Robinhood Markets: Finance Juggernaut

Equity research follow-up coverage, rating unchanged

Robinhood just reported a fantastic quarter where every part of the business is heading to new highs, while simultaneously developing the business in accordance with my investment thesis.

One of the largest risks associated with Robinhood is the cyclical nature related to market activity. For this purpose, it is important that Robinhood keep expanding into various lines of business in order to diversify but also stay competitive in one of the fiercest spaces in the market, the fintech space.

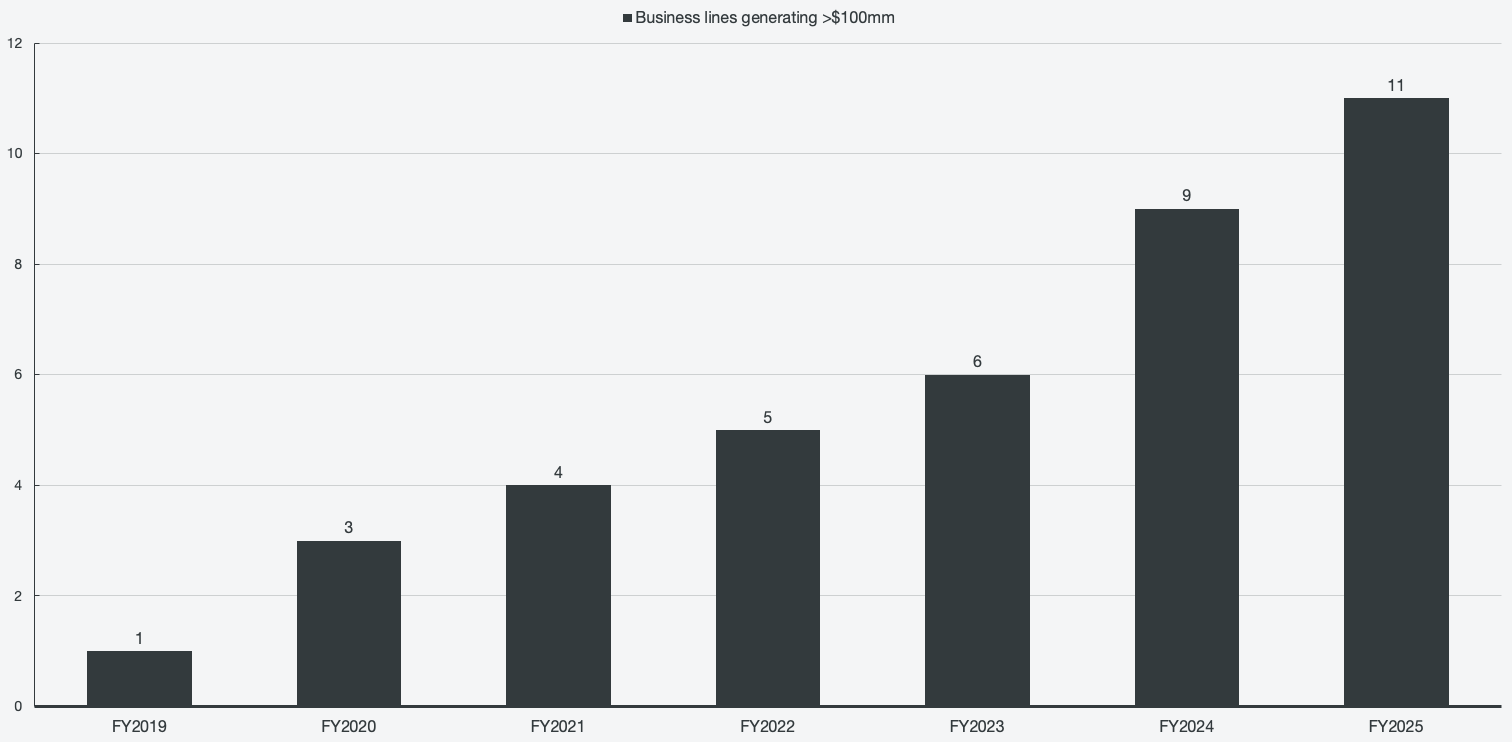

Figure 1: Business lines generating at least $100 million

This quarter not only further convinced me that Robinhood is an exceptionally high-quality company but also that management are execution monsters. As a result, the fair intrinsic value for the business has increased substantially compared to Q2, and both the short-term and the long-term look very bright for the company.

Company profile

November 25, 2025 Follow-up coverage

Direction: Buy

Previous fair intrinsic value: $108.21, as of July 26, 2025

Symbol: HOOD, Exchange: NASDAQ

Sector: Financial Services, Industry: Capital Markets

Theme: Growth

Fair intrinsic value: $172.50 (+50%), as of November 25, 2025

Market capitalization: $105 536 million

Pricing data: P/S 25x, P/E 48x

Previous coverage:

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

Unmatched execution

It’s been a focus point of mine these past few quarters to pay attention to the lines of business outside of sheer trading-related revenue. As noted in Figure 1, Robinhood has now reached 11 different business lines that have an annual run rate of at least $100 million. These are:

2019: Options trading.

2020: Margin interest and equities trading.

2021: Crypto trading.

2022: Margin-based securities lending.

2023: Cash sweep.

2024: Fully paid securities lending, gold subscriptions, and instant withdrawals.

2025 year-to-date: Prediction markets and Bitstamp.

In addition, we already know about several other businesses within Robinhood that are just about to start scaling while also consistently releasing more and more features. The pace of innovation is incredible, and the execution has been relentless. For the quarter, the receipt of the company’s pace is represented in the form of a 100% Y/Y revenue growth increase.

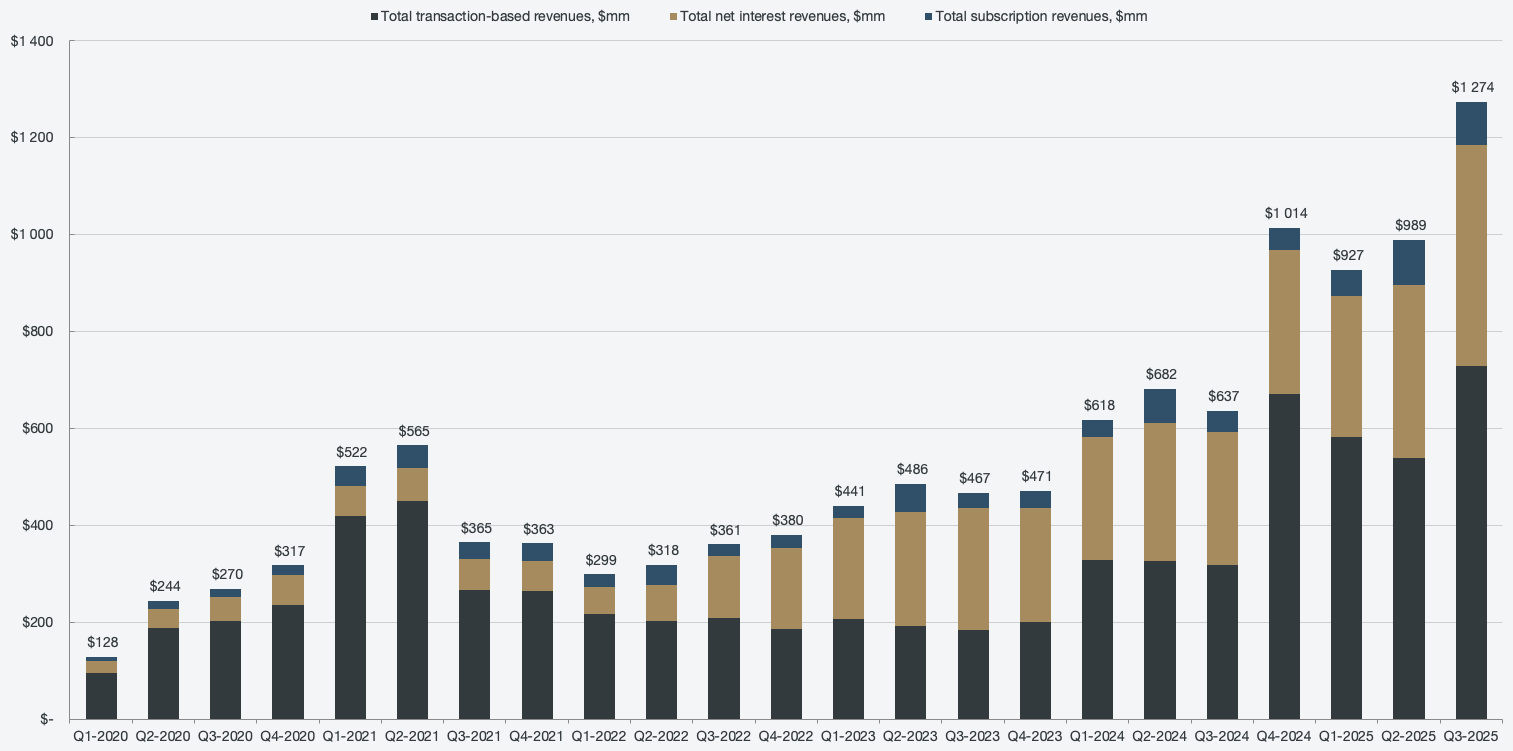

Figure 2: Segmented revenues

In addition to executing on the product front, every part of the existing business is accelerating. While trading (transaction-based revenues) remains the main source of revenues, it is decreasing. The important dynamic to understand here is that the overall transaction-based revenues stemming from payment for order flow are showing a downtrend as a percentage of total revenue, despite a big increase in PFOF revenue for the quarter. This implies that other, less volatile revenue sources are gaining in the mix.

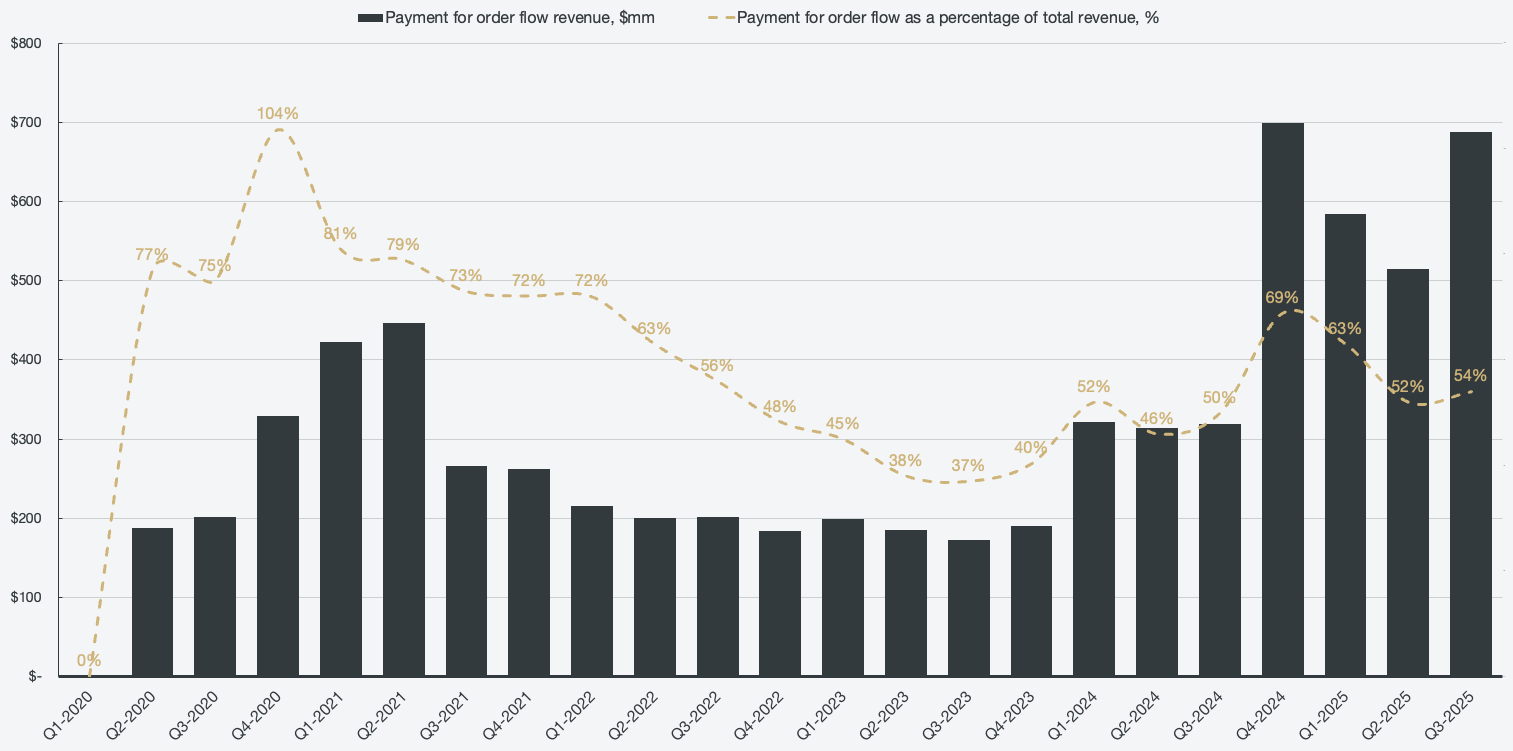

Figure 3: Payment for order flow revenues

Payment for order flow mainly accounts for equities, cryptocurrency, and options trading activities. However, the Other segment within transaction-based revenues has increased massively as of late. This is the result of prediction markets growing immensely. Currently, prediction markets are not a broken-out line item, but the sudden increase in the Other segment is primarily driven by prediction markets and instant withdrawals. Other is quickly catching up to equities, which once again shows how quickly Robinhood is able to scale their business lines.

[…] We’ve doubled volume every quarter since then to 2.3 billion contracts in Q3. And the month of October alone was up to 2.5 billion contracts. So October by itself was bigger than all of Q3 combined.

Vladimir Tenev, Chief Executive Officer

Robinhood Markets, Inc., Q3 2025 Earnings Conference Call

Prediction markets present a whole new avenue of revenues at limited risk to Robinhood. Robinhood has partnered with Kalshi, who, together with Polymarket, has been the main prediction market available. Polymarket used to have a large majority of the notional volume market share, but Kalshi has managed to outpace Polymarket and has since flipped Polymarket to become the largest prediction market by volume. As of Q3, Kalshi had a 52% overall market share, and with October surpassing the whole of Q3 in terms of overall volume, Q4 might see an even bigger market share gain.

Figure 4: Prediction markets notional volume

Robinhood currently features over 1000 different contracts across many categories, including sports, politics, economics, and culture. Recently, it was also announced that Robinhood offers predictions on the weather, showing that the options are truly limitless for the product. The only risk associated with prediction markets for Robinhood is that assets on the platform associated with prediction markets may be volatile and offer a lot fewer long-term monetization opportunities compared to an investment balance.

Figure 5: Segmented Transaction-based revenues

Equity trading has a relatively low yield due to its maturity. There are not a lot of spread opportunities in the equities markets, which is why market makers pay a lot less for the order flow. It has been trending lower throughout its reported history, but Q3 stopped the bleeding. However, investors should expect the equities yield to trend lower over time.

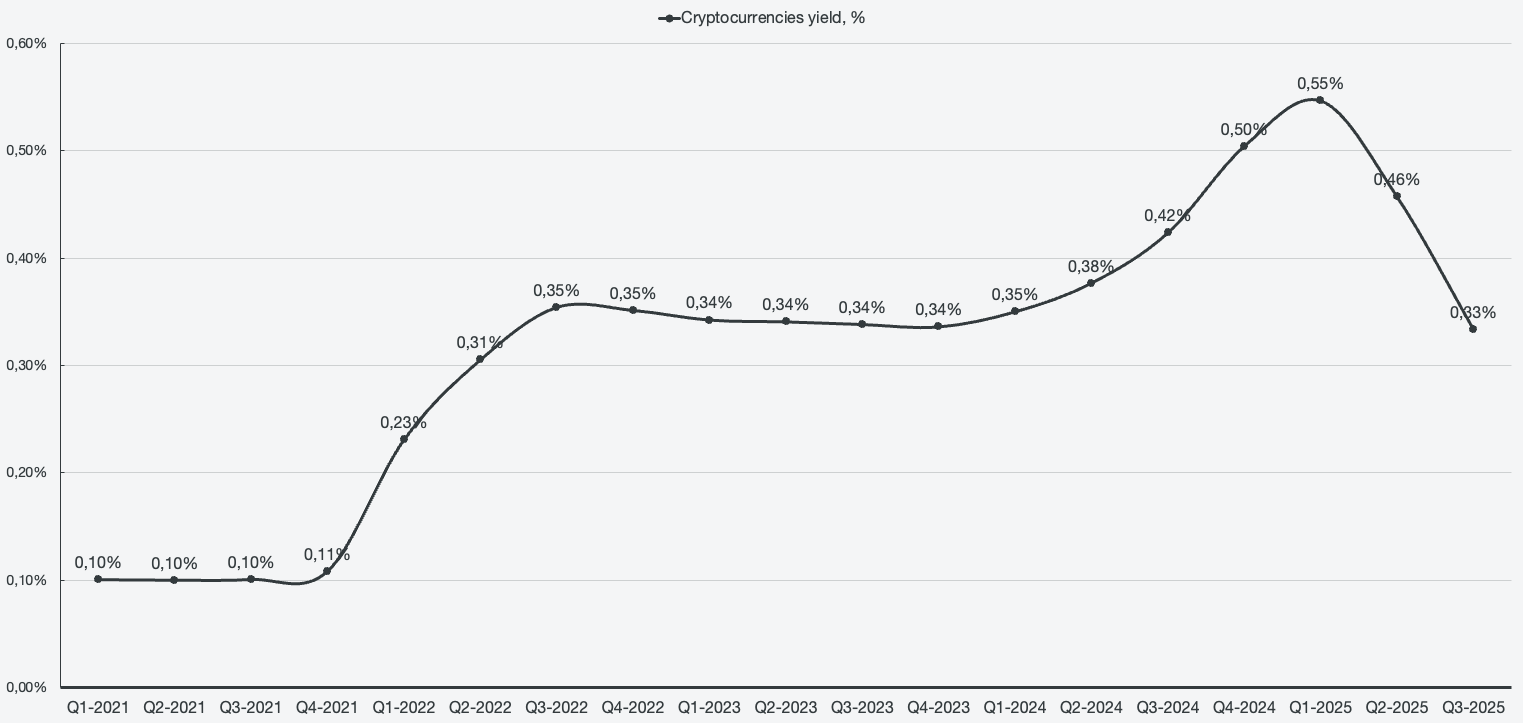

Cryptocurrencies and options are not as mature and still present attractive spreads for market makers. The yields are significantly higher compared to equities, where on average, a Robinhood user has to spend ~3x the amount of money trading equities in order to equal one cryptocurrency trade. That used to be ~5x, but since the acquisition of Bitstamp, it has been trending lower as well. The options yield has stayed relatively stable at 50% in Q3 2025, compared to 51% the quarter prior.

Figure 6: Cryptocurrencies yield

The sharp drop in yields may seem detrimental to the business at first glance, but there is still a tremendous opportunity for yield expansion in the space. When comparing to Coinbase, the retail-facing business typically has triple the yield, if not more. That inherently means that Robinhood still has a lot of expansion on the retail side that they may capture, since it is still a relatively immature market. What is interesting is that Robinhood is actually already at parity with Coinbase when accounting for institutional trading.

In Q2, Robinhood started reporting Bitstamp as part of the crypto mix, which is also when the drop-off began. When overlaying a chart of Coinbase’s yield, Robinhood is actually already at parity. In the following chart, I have only calculated the retail yield until Q2 2025, at which point I incorporated Coinbase’s institutional trading as well. The sharp drop implies that Bitstamp is generally a lot higher margin than Coinbase’s institutional offering. Bitstamp grew 60% Q/Q, showing tremendous scaling opportunities within the segment.

Figure 7: Coinbase cryptocurrencies yield against Robinhood’s cryptocurrency yield

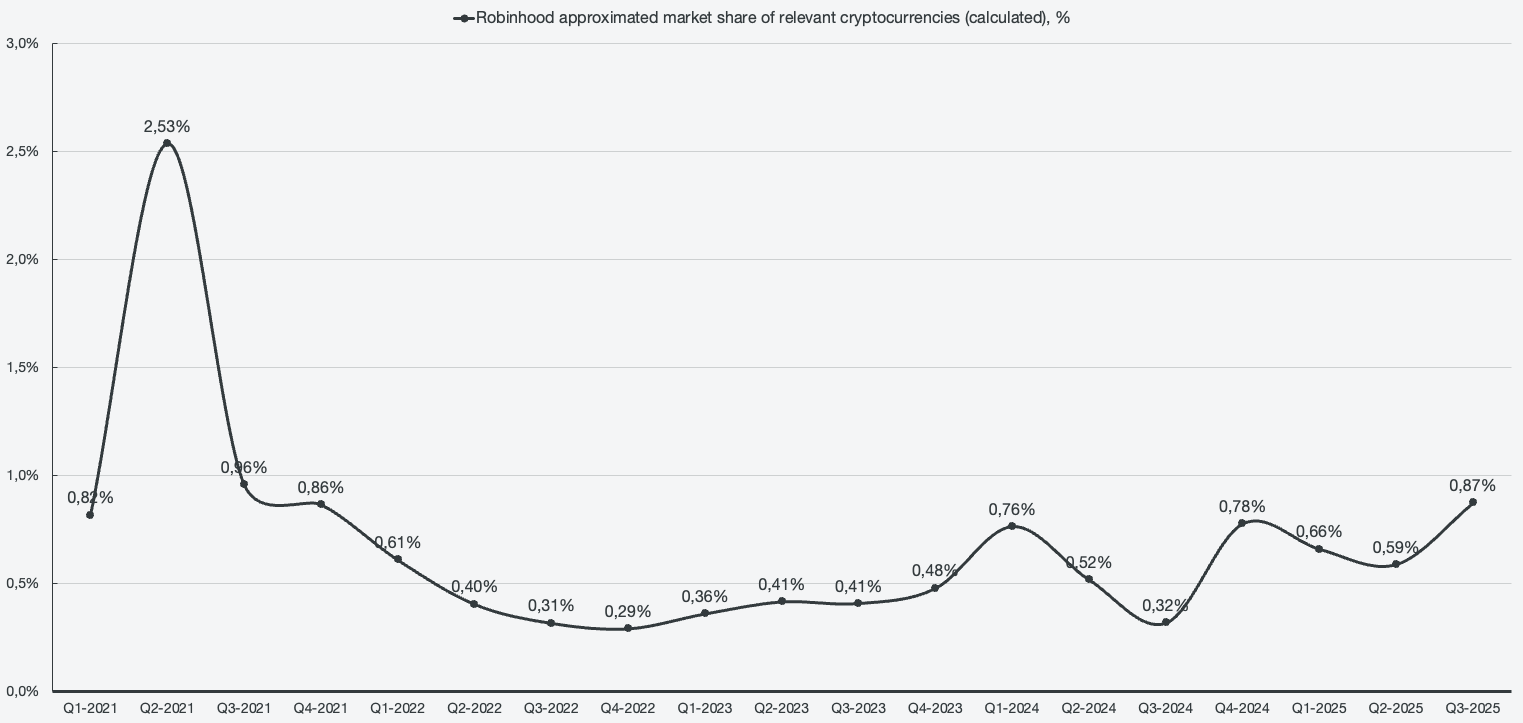

Overall, Robinhood is gaining market share in the cryptocurrency space. I calculate an approximated market share by comparing Robinhood’s crypto volumes against the total volume of relevant cryptocurrencies (Bitcoin, Ethereum, and Dogecoin). By this measure, the overall approximated market share is 0.87%. However, in their Q3 earnings presentation, Robinhood presented a 1.08% calculated market share of the cryptocurrency markets, defined as follows:

Figure 8: Robinhood’s approximated cryptocurrency market share

The way I calculate Robinhood’s equities market share is the same as how Robinhood calculates it in their Q3 earnings presentation. As of Q3, Robinhood is quickly approaching a new all-time high in terms of market share, only 0.05% lower than the peak in 2021.

Figure 9: Robinhood’s approximated equities market share

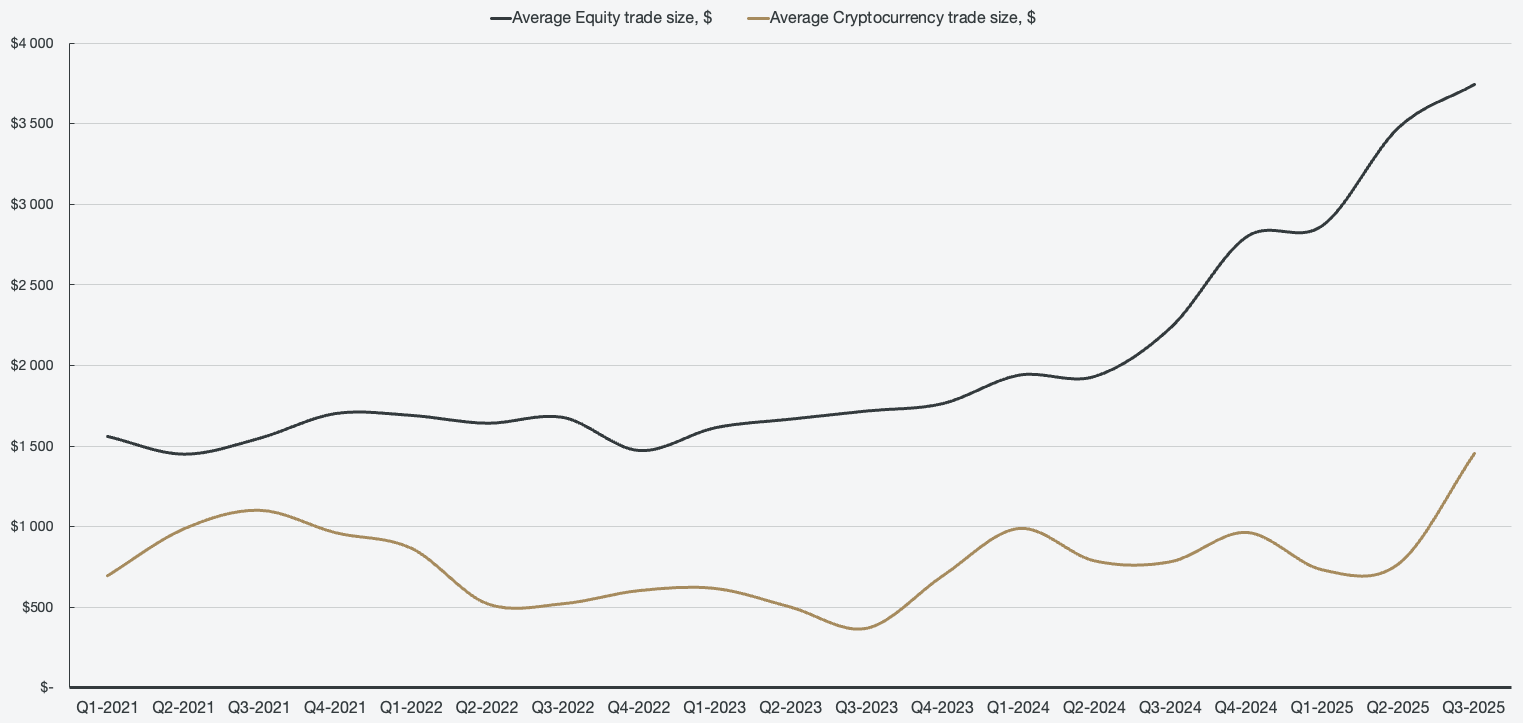

The increases in market share are primarily driven by trade sizes increasing substantially and showing a positive upwards trend. The average equity trade size is ~$3750, while the average cryptocurrency trade size is ~$1500. That represents:

34% Y/Y equity trade size growth

51% Y/Y cryptocurrency trade size growth

In addition, daily average revenue trades (DARTs) grew ~35% for both equities and cryptocurrencies for the quarter.

Figure 10: Equities and cryptocurrencies average trade sizes

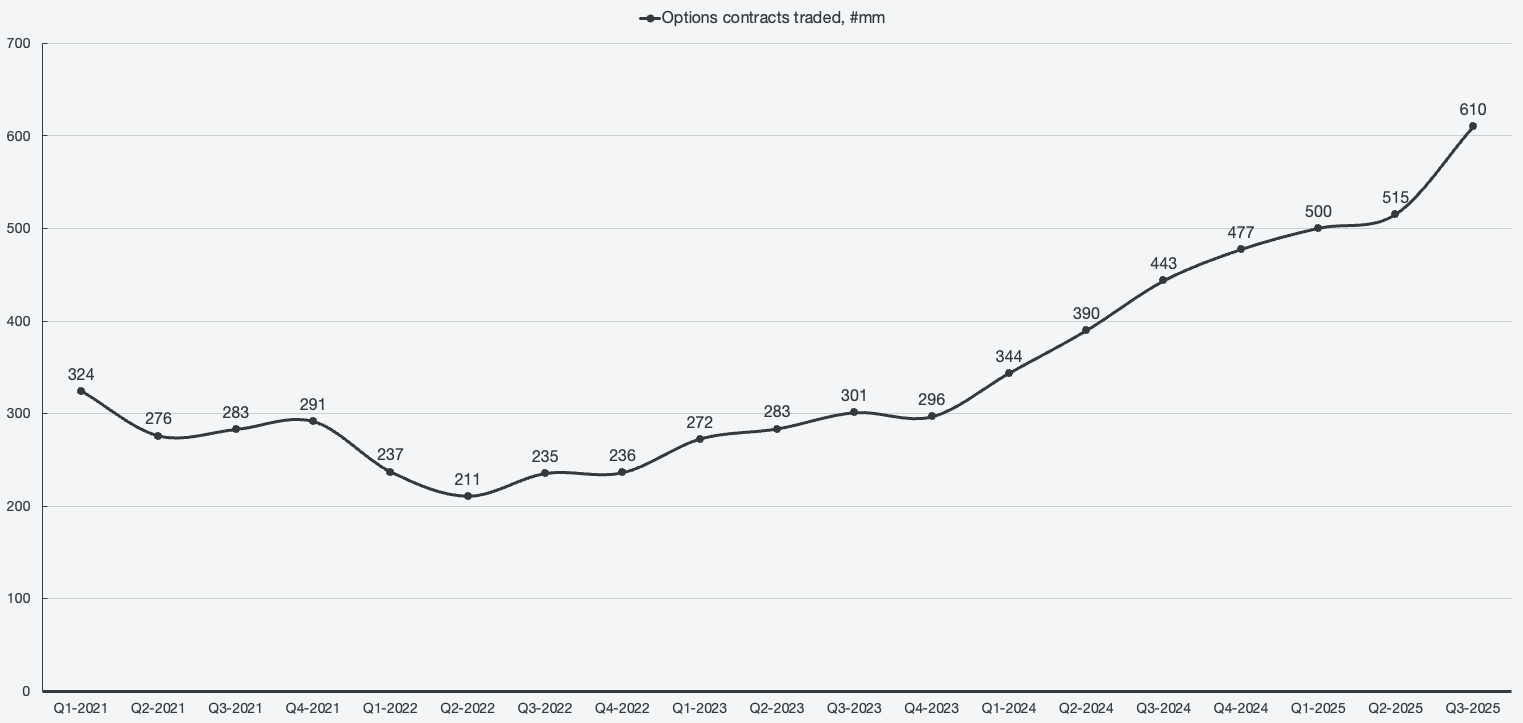

The main revenue driver continues to be options trading, and similarly to other segments, options are accelerating. During Q3 2025, options revenue reached an all-time high of $304 million, representing ~50% Y/Y growth. The total amount of options contracts traded also reached an ATH of 610 million contracts, and the trend is accelerating.

Figure 11: Options contracts traded

Options have significantly lower volume than the other trading segments and also present the highest spreads. This makes it especially attractive for market makers to bid for the order flow, which is why options remain such a driver for Robinhood’s overall business. Options trading is gaining in popularity, and Robinhood’s UI for trading options is, in my opinion, best-in-class. While it’s gaining traction among households, it is still a long way off from maturity, implying that Robinhood has a long runway of high-margin options trading.

Similarly to options reaching all-time highs in recorded history, so did equity volumes in Q3. The previous quarterly record was just shy of half a trillion dollars during the 2021 bubble. In Q3 of 2025, that all-time high was surpassed quite handily, and Robinhood recorded ~$650 billion of equity volume. Similarly, cryptocurrencies showed a recent high, but without surpassing 2021 highs.

Figure 12: Equity and cryptocurrency volumes