Palantir Technologies: Alex Karp's New Target Changes Everything!

Equity research report

Love him or hate him, but few voices make all swaths of both the corporate and investment world pay attention when they speak the way Alex Karp does. Over the years, what have seemed like ridiculous claims have often turned out as Karp prophesied. On July 1st on CNBC, discussing Palantir’s new deal with Nvidia, Alex Karp disclosed a financial target so ambitious that even Palantir bulls are having a hard time wrapping their heads around it.

However, history has proven Karp’s ambitious claims to come true, even if they seemed extremely unlikely at the time. I believe his most recent outrageous claim will prove true, as well.

Company profile

Previous fair intrinsic value: $268.5, as of May 9, 2026

Symbol: PLTR, Exchange: NASDAQ

Sector: Technology, Industry: Software - Infrastructure

Theme: AI Software

Fair intrinsic value: $340.77 (163.55%), as of July 5, 2026

Market capitalization: $332 420 million

Pricing data: P/S 64x, P/E 145x

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

The history of Alex Karp’s ambitious claims

I have made the latest Palantir coverage completely free to read by removing the paywall. I highly recommend reading it for a grasp on where Palantir is in its narrative.

It also serves as a free preview of the level of research I publish here on my Substack. You can find the research coverage below:

This article is not a full research piece.

It targets specifically the comments made by Alex Karp during his CNBC interview.

Alex Karp is not shy about sharing his thoughts, be it geopolitical views or forecasts of where he sees his own business over the coming years. When Palantir went public through a direct public offering (DPO) in September of 2020, one of the key financial targets was a compounded annual growth rate (CAGR) of 30% through 2025.

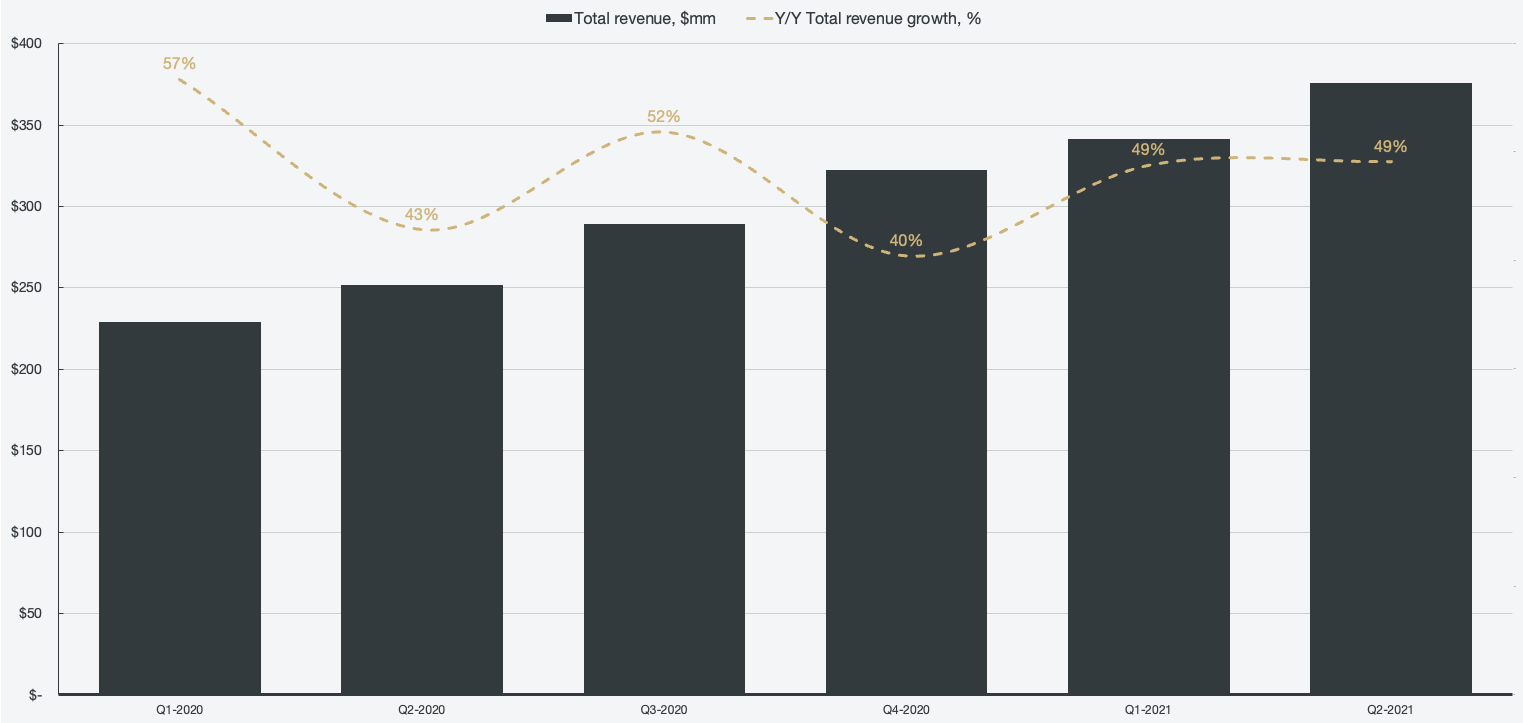

Looking at the financial performance surrounding the DPO, not only did 30% CAGR seem probable, but it even seemed understated. From Q1 of 2020 through Q2 of 2021, Y/Y revenue growth averaged 48%.

Figure 1: Total revenue and revenue growth, Q1-2020 through Q2-2021

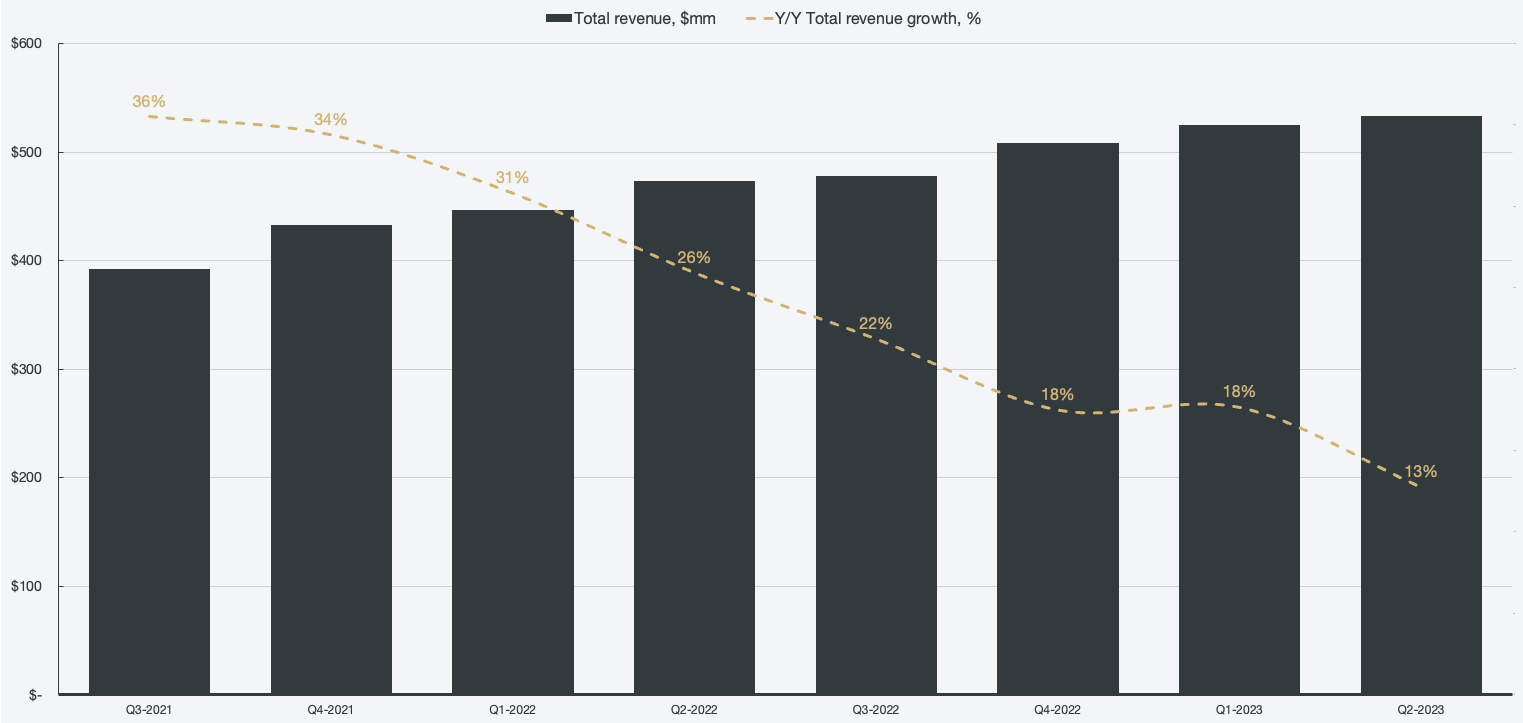

However, what followed was a rapid deterioration of growth rates, with an absolute low of 12.7% Y/Y revenue growth rate in Q2 of 2023. During the decline, Palantir quietly stopped reiterating its 30% CAGR target, raising the eyebrows of investors.

Figure 2: Total revenue and revenue growth, Q3-2021 through Q2-2023

During those times, Palantir still had representation of various financial analysts, and Sanjit Singh of Morgan Stanley addressed the elephant in the room during the Q2 2022 earnings call. That was the first quarter that Palantir dropped below 30% Y/Y revenue growth since going public.

Alex, I wanted to get your view, not just so much on the quarter, but sort of the longer-term framework. I noticed that you guys didn’t reiterate the 30% outlook. In some sense, that makes sense because deals are uncertain. I thought it was interesting that you guys took back the 30%.

Sanjith Singh, U.S. Software Analyst at Morgan Stanley

Palantir Technologies, Q2 2022 Earnings Conference Call

Alex Karp’s response was sharp, leaving no room for speculation:

I am driving the company to get to $4.5 billion in 2025.

Alex Karp, Chief Executive Officer

Palantir Technologies, Q2 2022 Earnings Conference Call

$4.5 billion in 2025 would be a 33% CAGR from FY 2020, the year Palantir went public. Not only reiterating the 30% CAGR goal, but overshooting it. At the time, for each quarter that followed that quote over the next year, the target seemed more and more unlikely, and the stock quote reacted accordingly, hitting single digits and trading there for close to a year.

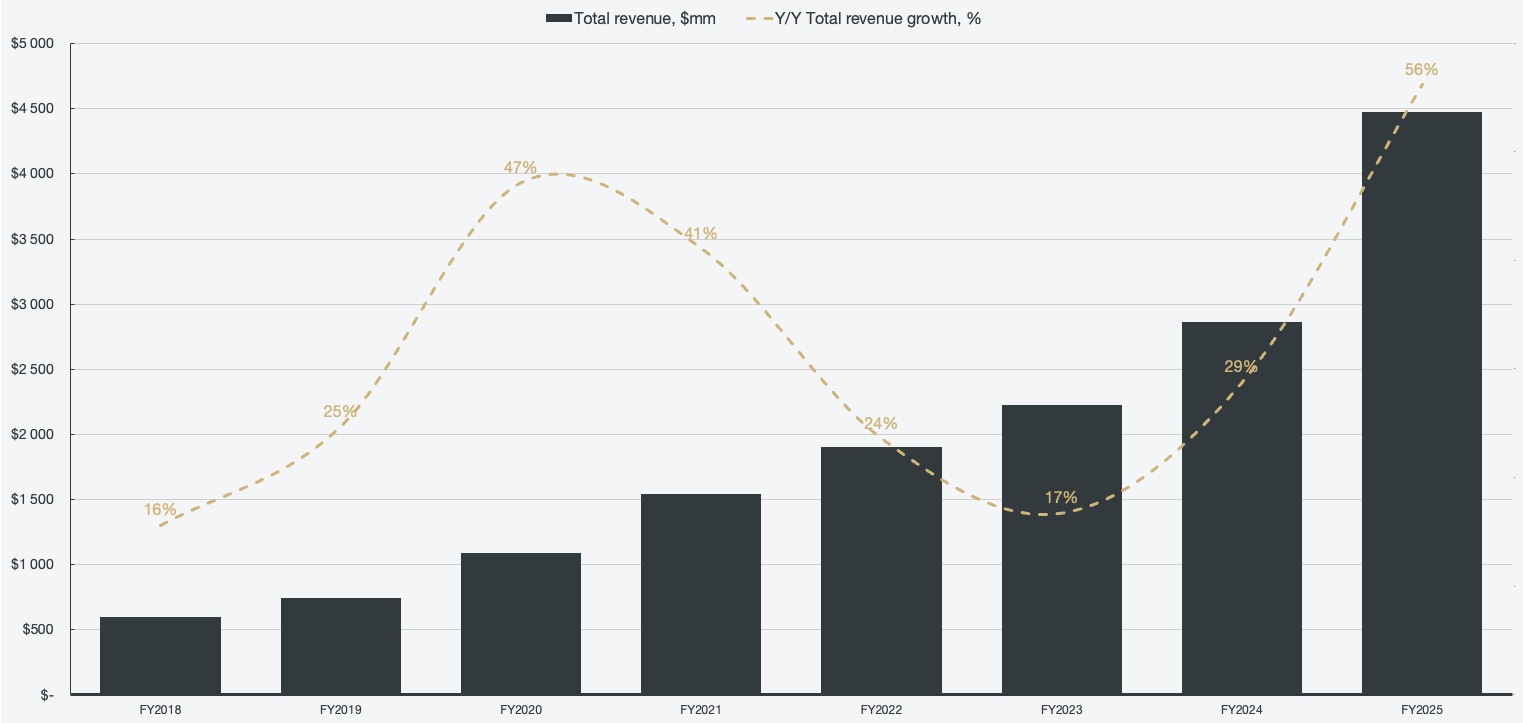

However, in Q2 of 2023, at the absolute rock bottom of Y/Y growth, Palantir launched AIP. Since then, for three years to date, every single quarter that followed the bottom of 12.7% in Q2 of 2023 has been higher than the previous quarter. A revenue acceleration out of this world, and one that most investors would find absolutely absurd as a claim if you told them that at the time of decelerating growth. Most did not believe Karp’s reiteration of the 30% CAGR, and the following quarters proved it to be more and more unlikely.

2025 came around, and sure enough, Palantir hit Alex Karp’s forecast of $4.5 billion in revenue, however unlikely it sounded at the time. In Q2 of 2022, when Alex Karp replied to the Morgan Stanley analyst, $4.5 billion would require revenues to 2.5x in 2.5 years, and it did.

Figure 3: Total revenue and revenue growth

The seemingly impossible lofty goals

That brings us to today and the new claims made by Alex Karp. History serves as the witness to the credibility of the ambitious CEO’s claims, and if nothing else, that they should not be disregarded easily.

Before we look at the most outrageous goals of them all, let’s rewind to a few months ago, when Alex Karp set a forecast for the company that changed intrinsic value massively.

After the amazing year of 2025, my fair intrinsic value for the business was $205. Not only was revenue growth accelerating for each passing quarter, hitting 70% Y/Y in Q4 of 2025, but margins were simultaneously exploding. Palantir has immense operating leverage as a capital-light business, unparalleled scalability, and sticky revenue. However, in a single quarter, that fair intrinsic value estimate changed to $270 in a single quarter due to a specific quote during the Q1 2026 earnings call:

We are at our limit doing 100% this year, which I am going to drive the company to, and maybe we can do 100% next year in the U.S.

Alex Karp, Chief Executive Officer

Palantir Technologies, Q1 2026 Earnings Conference Call

U.S. revenue is ~80% of total revenue, and seeing two consecutive years of at least 100% growth has massive implications for the business. The fair value estimate of $270 may seem like a delusion at face value, but when one extrapolates the characteristics of how Palantir grows its revenues and combines it with the expanding margin profile that seemingly has no cap, that fair value estimate no longer seems as crazy.

Now, after Alex Karp’s CNBC interview a few days ago, my fair value estimate for Palantir is $341, an unfathomable number. However, the claim by Alex Karp is equally unfathomable, and once one understands what it implies, $341 no longer seems as a crazy fair intrinsic value estimate.

We have more business than we can supply.

If you just look at our financials, you can see, 2 years out, $15-$18 billion in free cash flow.

Alex Karp, Chief Executive Officer

CNBC interview, July 1st 2026

A bomb was dropped, and due to the nature of the intense ~18-minute interview, this quote seemingly passed by without much attention. However, $15 billion in free cash flow would mean a 5x in 2.75 years. A 2.5x in revenues in 2.5 years was impressive, but a 5x in free cash flow, when adjusted FCF margins are already at 57%, the implications are massive. If FCF margins were low, a 5x would be quite achievable, but as it stands, the implications of a 5x are titanic for the business, as it implies a massive increase in revenue. And that is just at the lower end of the target, $15 billion.

Unlevered free cash flow, commonly used in valuation models, which also accounts for reinvestment needs, is slightly lower than adjusted free cash flow. Karp’s target likely refers to adjusted free cash flow, which is adjusted for payroll taxes associated with stock-based compensation.

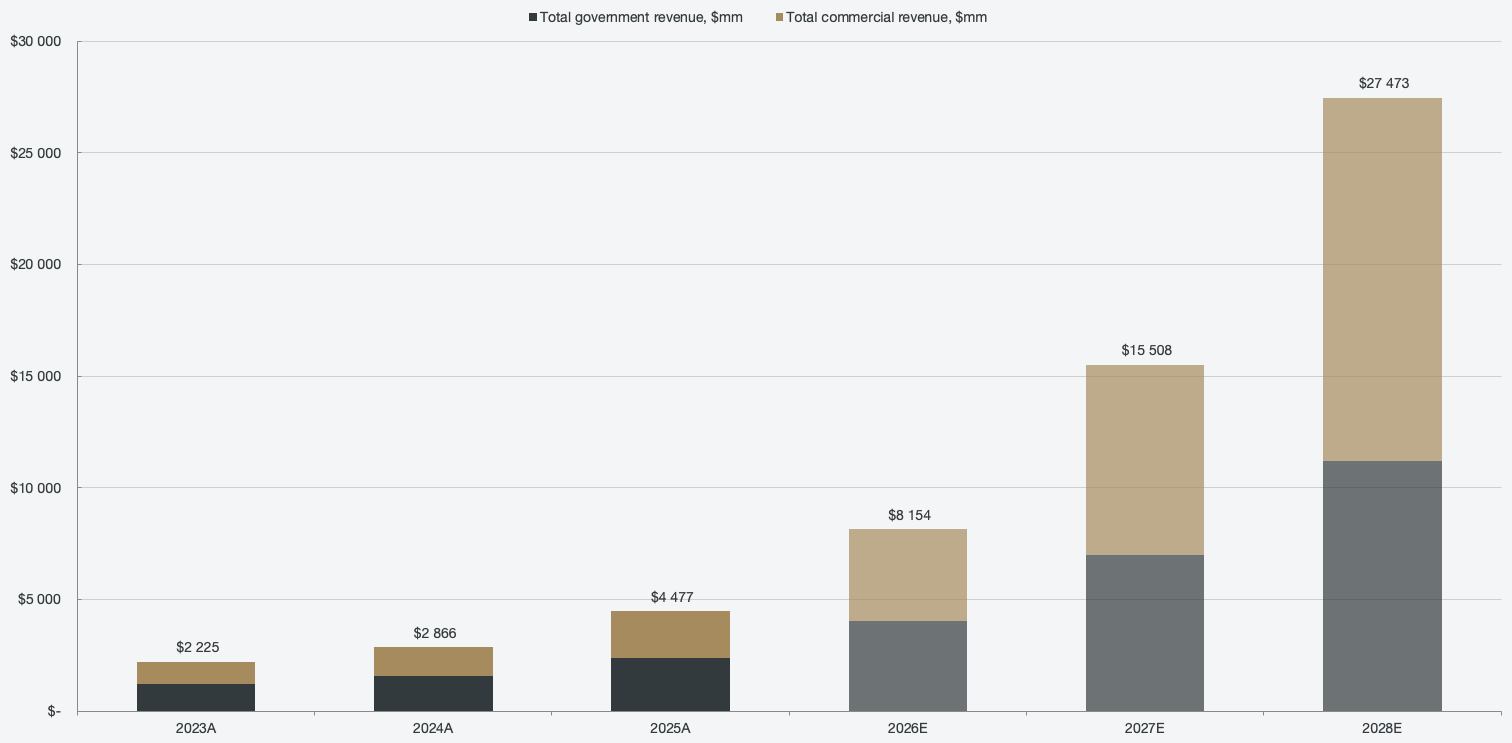

When I model my expectations for the business while keeping $15 billion in adjusted FCF in mind, the inputs seem fairytale-like. While I have allowed for reasonably probable margin expansion as well, the CAGR rates for the business segments eclipse my wildest imaginations for the company:

U.S. Government CAGR: 80%

Non-U.S. Government CAGR: 54%

Total Government CAGR: 75%U.S. Commercial CAGR: 136%

Non-U.S. Commercial CAGR: 12%

Total Commercial CAGR: 112%Total Revenue CAGR: 93%

Figure 4: Historical segmented revenue and revenue forecast

When these figures are then extrapolated over 10 years, while keeping the sheer scalability and sustainable nature of the growth in mind, $341 fair intrinsic value does not seem that absurd anymore.

Our free cash flow this quarter is larger than our revenue a year ago in the same quarter. Think about that. Same company, same people, extended products. It’s all being extended.

Alex Karp, Chief Executive Officer

Palantir Technologies, Q1 2026 Earnings Conference Call