FICO: Regulators Are Failing To Disrupt The Best Business In The World

Equity research follow-up coverage, rating unchanged

Seemingly, no one wants to own FICO 0.00%↑ today, a stark contrast to a year ago, when everyone wanted to own FICO. The business has only gotten stronger, the pricing power has increased, and even with a large fantasy, it is difficult to imagine a business model more robust, unfair, and profitable than FICO’s.

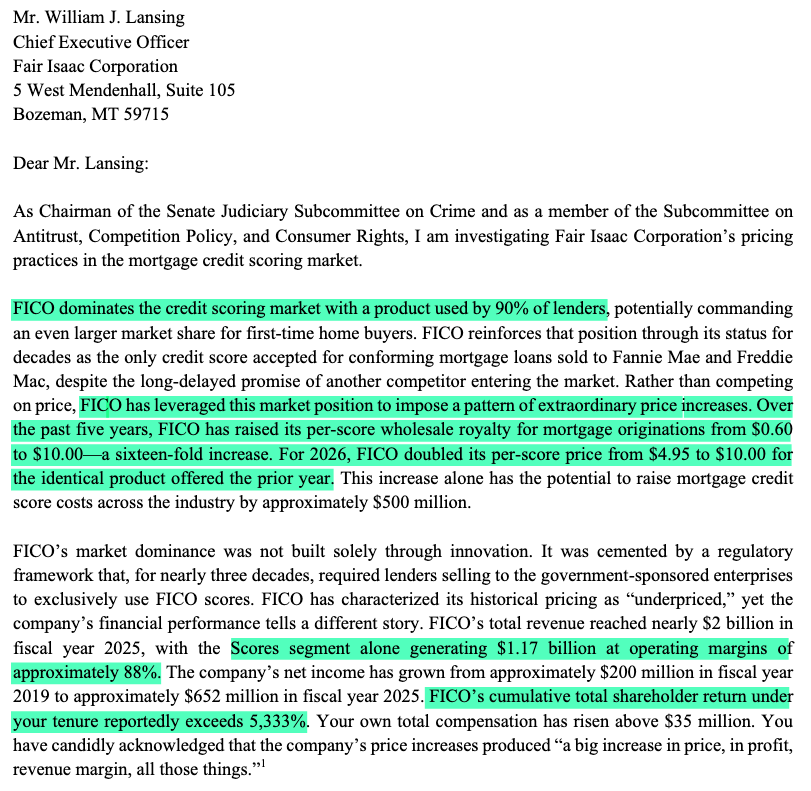

That is also the problem right now: FICO has too much pricing power in the eyes of regulators. I previously detailed FHFA Director Pulte’s comments about FICO being a core reason for the unsustainable housing market. This time, it is Senator Josh Hawley opening an investigation into FICO through a letter to FICO CEO William Lansing. The letter reads as a bullish investment case into the company, and cites many of the core reasons I am very excited about the company. However, much like with what Director Pulte brought forward, the concerns raised are misdirected.

Screenshot 1: Senator Hawley’s oversight letter to FICO, highlighted bullish remarks

Company profile

March 31, 2026 Follow-up coverage

Direction: Buy

Previous fair intrinsic value: $2081.66, as of January 12, 2026

Symbol: FICO, Exchange: NYSE

Sector: Technology, Industry: Software - Application

Theme: High quality

Fair intrinsic value: $2051.6 (95.33%), as of March 31, 2026

Market capitalization: $25 168 million

Pricing data: P/S 12.2x, P/E 38.3x

Previous coverage:

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

The best business model in the world continues to dominate

I typically start off my coverage of a company by breaking down the operations and the financials, but this time I want to deal with the elephant in the room first. Both Director Pulte and Senator Hawley both cite that FICO has raised the prices for its royalties per score pull significantly, and both cite concerns over how FICO’s pricing power may impact the consumer. Let’s break it down by looking at the number.

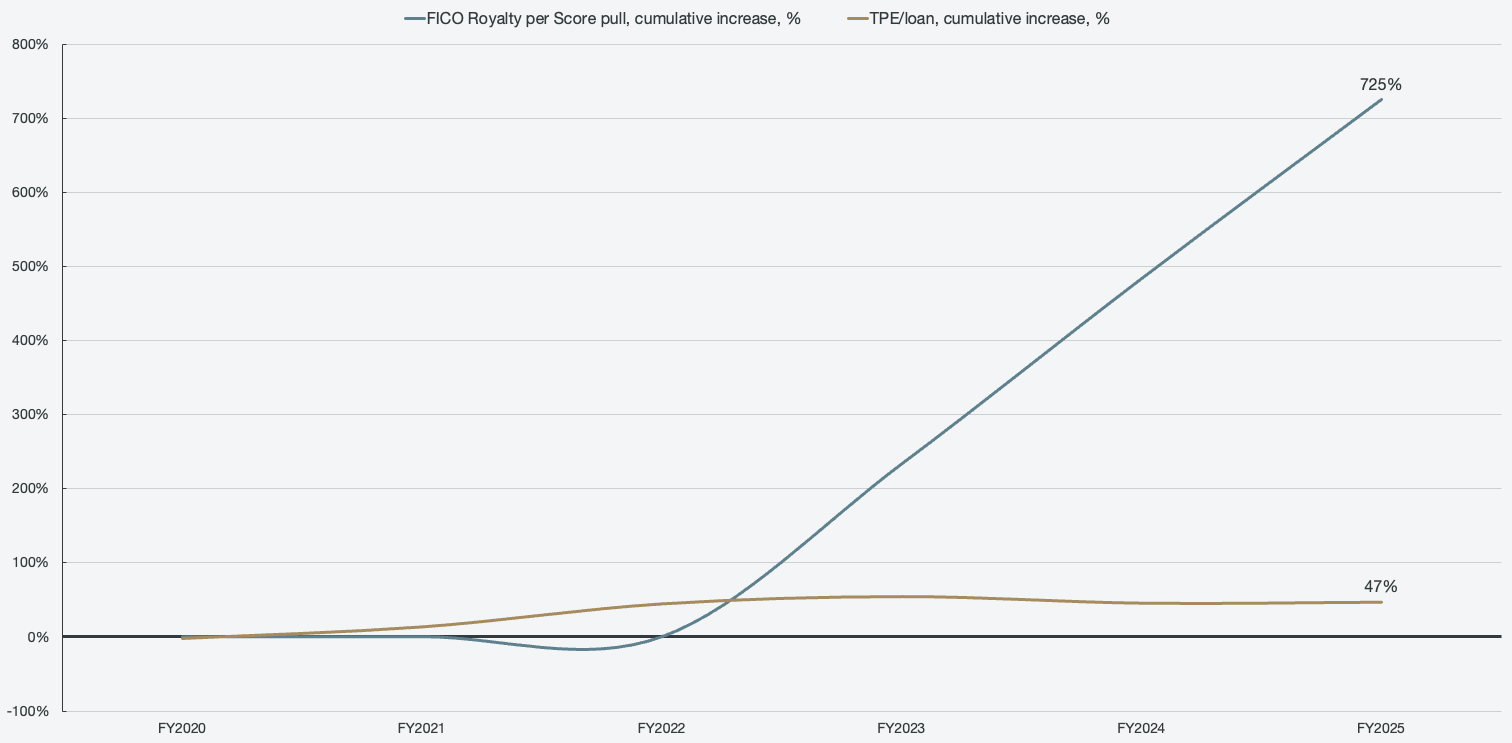

First, it’s important to understand that closing costs vary depending on the lender, the borrower, the state, and many other variables. However, what drives closing costs and the overall consumer impact is the cost of producing a loan. The cost to produce a loan must be recovered through a rate, a point of origination (direct up-front cost for the borrower), or a mix of both. For example, a $12,000 production expense could be charged to the borrower through $3,000 in closing fees, and the rest through a rate spread. Another lender might charge $0 in fees and price everything into the rate. In any case, the cost and more will be recouped for an issued loan. The Mortgage Bankers Association (MBA) tracks the production expense per loan, and we can use this as a relative measure to see if it correlates with the raise of FICO scores royalties to gauge the impact.

Figure 1: FICO Royalty per Score pull, total production expense per loan, cumulative increase %

We can see that the TPE/loan increased by 45% in 2022 compared to 2020, while FICO’s royalties remained at $0.60 per pull, a 0% increase in price. From 2022 to 2025, FICO increased the royalty per score pull by 725%, but the TPE/loan remains relatively static. By 2022, the TPE/loan had increased by 45% cumulatively from 2020, then 55%, 46%, and 47% for 2023, 2024, and 2025, respectively. The TPE/loan is not correlated to FICO’s price increases, and there is a good reason for that.

The FICO royalty makes up 0.04% of the total production expense per loan. In 2020, that was 0.01%, both equally non-meaningful to overall production expenses. However, Senator Hawley comments on this directly with the following:

FICO has suggested that its royalty constitutes a negligible share of overall closing costs. But the relevant question is not whether the charge is small relative to other fees. Instead, we investigate whether the charge is justified by competitive market forces or is instead an exercise of monopoly pricing power.

Senator Hawley’s oversight letter to FICO, March 23, 2026

If the concern is indeed about the average borrower feeling the pain from FICO’s price increases, and in turn, is hurting the mortgage market, then it is most definitely relevant to look at whether FICO’s royalties constitute a meaningful share of overall closing costs or not. It clearly does not, given the objective data, and the probe should be ended with that. However, I think Senator Hawley is correct to ask the question about FICO exercising monopolistic pricing power. We can dig into that data as well.

Is FICO right to raise its royalties per score pull?

FICO has characterized its historical pricing as “underpriced,”

Senator Hawley’s oversight letter to FICO, March 23, 2026

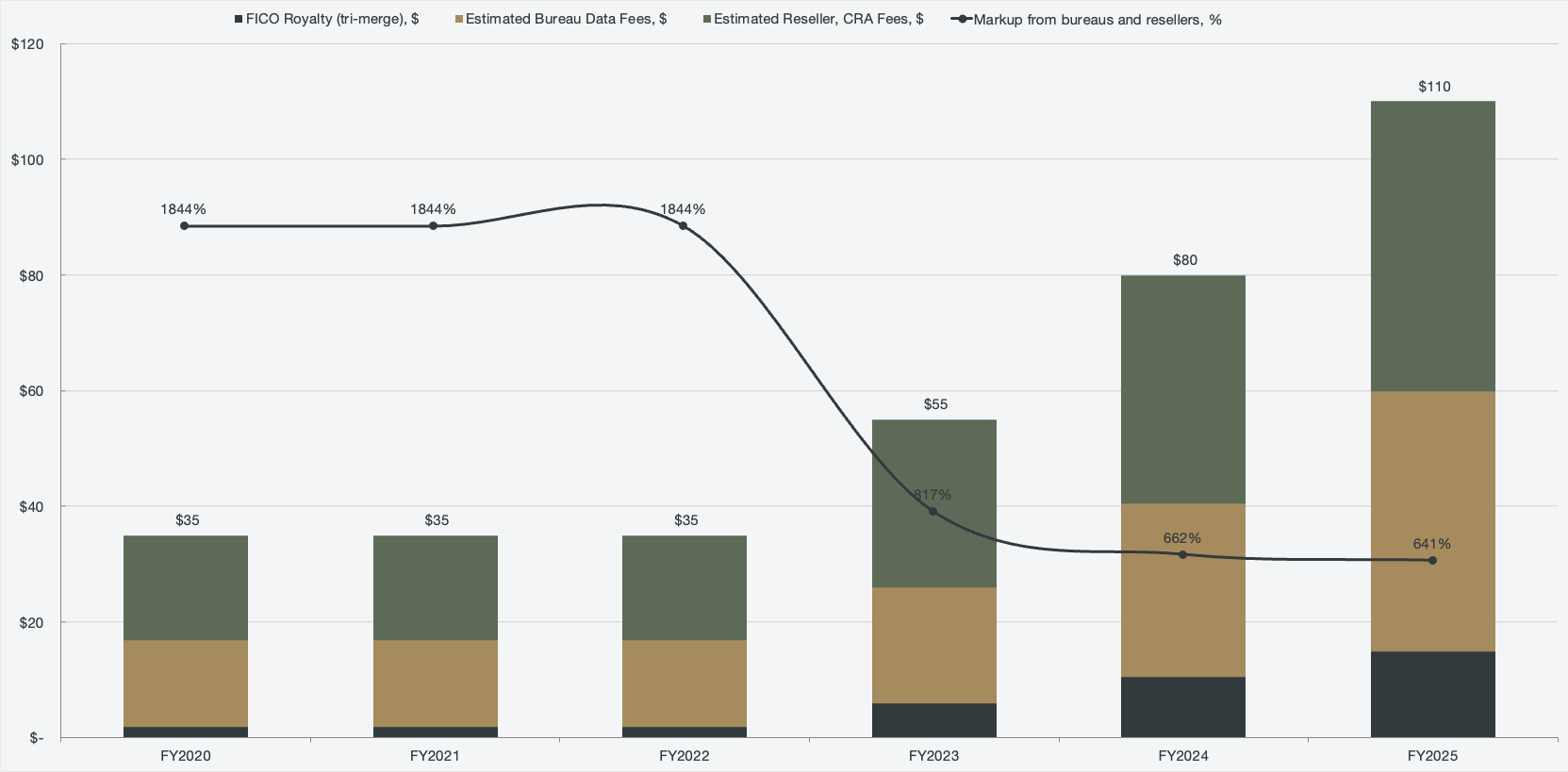

I believe FICO is justified in its price increases, and it has definitely been underpriced historically. In fact, I still think it is underpriced, and they should increase the price even further. Why do I say that? Because the markup from bureaus and resellers over the past five years has been as high as 1844%. While FICO only charged $0.60 per score pull, or $1.80 on a tri-merge basis, the total estimated cost per pull was $35. That implies a full 1844% markup from bureaus and resellers. The mathematical model of the credit report is the integral and centerpiece, so why should it be a mere 5% of the overall cost per pull? The line item presented to banks and borrowers is a lump sum with bureau data fees and CRA fees, not allowing for transparency of who is making it out like a bandit.

Since 2020, FICO has increased its cost per score pull by 725%; however, its share of the estimated total cost per pull only increased from 5% to 14%. FICO, the core and integral part of a FICO score, is still by far the minority in terms of overall costs for a score pull.

Figure 2: Estimated costs per credit score pull, markup from bureaus and resellers

FICO launched the mortgage direct licensing program to cut out a lot of the markups associated with pulling a FICO credit score, and in turn, also provide a lot more transparency. Senator Hawley claims that FICO doubled its prices from 2025 to 2026, from ~$5 to $10, while not providing a meaningfully better product. While that is partially true, the $10 per score is, on average, the same price that resellers paid for FICO scores in 2025, which gives a clear picture of how muddied the bundled line item was.

The other pricing option for FICO scores, by going directly to lenders through resellers, is a performance model. In the performance model, the price per score remains the same at $4.95, with a $33 funding fee on closed loans. This directly combats the statement made by Senator Hawley in his letter that FICO is actively hurting first-time borrowers who typically have their credit scores pulled multiple times. This is effectively a 50% reduction in average per-score fees compared to what resellers paid for FICO scores in 2025.

These price increases are most damaging to the Americans who can least afford them. First-time homebuyers bear a disproportionate burden of the cost. They typically undergo multiple credit checks during the home-buying process—at prequalification, at formal application, and often again before closing—and frequently pay for credit pulls on applications that do not result in a funded loan.

Senator Hawley’s oversight letter to FICO, March 23, 2026

I don’t see how FICO should be blamed for various types of lenders having to undergo multiple credit score pulls. If Senator Hawley wants to combat this, FICO, which only provides the mathematical scoring models, has no impact on the practice.

One final point that Senator Hawley raises is that FICO’s dominance is the result of a regulatory framework that required lenders selling to GSEs to exclusively use FICO scores for over three decades.

FICO’s market dominance was not built solely through innovation. It was cemented by a regulatory framework that, for nearly three decades, required lenders selling to the government-sponsored enterprises to exclusively use FICO scores.

Senator Hawley’s oversight letter to FICO, March 23, 2026

The framing Senator Hawley puts forward overstates the role of regulation. There was no federal statute, FHFA rule, or HUD regulation that mandated GSEs to adopt or exclusively use FICO scores. The GSEs themselves chose to incorporate FICO into their underwriting and delivery guidelines in 1995 because it was already widely used by lenders and seen as a gold standard. GSE guidelines are contractual and business requirements that lenders follow to sell loans, not regulations imposed by a government agency. In fact, in 2018, Congress passed the 2018 Credit Score Competition Act specifically to require FHFA to create a validation process for alternative credit score models. FICO was the standard through GSE policy, not through a binding regulatory mandate.

In summary, FICO score royalties have no impact on the production expense for loans. FICO exercising its pricing power does not hurt the end consumer in a meaningful way, as its overall royalty constitutes a negligible part of overall closing costs, even after a 725% increase. A FICO royalty only constitutes 0.04% on total production expenses in 2025, and of an estimated cost per pull on a tri-merge basis, the markup from bureaus and resellers is still 641% (down from 1844% pre-increases). These investigations into FICO scores will not help the mortgage market or borrowers. FICO is an easy target to go after, as it creates headlines with the pricing increases. However, the math behind the increases justifies them and does not hurt the overall mortgage market, and as such, I don’t see a scenario where FICO is meaningfully hurt over these probes.

I see FICO retaining complete monopolistic dominance as it is too deeply embedded in the finance ecosystem. For a more detailed breakdown on FICO’s monopoly, see my previous FICO coverage.