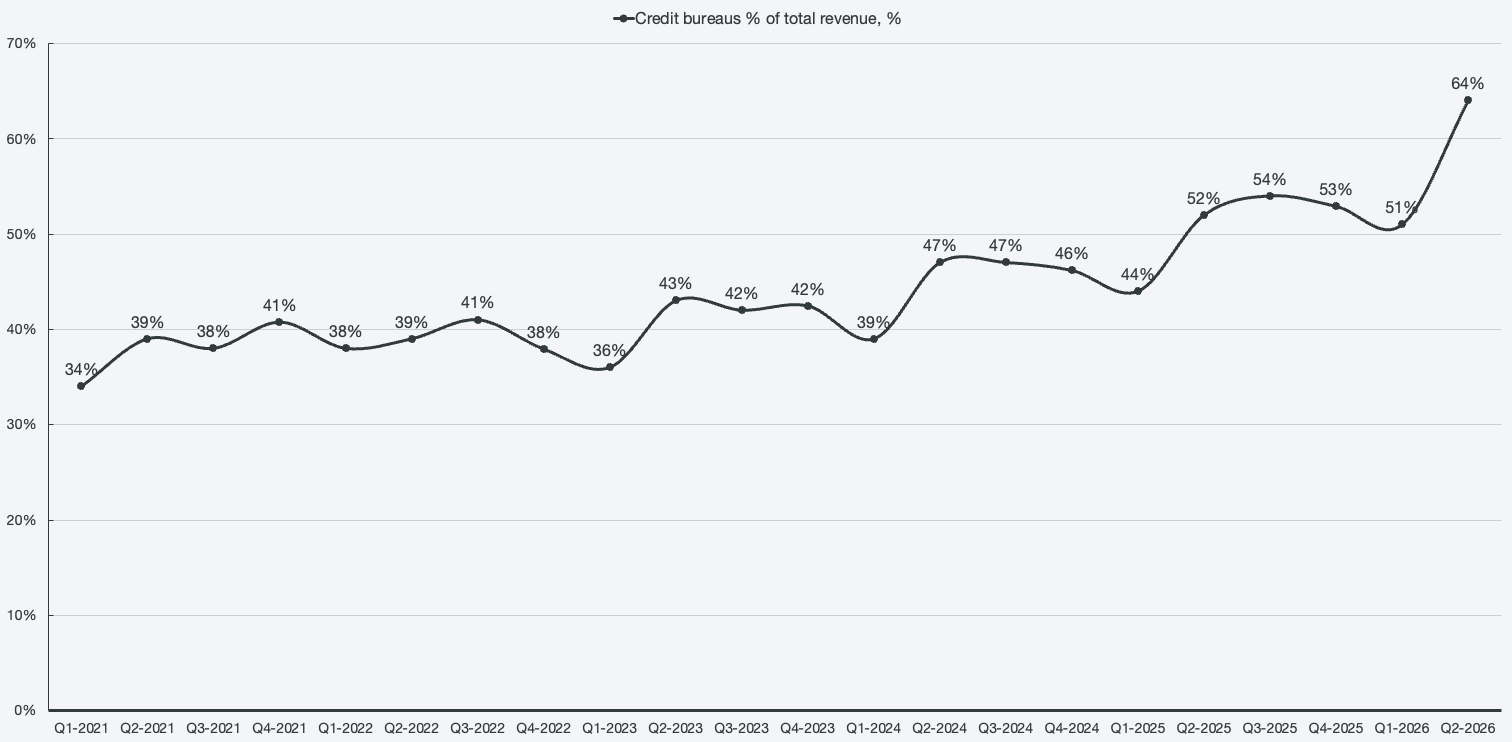

The direct license program is not widely available yet, as evidenced by the increase in bureaus as a % of overall revenue and from management commentary. That figure should drop once the program is live and adoption increases, and it will also impact the timing of score revenue. The performance-based model would have a trailing funding fee compared to straight up-front costs, which would hurt the score’s growth in the initial phases (very short term), but would catch up as the funding fees start being received.

Figure 3: Credit bureau revenue as a percentage of total revenue

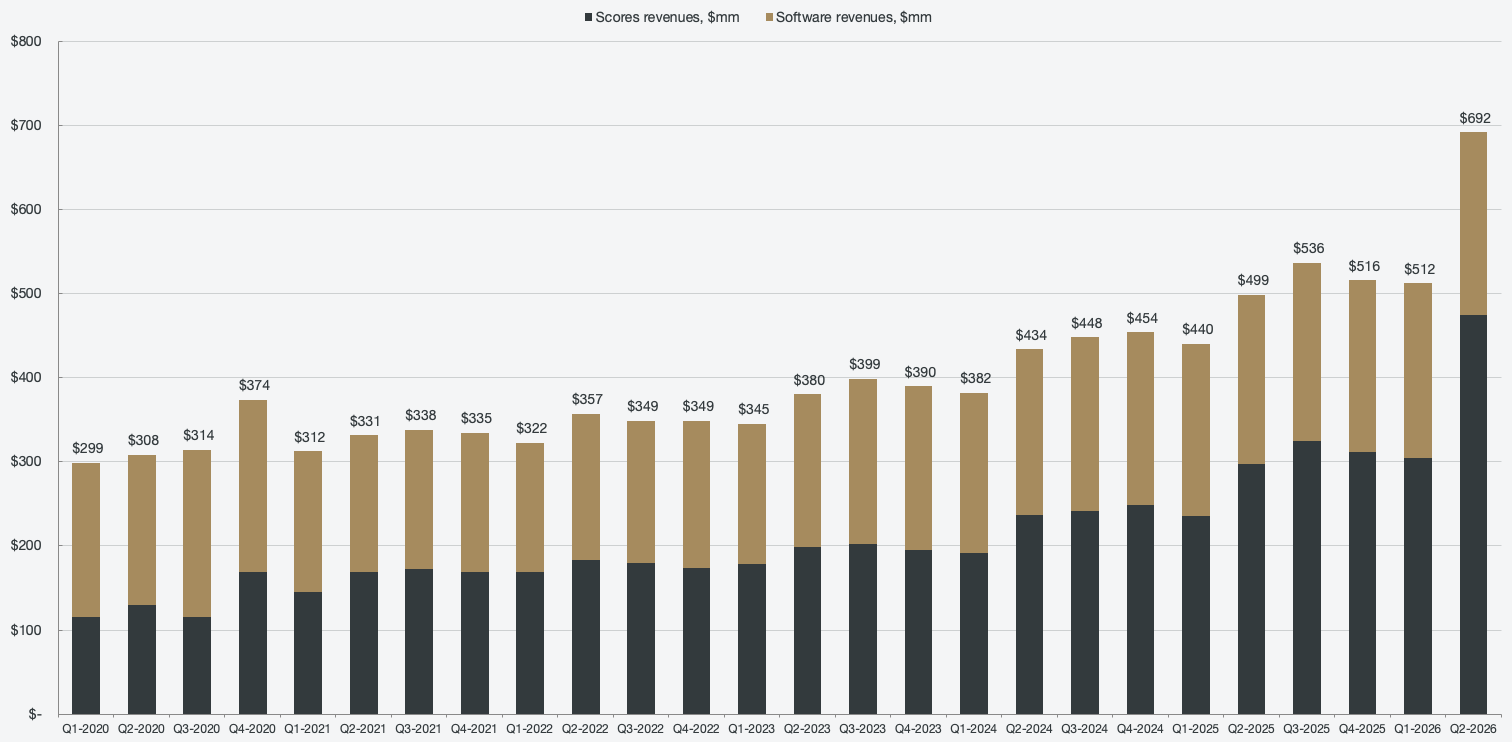

Scores are not the only exciting part of the business anymore, as software had a fantastic quarter as well. Scores grew 60% Y/Y in Q2, while software grew 7% Y/Y. Not many people would get excited at such a headline, but those are the same investors who don’t look deeper at the dynamic unfolding.

Figure 4: Segmented revenue

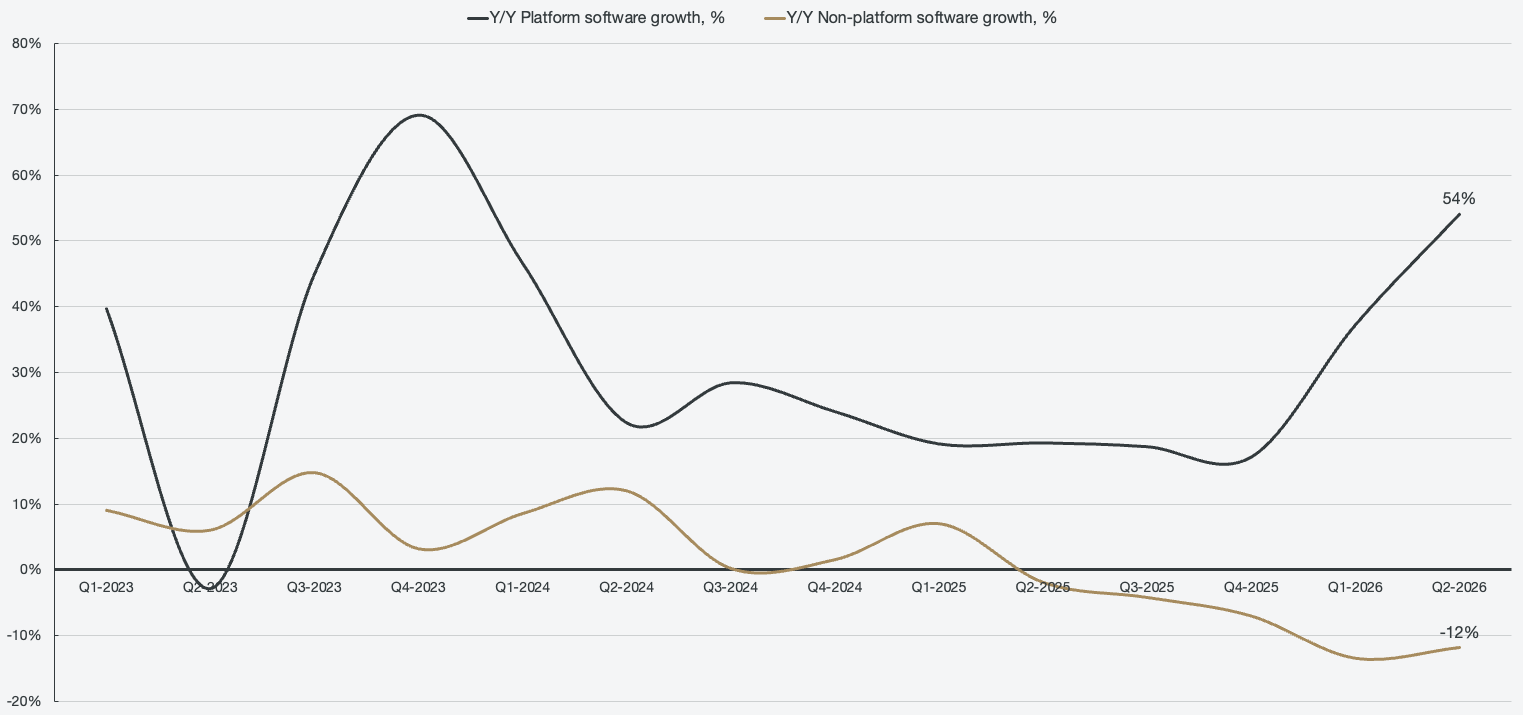

The dynamic that many investors unfamiliar with FICO may be missing is that a majority of FICO’s software revenue is legacy, and actively being phased out for a modern, cloud-based platform solution. The mix is quickly shifting towards the modern platform, a segment that is seeing impressive scalability (akin to Palantir’s). Platform revenue grew 54% Y/Y, which, while not 60% like scores, is completely organic revenue. It is important for FICO as a business to have organic growth, as scores are cyclical in nature. Non-platform is losing revenue each passing quarter, acting as a drag on overall software revenue. However, as the mix shifts, the software segment will increasingly become harder and harder to ignore.

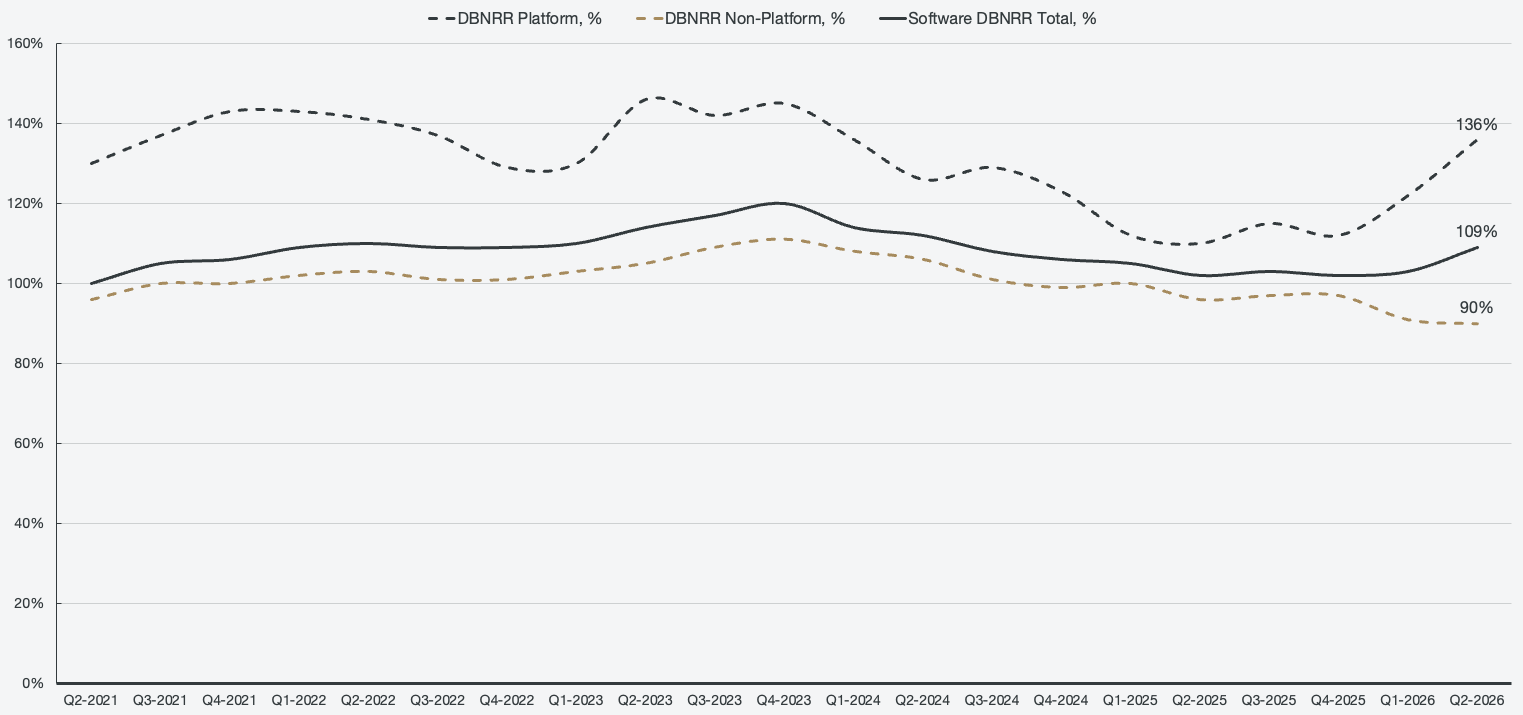

Figure 5: Segmented software growth

A year ago, platform revenue made up ~30% of overall software revenue, a figure that is now 44% as of Q2 2026, rapidly approaching that 50% majority line. What’s impressive is not the mere top-line growth figure, but the expansion among existing customers. The dollar-based net retention rate (DBNRR) increased to 36%, meaning that a majority of the growth in the segment is attributed to existing customers increasing their usage of the service. This is a dynamic similar to what Palantir is seeing, where it is important to simply land inside a business, to then showcase value, after which existing customers increase their spending. I am not expecting the segment to grow at the rapid pace Palantir is, but the increasing DBNRR is showcasing the value of the analytics and decision-making platform.

Figure 6: Segmented software dollar-based net retention rate