S&P Global: Undervalued Even With AI Disruption

Equity research follow-up coverage, rating unchanged

Many parts of the markets have had to take a backseat view and watch AI and AI infrastructure-related stocks soar. Many businesses have seen drastic reductions in their stock quote out of fear of AI disruption. S&P Global is no exception, with the narrative of AI disrupting its market intelligence business segment. I don’t find it likely that S&P Global will suffer from AI disruption, simply because as much as 95% of the data the company provides is proprietary.

However, despite it being unlikely, S&P Global is undervalued even if AI eats the whole market intelligence segment and reduces it to ashes. The rest of the business is strong enough to warrant an intrinsic value above where the stock is, and has been trading. That is the kind of optionality that I like to look for in businesses, especially high-quality ones like S&P Global.

Company profile

18 June, 2026 Follow-up coverage

Direction: Buy

Previous fair intrinsic value: $720.8, as of December 21, 2025

Symbol: SPGI, Exchange: NYSE

Sector: Financials, Industry: Financial Data, Stock Exchanges

Theme: High quality

Fair intrinsic value: $562.14 (37%), as of June 19, 2026

Market capitalization: $122 003 million

Pricing data: P/S 7.76x, P/E 25.54x

Previous coverage:

TYPEFCAPITAL.COM

Consider following me on X and YouTube.

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell securities.

AI is a tailwind, not a headwind

It has been a while since I revisited S&P Global for a report, simply because this type of high-quality compounder doesn’t require much maintenance. There generally are not many drastic risks or narratives that warrant watching over them like a hawk. They fit the bill of Buffett’s philosophy of buying stocks you would be happy owning even if the market shuts down for 10 years, as well as the farm test. Buffett likes to compare owning stocks to owning a farm, where the farmer buys land based on its ability to produce crops, not the daily fluctuations in real estate quotes of the farm.

S&P Global operates a high-quality business, but it is subject to fluctuations. The most lucrative and robust segment is its credit rating business, which is highly cyclical and subject to external factors. However, over time, the segment’s ability to generate cash is borderline unfair. Over the past 10 years, S&P Global’s revenue has increased by 178%, representing a moderately impressive ~11% CAGR. However, the cash the company generated over the same period increased by a staggering 364%. That is what investors should expect from this business in the future, and why compounders are attractive. Finding them out of favor is a lucrative proposition for investors; that’s where we are today with S&P Global.

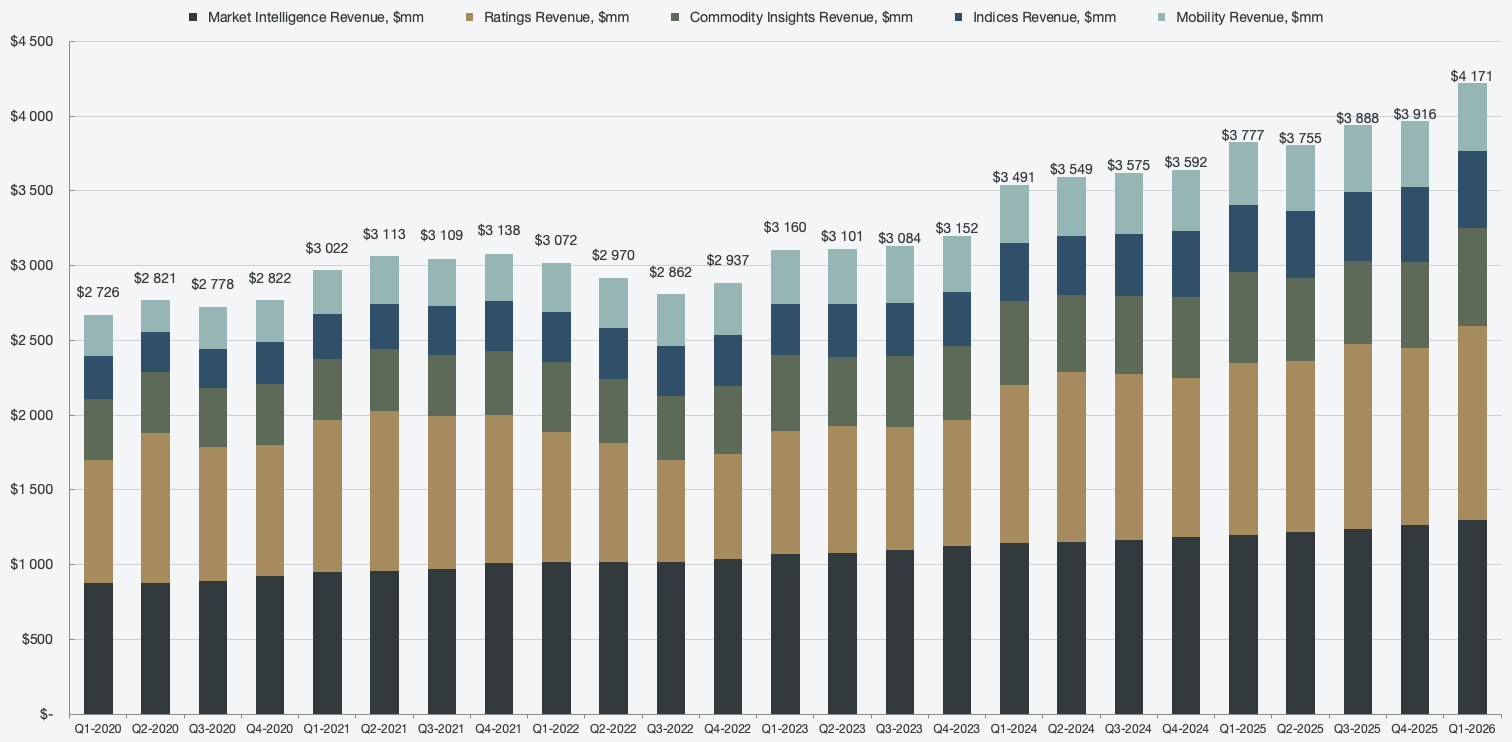

Figure 1: Segmented revenue

However, any material threat still needs to be thoroughly investigated for its impact. Generative AI is indeed a threat to software businesses in general, and by extension, it is fair to assume that it can impact the market intelligence segment. Two-thirds of S&P Global’s revenue and three-quarters of its profits are tied to benchmarks, such as ratings, indices, and commodities. Those are very resilient businesses, and S&P Global is the sole source for that proprietary data. What investors are worried will be disrupted is primarily the Capital IQ platform, which is a competitor to the Bloomberg Terminal, Refinitiv, and other similar platforms such as FactSet. However, Capital IQ represents only 6% of total revenue, and even less of the overall profits.

One trend that can be observed with the AI revolution, and perhaps because of it, is vendor consolidations and the demand for value creation. Compared to competitors in the market intelligence space, S&P Global owns data across all parts of the market and, as such, has been well-positioned to increase its market share rather than see it diminish. Growing 6-8%, as management targets for the segment, is outpacing the general market segment, meaning that S&P Global is actually about to grow its market share in the face of AI, not have it diminish. That is likely due to S&P Global being at the forefront of implementing AI solutions and bundling data for their customers, allowing for vendor consolidation. For the most recent quarter, MCP connections grew 500% Q/Q and 100% M/M, showing that AI integrations are growing rapidly within S&P Global. MCP stands for Model Context Protocol and is an open standard that allows AI models to interact with data sources, applications, and tools.

When we look at customers who are looking to invest more in their AI solutions, looking to invest more in data, looking to really scale out some of these strategic initiatives, S&P Global is probably as well-positioned as any company in the world to facilitate that.

Mark Grant, Senior Vice President, Investor Relations and Treasurer

Mizuho Technology Conference, June 10, 2026

The MCP growth shows inherent robustness to the data S&P Global has sole ownership of, since it is meant to be used with the client’s internal AI solution, even if they do not use Capital IQ. However, Capital IQ is seeing increased pricing power as well. Clients are cited to pay 35-45% more during renewals to gain access to AI-ready versions of S&P Global’s datasets, per CEO Martina Cheung during Bernstein’s 42nd annual strategic decisions conference (May 27, 2026).