PayPal Holdings: Days of "PainPal" are soon history

Equity research follow-up coverage, rating unchanged

I seldomly comment on a stock quote; instead, I focus almost entirely on the business. I typically only tie in the current stock quote in reference to fair intrinsic value, but today I will make an exception. PayPal PYPL 0.00%↑ has the moniker of being “PainPal” and has been regarded as dead money for quite some time.

Figure 1: Historical stock quote, weekly

Over the past 3 years, PayPal stock has a return of -9.64%, while the S&P 500 SPY 0.00%↑ is up 75%. During this time, there have definitely been concerns that may have warranted some skepticism. However, the current quote does imply some pretty severe scenarios for PayPal, which are not materializing. In a reverse DCF scenario, PayPal would have to shrink -5% CAGR over the next 10 years in order for intrinsic value to be where today’s quote is.

As a reminder, PayPal is growing and is doing so with a lot of exciting products at the forefront of innovation in the payments space.

Company profile

November 2, 2025 Follow-up coverage

Direction: Buy

Previous fair intrinsic value: $136.60, as of August 3, 2025

Symbol: PYPL, Exchange: NASDAQ

Sector: Credit Services, Industry: Financials

Theme: Deep value

Fair intrinsic value: $145.90 (+111%), as of November 2, 2025

Market capitalization: $67 677 million

Pricing data: P/S 2x, P/E 14x

Previous coverage:

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

The dinosaur argument no longer applies

As discussed in my previous coverage, PayPal is largely seen as a dinosaur by many investors, but the future plans for the business have been quite grand for quite some time. This is starting to manifest itself with some grand partnerships that PayPal has entered into in recent times, including:

OpenAI

Integrates PayPal’s wallet into ChatGPT, enabling users to make purchases using the chat platform.

PayPal facilitates the checkout process for consumers, as well as enables its merchant network to sell through ChatGPT.

Mastercard

Integrating the Mastercard Agent Pay platform into PayPal’s wallet, enabling AI-agent-driven transactions.

An additional partnership around “One Credential,” which is a joint effort to give consumers more control while checking out using single credentials.

Google

A multi-year partnership to integrate PayPal’s checkout, payouts, and other services into Google’s products.

Also allows PayPal to leverage Google’s AI capabilities for an improved payment and shopping experience.

In addition to those major partnerships, PayPal has entered into many other partnerships for enhancing various parts of its business, including Perplexity AI.

In short, this company is not standing still and is seriously starting to leverage its data and network edge in the payment space. PayPal is pushing the whole next generation of payment processing and checkouts, but due to its massive scale, it is not quite as nimble as some smaller competitors. The dinosaur argument will find itself shelved among even the most bearish investors in the coming periods.

The transformation can be observed in the segmented financials. Currently, the return of growth in the OVAS (other value-added services) segment is telling the narrative.

Figure 2: Other value-added services revenues

PayPal has identified the future of digital finance and has positioned itself to become the premier commerce orchestrator. Building a layer to power the next generation of shopping experiences utilizing chatbots and AI agents is the correct decision in my view, but we will still need some time to see the effects at scale.

Growth in key areas

The quarter itself was not groundbreaking or overly impressive, but since the quote implies negative growth, an actual acceleration is proving the market wrong. This is the third quarter in a row where PayPal has accelerated Y/Y total revenues.

Figure 3: Segmented revenues

However, the current story is not so much about the top-line growth but rather the mix shift that is happening across the business. The digital payments space in general is growing, but due to competition, the overall take rates are decreasing for all participants. What matters for PayPal is finding ways to increase transaction margins, and in order to do so, they have to scale and monetize the more attractive parts of their transaction business.

The overall TPV mix is still favoring the lower-margin PSP segment and will likely continue to do so since it makes up a majority of TPV. Even though PSP is growing at a slower pace, it will take some time for a meaningful mix shift.

Figure 4: Segmented total payment volume

The associated take rates are still decreasing, both on a transaction basis as well as on a total basis. However, as PayPal shifts the narrative within its business, this is already accounted for in my intrinsic valuation model.

Figure 5: Transaction and total take rates

Over time, I see PayPal being able to increase its take rate, despite the highly competitive digital payments market. This is due to the fundamental advantage merchants can gain by connecting to PayPal’s network and vault. The Vault stores more than 25% of all issued cards in circulation and has a total of ~7 billion vaulted financial instruments. By leveraging this, PayPal is able to tailor experiences for customers in a way that is unparalleled in the digital payments space. I expect that the Vault’s value, and merchants’ willingness to pay for the value, will manifest more meaningfully as PayPal ads grow larger.

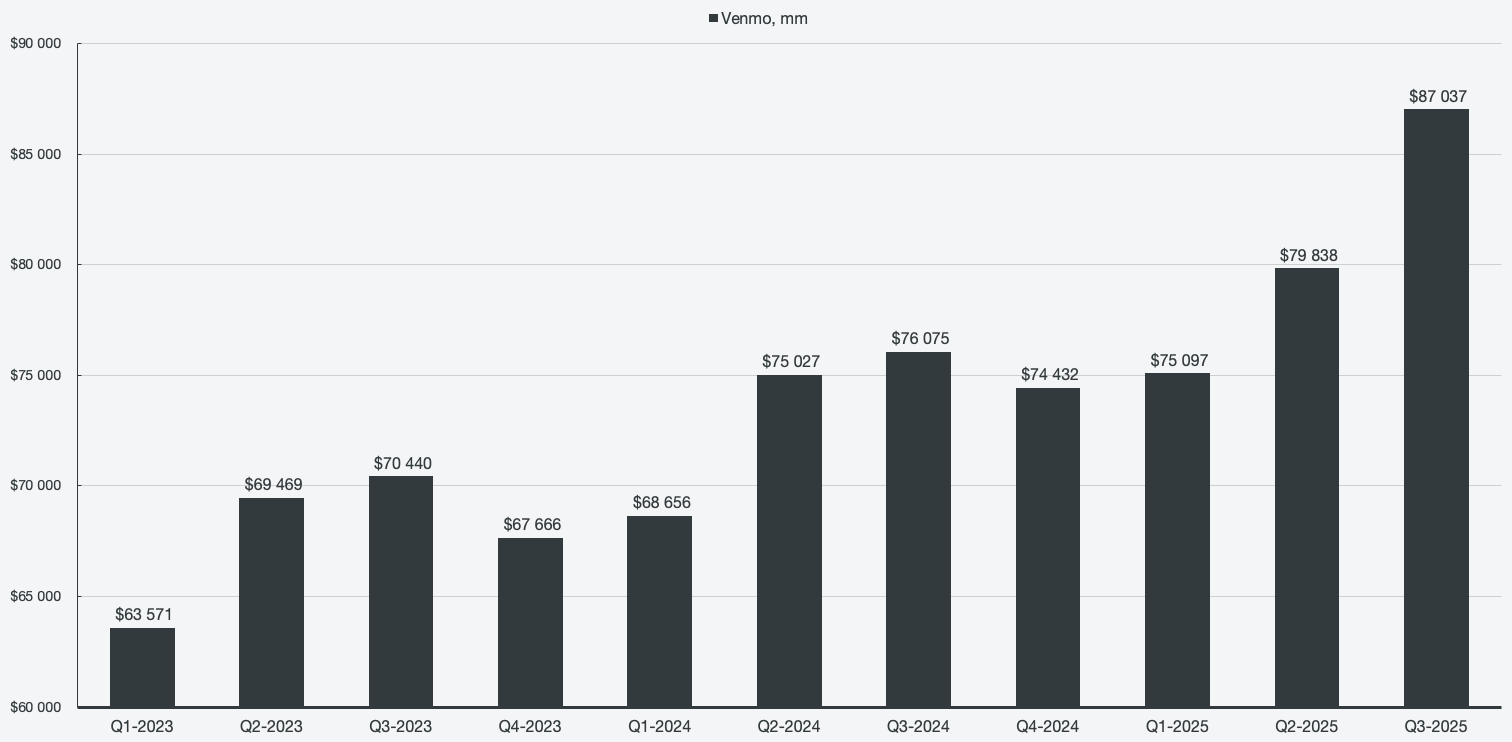

One segment that has gotten a lot of attention from management since Alex Chriss stepped in as CEO is Venmo. PayPal has two key growth drivers: online as well as in-store branded checkout. The core idea is to enable customers to be empowered by PayPal in-store, online, and during agentic shopping experiences. To do so, they have to provide a superior checkout experience compared to other market competitors. Venmo was previously a poorly monetized segment without much growth, but since the introduction of Venmo offline using debit cards, customers’ online activities have increased as well. As a result, so does profitability from the segment.

Venmo is no longer a simple payment app; it’s being built into a next-generation money platform. Venmo is approaching 100 million total active accounts and is growing in mid-single digits. Venmo is quickly cementing itself as the top P2P platform; now they need to grow the whole ecosystem. We can already observe Venmo payment integrations growing across more services with Pay with Venmo, whose monthly active accounts grew ~25% in Q3 2025. Similarly, payment volumes grew 14.4% Y/Y.

Figure 6: Venmo total payment volume

The scalability available within Venmo is quite massive. Out of the ~100 million total active accounts, only about 5–10% actually use the debit card or Pay with Venmo. PayPal is just starting to monetize Venmo, and it’s expected to be a high-margin transaction segment.

[…] Venmo is on pace to generate $1.7 billion in revenue this year, excluding interest income. That’s up more than 20% and a 10-point acceleration from two years ago. Under the surface, we are also changing our revenue mix and growing in high-margin areas. Over the past two years, we’ve doubled Pay with Venmo and Venmo debit card revenue.

Today, Venmo’s average revenue per monthly active account sits at just over $25. While over 90% of Venmo’s users engage with P2P, only 5% to 10% are using our debit card or Pay with Venmo, and less than 5% have set up recurring funds in. For the subset of accounts engaged across P2P, debit and Pay with Venmo, which is still small today, ARPA is about 4x higher.

- CEO Alex Chriss,

PayPal, Q3 2025 Earnings Conference Call

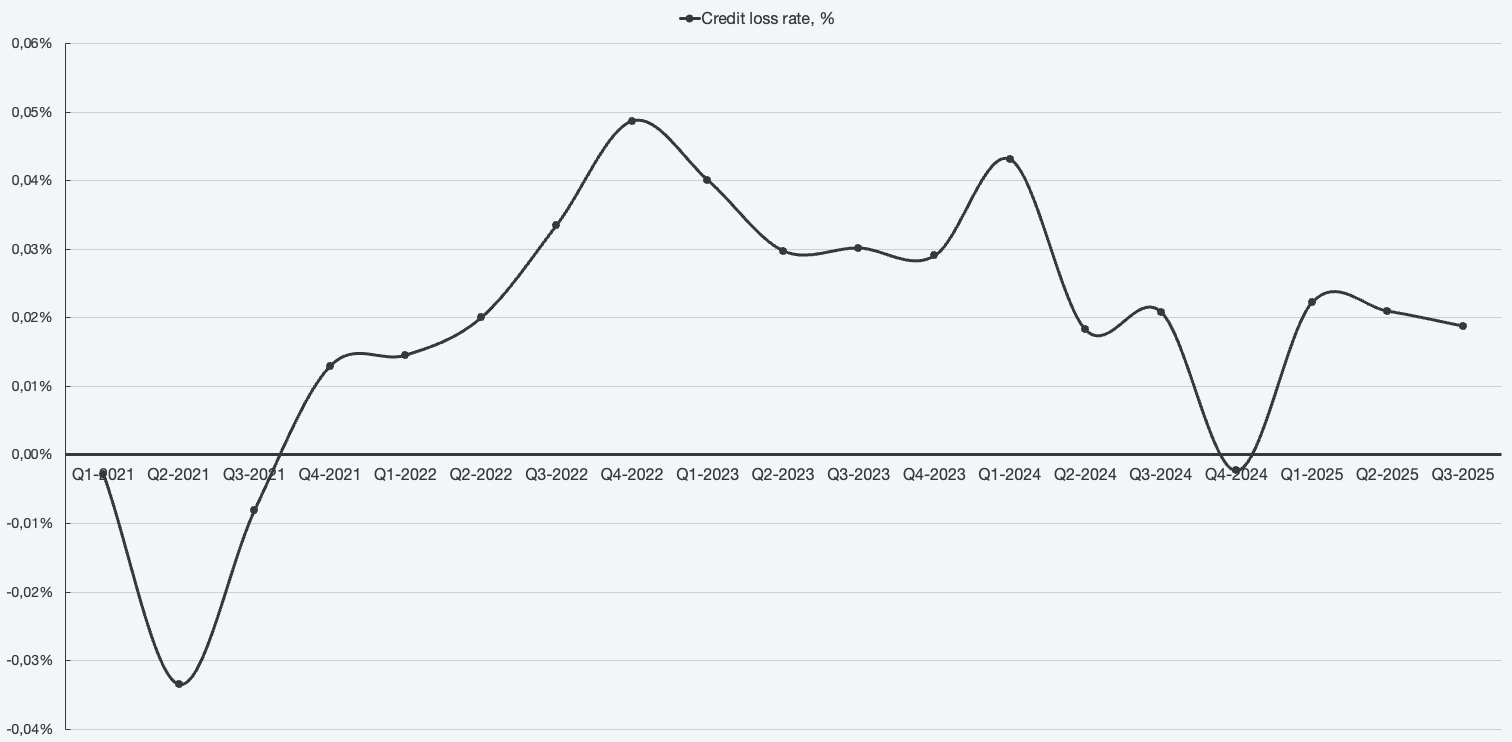

Another growth lever is growing exceptionally fast in the BNPL segment, which grew 20% Q/Q. BNPL in particular is a product particularly attractive to younger demographics, not unlike Venmo. BNPL is expected to do $40 billion of TPV in 2025, and it is much about offering every kind of experience that customers want; there should be no excuse not to use PayPal due to preference of payment method. BNPL as a business is significantly more risky, but charge-offs and credit losses are not increasing meaningfully to signal that PayPal has taken on too much risk as a result of growing BNPL.

Figure 7: Credit loss rates