PayPal Holdings: The Value Trap Unfolded

Equity research follow-up coverage, rating downgrade

PayPal has misled investors with grandiose promises of being at the frontier of adapting to the next era of finance, financial timelines, and product launch scale. I see it as a large wasted opportunity, as PayPal truly had all the tools required to do all of the aforementioned feats, and retain its dominance in the digital payments space.

The stock has cratered from an already extremely cheap quote, the CEO has been fired, and uncertainty is the highest it has ever been. However, the stock is not the only thing that has cratered; so has the intrinsic value. Is there any reason remaining to own PYPL 0.00%↑ stock as of right now?

Company profile

March 12, 2026, Follow-up coverage

Direction: Hold

Previous fair intrinsic value: $145.90, as of November 2, 2025

Symbol: PYPL, Exchange: NASDAQ

Sector: Financials, Industry: Credit Services

Theme: Deep value

Fair intrinsic value: $68.73 (+52.66%), as of March 12, 2025

Market capitalization: $43 219 million

Pricing data: P/S 1.30x, P/E 8.26x

Previous coverage:

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

Uncertainty gets punished

On a surface level, PayPal was truly set up to capitalize on the agentic wave that we are seeing across the AI industry. They have partnerships with OpenAI, Google, Mastercard, Perplexity, and just about every other major player in the space in order to enable user purchases within AI platforms. In addition, they have the single greatest source of actual purchase data relating to e-commerce, so why has the ads business not been launched and been a success yet? The questions relating to execution have been piling on, and investors’ patience has seemingly run out.

In my coverage of PayPal, I have deemed it a deep value opportunity, since the stock quote implied that the stock would not only stop growing, but actually decline. Where the stock quote is currently trading, it implies about a -7% CAGR at 13% FCFF margins over the next 10 years. Such a narrative has not materialized, and PayPal, while not as undervalued as I initially thought, is still trading very undervalued. However, the undervaluation could be justified given that they are quickly decelerating the business in an overall industry outlook that is set to grow in the mid-teens.

Former CEO Alex Chriss took over a sinking ship, and famously mentioned that PayPal was going to “shock the world” in January of 2024, and with a solid track record at Intuit, many investors believed him. What followed was two years of no material progress towards the goals of capturing the AI commerce market, launching a successful and prominent ads business, or meaningful innovation.

Our execution has not been where it needs to be, particularly in branded checkout.

Jamie Miller, Interim Chief Executive Officer

PayPal Q4 2025 Earnings Release

What followed in the Q4 2025 results was a fired CEO and horrific guidance for the fiscal year 2026 of declining transaction margin dollars and EPS. PayPal pulled their revenue guidance several periods ago, and instead, they give us transaction margin dollars guidance as a way to track their path towards “profitable growth”. To reach profitable growth, they sacrificed the performance of core drivers to exit the race to the bottom that all payment solution providers are participating in (resulting in a decline in take rate for all participants). Now, they’re still losing take rate, but even worse, there’s no trade-off in rapid payment volume growth. It’s a lose-lose situation in that regard.

Searching for a positive note with a lantern

While PayPal didn’t make material progress towards becoming the premier commerce orchestrator as promised, not all is doom and gloom. As mentioned, the company still has growth, and is not showing indications of ~8% annual declines as the quote implies. However, the growth in revenue for FY2025 was a mere 4.3% Y/Y, while being participants in a digital payments market that grew ~20% Y/Y, and is expected to compound annually at a rate of ~20% over the coming 7-10 years.

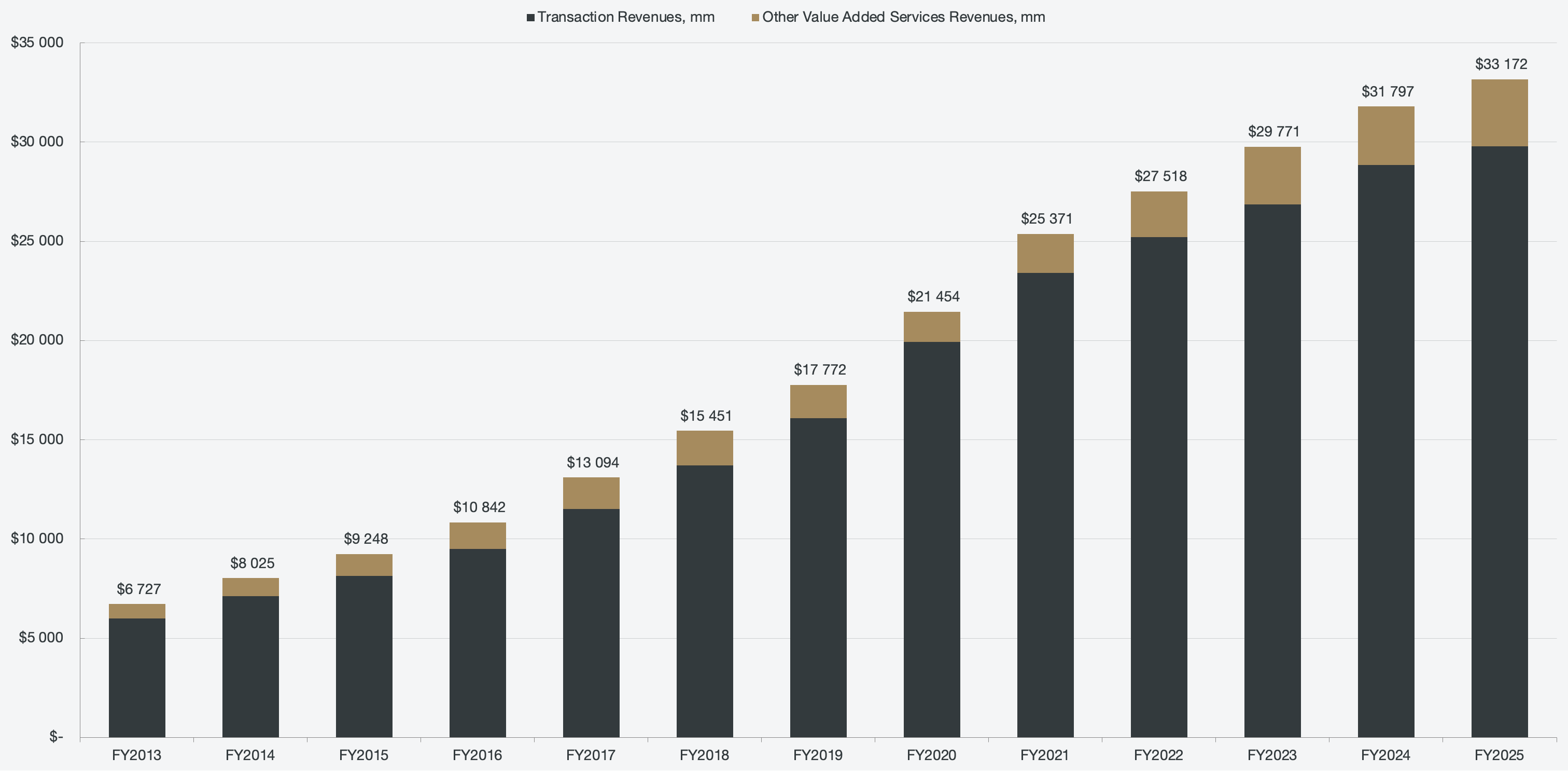

Figure 1: Segmented revenues

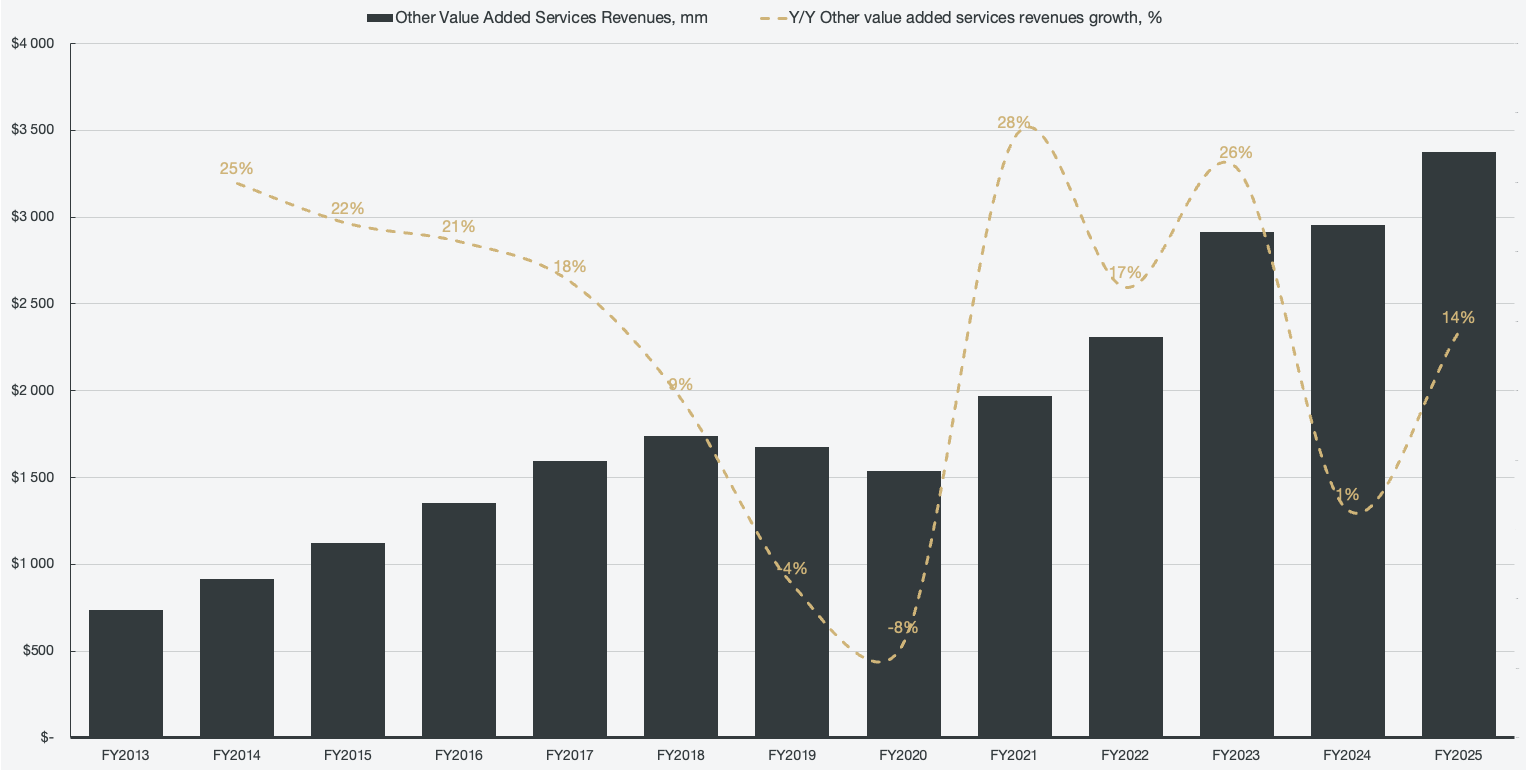

The core segment, transaction revenues, only grew 3.3%. The other value-added services (OVAS) grew 14.2%, showing signs of life after a flat 2024. The 14.2% increase signals that the business is gaining traction across credit and interest products, as well as subscription and partnership fees.

Figure 2: Other value-added services revenues

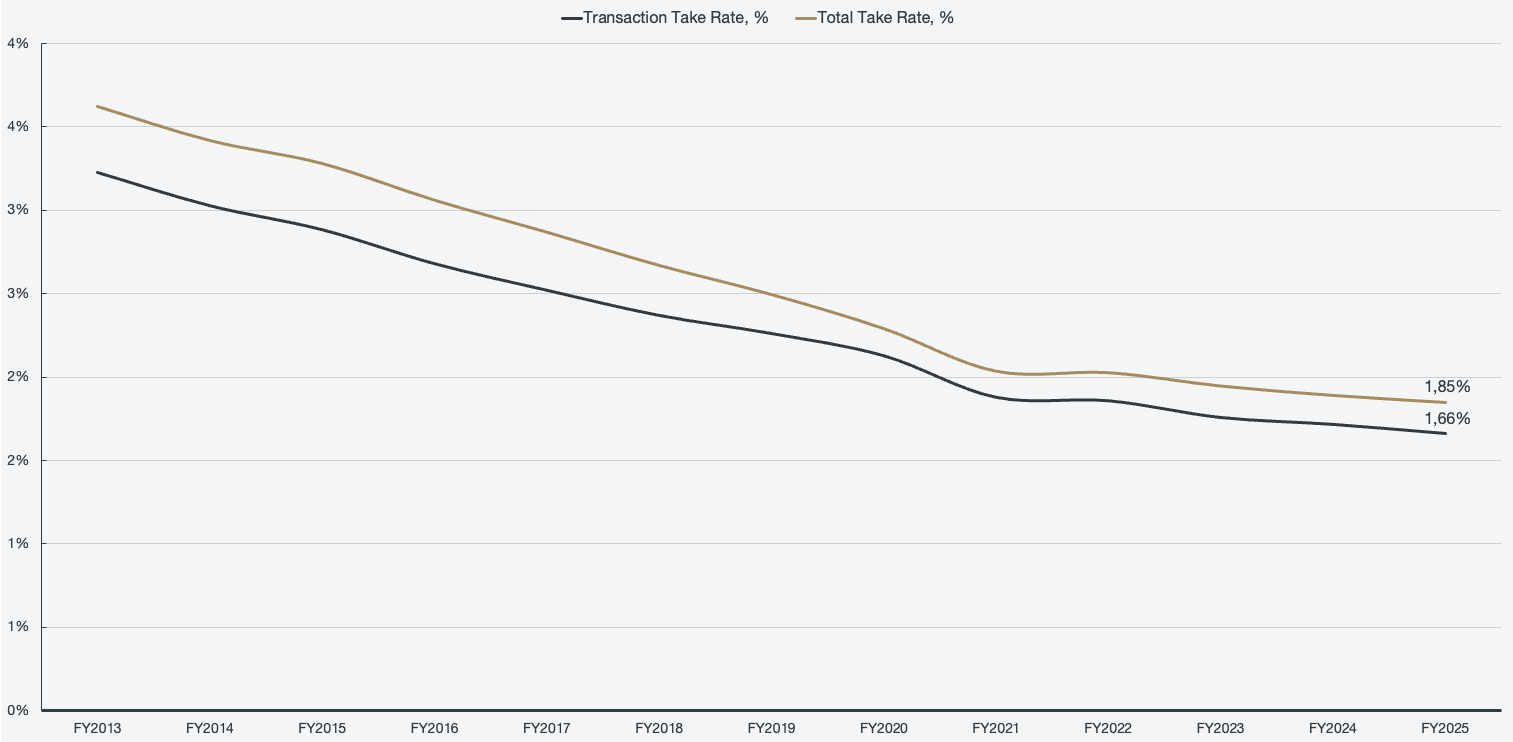

All the segmented total payment volume segments grew more than 3.3%, which means that the take rate decreased for the transactions. The whole purpose of having an off-year to reposition the business was to stop the bleeding take rate at the expense of growth, but as mentioned, PayPal lost on both ends.

Figure 3: Take rates

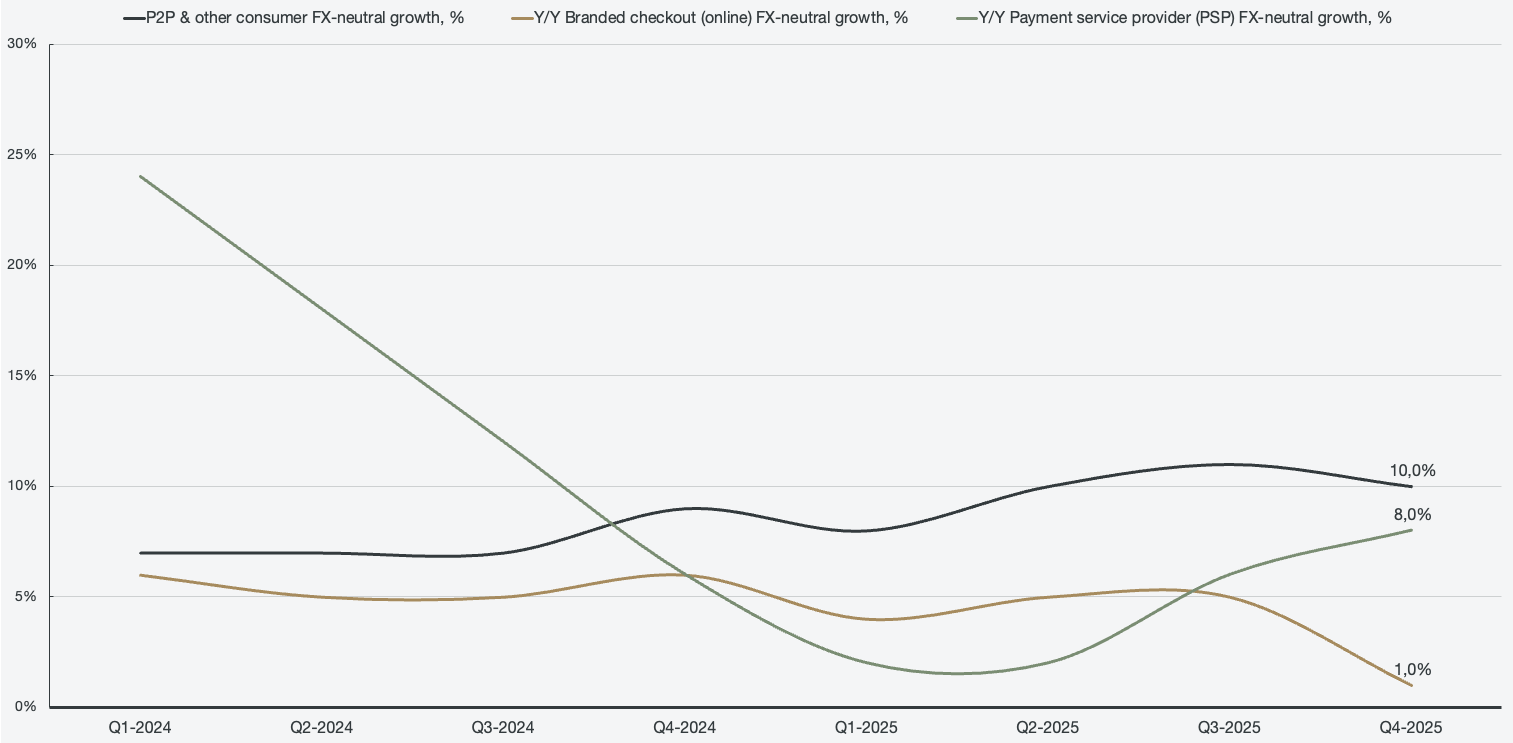

The highest margin segment, branded checkout, only increased 4% on a currency-neutral basis for the year, and 1% in Q4 2025. Peer-to-peer (P2P) is accelerating as a result of Venmo’s growth, but the real pain is felt in the payment service provider (PSP) solution, which accounts for a majority of the TPV.

Figure 4: Segmented TPV growth rates

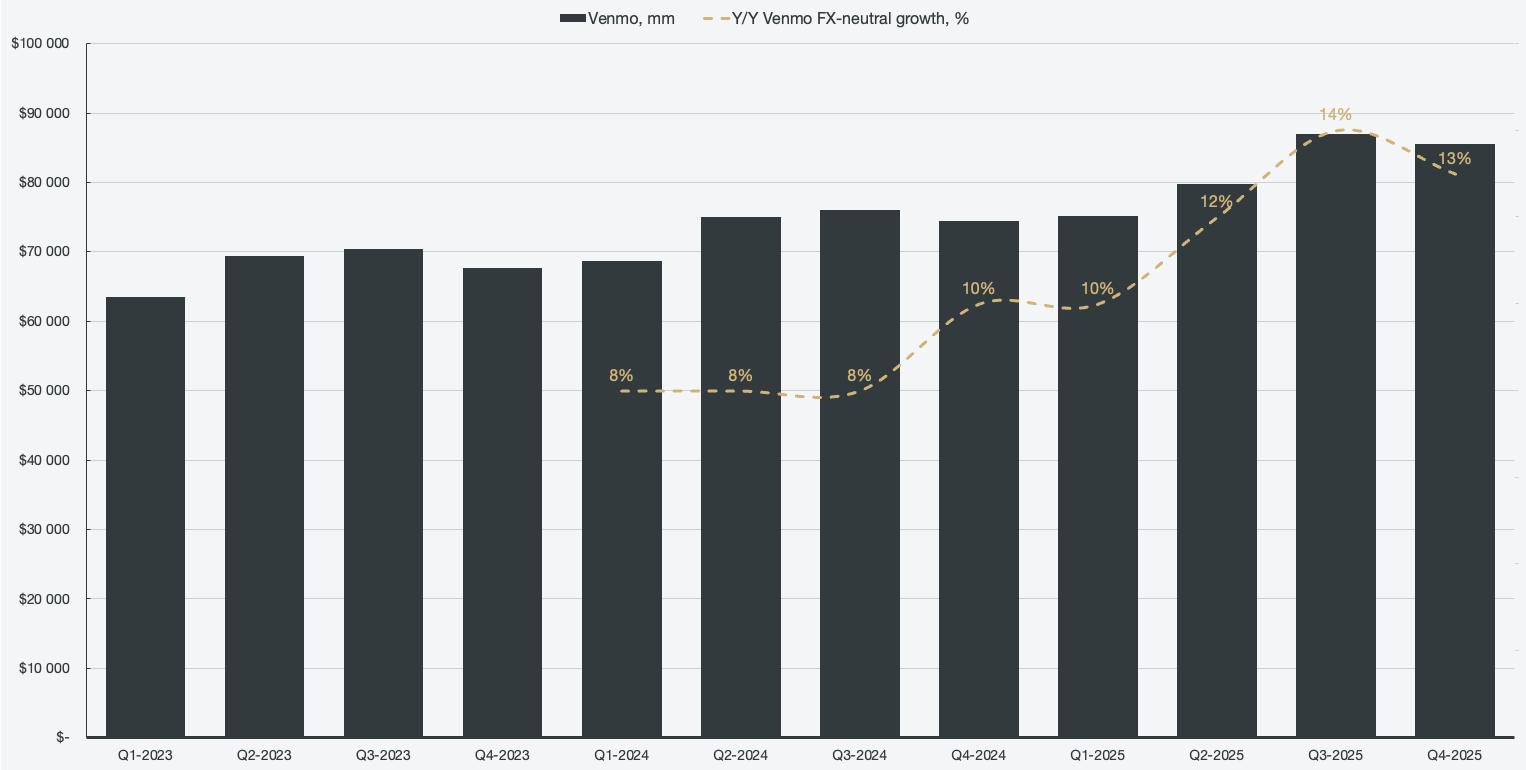

Venmo is one of the strongest financial services in the U.S., and is consistently at the top of most downloaded apps in the Apple and Android app stores. However, for a long time, it has not been properly monetized or given enough attention. One of the few developments under Alex Chriss’s management was improved substantially. Historically, even though Venmo was owned by PayPal, the two operated in silos without communication, essentially operating independently. That has changed, and Venmo is now starting to see innovation, growth, and monetization. However, even Venmo, while gaining traction as of late, is still stuck at where it was three years ago. In Q1 of 2023, Venmo made up 18% of total TPV. In Q4 of 2025, it makes up 18% of total TPV; essentially, there hasn’t been any progress.

Figure 5: Venmo TPV

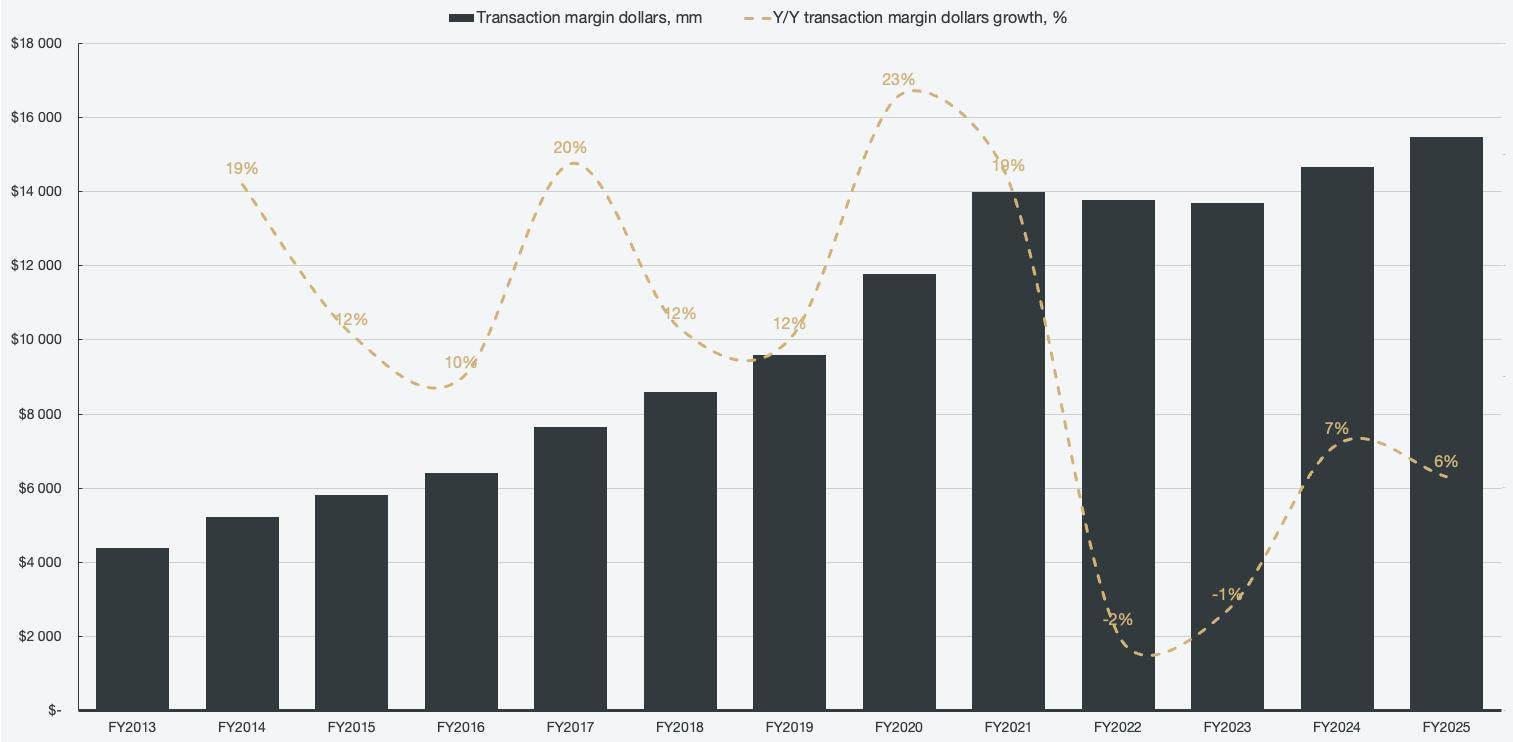

Looking at the core focus for 2025, transaction margin dollars, we saw an increase of 6%. This is expected to decrease in 2026, per management guidance as of Q4 2025. On a positive note, the transaction margins have been increasing for two years in a row, after dropping from 65.26% in 2013 to a low of 46.03% in 2023. As of 2025, the transaction margin is 46.62%, implying that the bleeding has ceased for the time being.

Figure 6: Transaction margin dollars

Looking at the operational statistics, it is a bit of a mixed bag. For the first time since 2022, PayPal managed to grow the average active accounts by ~7 million, representing 1.8% growth Y/Y.

Despite 7 million additional active accounts, the number of payment transactions decreased by ~1 million compared to 2024. For reference, it is the first time in reported history that PayPal failed to grow the number of payment transactions Y/Y. Historically, payment transactions have been growing on average by ~20% CAGR since 2013, and that includes the -3.7% in 2025.

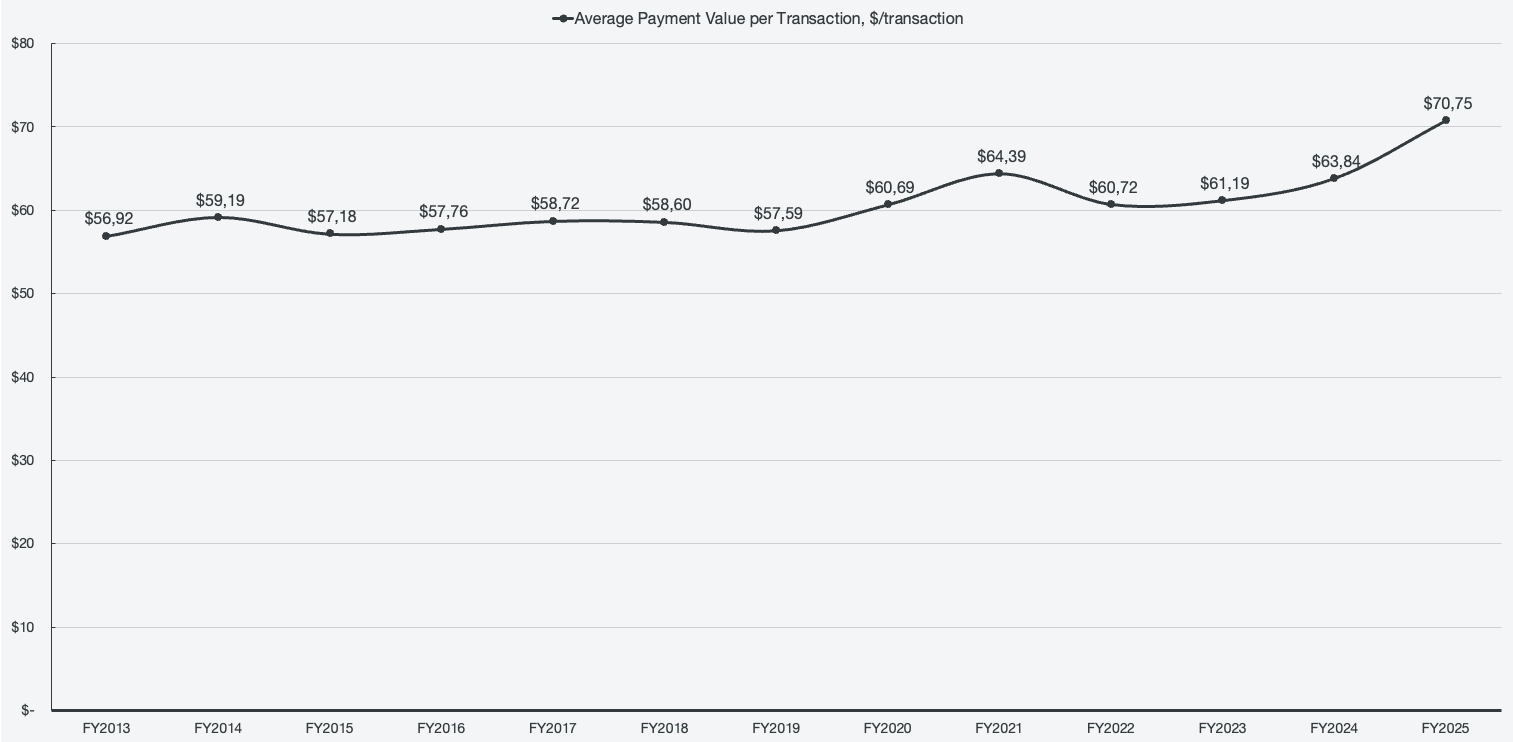

Since total TPV grew by 6.7% Y/Y (10% FXN) while total payment transactions decreased, it means that the average payment value increased, crossing $70 for the first time (~11% growth).

Figure 7: Average payment value per transaction